Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

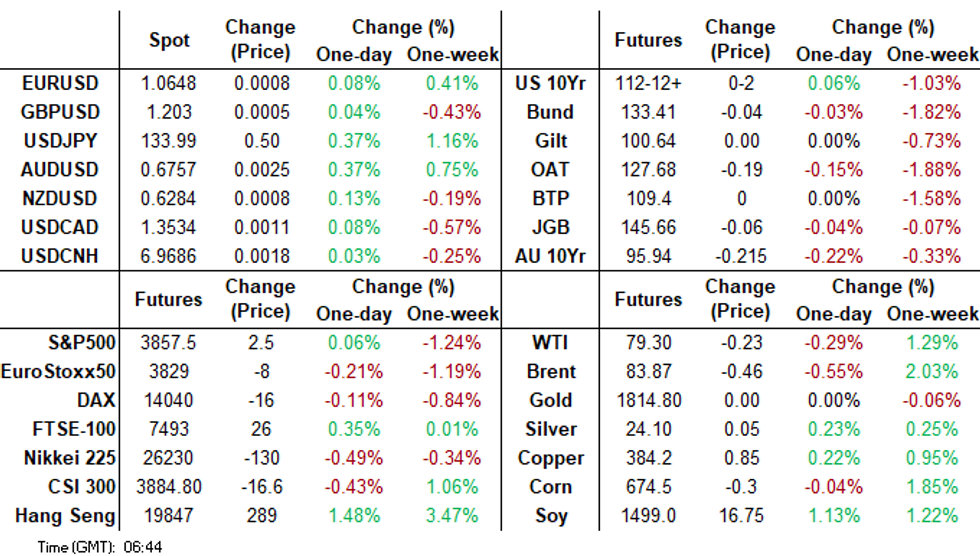

- Early Asia-Pac trade saw weakness in wider core FI markets as the space/region caught up with moves in European FI & U.S. Tsys since Friday's local close. The latest Chinese reopening push & hawkish ECB speak provided the focal points on the news flow front over the Christmas break. This dynamic triggered a round of unscheduled BoJ purchases.

- JPY weakness was at the fore in FX trade. The summary of opinions from the BoJ's most recent meeting pushed back against the notion of any premature moves away from ultra-easy monetary policy conditions, while Kuroda has recently played down the idea that YCC tweak represented a form of monetary tightening. Yield differentials are also tracking in the USD's favor.

- Looking ahead, the main focus will be on U.S. data, with the Richmond Fed m'fing index and pending home sales due.

US TSYS: Light Twist Flattening Observed

TYH3 deals +0-02+ at 112-13, in the middle of its narrow 0-05 Asia-Pac range, on limited volume of ~65K.

- Early Asia-Pac trade saw some marginal weakness as the region reacted to Tuesday’s bear steepening.

- Still, that move was limited, as the major cash Tsy benchmarks failed to breach their respective Tuesday yield peaks.

- We then saw a pullback from session cheaps, with the long end leading the move as the curve twist flattened, leaving the major benchmarks 1bp cheaper to 2bp richer, with a pivot around 10s.

- Macro headline flow was subdued at best, with continued focus on the latest wind back of COVID-related restrictions in China.

- Looking ahead, the NY docket will see the release of pending home sales & Richmond Fed m’fing data, with 2-Year FRN and 5-Year Tsy supply also due.

JGBS: Global Core FI Impetus & BoJ Purchases Promote Twist Steepening Of The Curve

Spill over from weakness in core global FI markets triggered a round of unscheduled BoJ purchases in paper out to 10s (in both Rinban and fixed rate varieties), which provided a brief boost for JGB futures, before that particular impulse faded.

- JGB futures then printed through their overnight session base in the latter rounds of morning trade, but the move lacked meaningful follow through, allowing the contract to bounce, printing at unchanged levels ahead of the bell.

- The presence of the aforementioned BoJ purchases provided a twist steepening impulse on the curve, leaving the major benchmarks 2bp richer to 3bp cheaper, with 10s providing the firmest point on the curve as paper beyond that point cheapened.

- The summary of opinions covering the BoJ’s Dec meeting provided fairly run of the mill comments, generally within the confines of the lines of rhetoric that we have witnessed since the surprise YCC tweak.

- Looking ahead, weekly international security flow data headlines Thursday’s thin local docket, with the general direction of travel for wider core global FI markets and the potential for unscheduled BoJ JGB purchases eyed.

AUSSIE BONDS: Early Steepening Holds, Relative Underperformance Extends

ACGBs adjusted cheaper after the Christmas break, softening in lieu of weakness in core global FI markets that came on the back of the latest reopening push in China (with most of the focus on the wind back of international travel restrictions/limitations) and some hawkish ECB speak.

- The space went out just above worst levels, with YM -19.0 & XM -21.5, while wider cash ACGB trade saw 15-21bp of cheapening as the curve bear steepened.

- ACGBs extended their recent run of underperformance vs. their global counterparts, with the AU/U.S. 10-Year yield spread briefly moving out beyond +20bp, before finishing off extremes, albeit still comfortably wider than late Friday levels.

- There wasn’t anything in the way of meaningful domestic/idiosyncratic headline flow.

- The local docket is empty in the time between Christmas and the New Year, which will leave broader macro headlines and spill over from wider cross-market flows at the fore in the coming days.

- Meanwhile, expect volumes and general liquidity to be limited as many participants will take time off between Christmas and NY.

NZGBS: Under Pressure, Payside Swap Flow Noted

NZGBs could never shake off the downward bias established at Wednesday’s open, as catch up to weakness in U.S. Tsys either side of the Christmas break & the latest roll back of Chinese COVID restrictions (most notably re: international travel), as well as some fresh downward impetus for core global FI markets in Asia-Pac hours, all applied pressure.

- That left the major NZGB benchmarks running 9-13bp cheaper across the curve at the bell, with the belly leading the weakness.

- Meanwhile, payside flow in swaps helped apply pressure, with the major swap rates running 14-22bp higher as that curve bear steepened and swap spreads widened.

- There wasn’t anything in the way of meaningful domestic headline flow observed,

- The local docket is empty in the time between Christmas and the New Year, which will leave broader macro headlines and spill over from wider cross-market flows at the fore in the coming days.

FOREX: USD/JPY Recovery Continues, A$ Outperforms

The main theme today has been yen weakness. USD/JPY has continued to recover, with the pair getting to a high of 134.40 before selling interest emerged. We are now back close to 134.00, still 0.40% weaker for the yen since the open. This has helped keep the USD indices slightly higher, with the other majors tracking tight ranges. The BBDXY was last just under 1254.70.

- Weighing on the yen was the BoJ Opinion Summary from the last policy meeting, which pushed back against any premature moves away from ultra-easy monetary policy conditions. Yield differentials are also tracking in the USDs favor. China's rapid move away from CZS is at risk of being inflationary, which is aiding the US cash Tsy yield move higher.

- Commodities are also generally supported, with oil holding close to recent highs (Brent last near $84.40), while copper has nudged up to $384.20. The A$ has outperformed, up nearly 0.30%, last just off session highs at 0.6745. AUDJPY is back close to 90.50.

- The AUD/NZD cross is back at 1.0760, fresh highs since the start of the month. NZD/USD is near 0.6270, slightly down for the session, but up from earlier lows just under 0.6260.

- Looking ahead, the main focus will be on US data out later, with the Richmond Fed index and pending home sales due.

ASIA FX: Currencies Sensitive To US Yields Weaken, Won Gains Persist

Most USD/Asia pairs are higher today, with firmer US yields and more elevated oil prices negative external headwinds. The won is the main exception, continuing to outperform. In terms of data tomorrow, South Korean industrial production prints, while Thailand trade figures are also due.

- USD/CNH has consolidated today, after the China currency rallied over the past two sessions as further covid restrictions were cut. We have stabilized close to 6.9700. The CNY fixing was close to neutral.

- 1 month USD/KRW has been offered for much of the session, last just under 1267, versus an open near 1272. Yesterday's lows were just under 1265. Onshore equities have slumped over 2%, following US led tech weakness, while offshore investors have been large sellers of local equities (-$403mn). Dollar selling, potentially related to onshore hedging off offshore asset positions, seems to be dominating for now.

- USD/IDR is higher, last around 15710, +0.30% firm for the session. This is fresh highs in the pair since the start of the month. The firmer US real yield backdrop is likely weighing on sentiment. November highs in the pair were around 15750.

- USD/THB sits slightly above recent lows, the pair last at 34.68. Through December dips sub 34.60 have been supported. Like other pairs in the region today, the USD is seeing some support, amid higher yields and a firmer oil price backdrop. Optimism around a pick-up in China outbound travel is a clear positive for the local currency. The government's latest estimates of 25million arrivals for 2023 is critical for a further improvement in the growth backdrop. The finance minister stated as much yesterday, with the government targeting 3.8% growth this year. The consensus sits slightly lower at 3.7%.

- USD/PHP is continuing to recover higher. The pair got close to 56.30 in the first part of the session but we are now back to 56.15 (+0.40% for the session). This is close to 2% above recent lows sub 55.10. We are back above the 20-day EMA (55.882), while the 100 day sits at 56.51 on the topside. External drivers in the form of higher US yields, (real 10yr yield back to 1.58%), and higher oil prices are likely headwinds.

EQUITIES: US Tech Weakness Weighs, HSI/H Shares Outperform

Asia Pac equities are mixed, with tech sensitive indices generally underperforming in what is still holiday impacted markets. US futures have tracked a narrow range for much of the session, sitting slightly in positive territory currently (+0.05/0.10%).

- Tuesday's US session saw the Nasdaq underperform as Telsa slumped due to demand/production worries in China.

- This has seen tech sensitive plays weaken in the region. The Kopsi is off by over 2.1%, with offshore investors selling $403mn of local shares. The Taiex is down by 1.23% and the NIkkei 225 by -0.60%.

- The HSI tech sub index has bucked the trend though, up 2.7%, helping the aggregate HSI rise by over 2.1%. The China Enterprise index is also up a solid 2.60%. Mainland shares are more mixed, after +1.5% gains for the CSI 300 across the first two sessions of this week, as Covid restrictions were scrapped further. Today the CSI is down by 0.17%, but the Shanghai Composite is up slightly.

- Other markets are mixed, with overall ranges fairly modest. The JCI in Indonesia is down a by 0.87% though.

GOLD: Down On The Day But Trend Conditions Bullish

MNI (Australia) - Gold prices rose 0.9% on Tuesday on the back of signs of easing US inflation and further reopening of China, which is one of the world’s largest purchasers of gold. Today it is down 0.2% as the DXY is up 0.1% and is currently trading around $1810.75/oz.

- It has been in a tight range with a high of $1814.61 and a low of $1809.66 today. Trend conditions remain bullish for gold.

- There are only secondary data in the US this week. Later today the Richmond Fed index and pending home sales print. The FOMC minutes and the US ISM on January 4 are likely to be the next items of focus.

OIL: Oil Prices Supported By China Quarantine Easing, May End 2022 Higher

MNI (Australia) - Oil prices have been trading in a tight range during the session and are up just 0.1% after rising solidly on Tuesday. WTI is around $79.60/bbl and is just under the 50-day simple MA after a high of $79.92. It is currently above where it began 2022. Brent is about $84.40 after a high of $84.76 earlier.

- Oil markets have been supported by the announcement that arrivals into China will no longer have to quarantine. Increased international travel will boost oil demand.

- Russia has banned exports of crude to nations participating in the oil price cap from February 1, as threatened at the start of December, but it has avoided more extreme measures such as a minimum price.

- Oil and gas production in north America has been impacted by the severe winter storms.

- There is US API and EIA inventory data later today as well as the Richmond Fed index and pending home sales. The FOMC minutes and the US ISM on January 4 are likely to be the next items of focus.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/12/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 28/12/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 28/12/2022 | 1500/1000 | ** | | US | Richmond Fed Survey |

| 28/12/2022 | 1500/1000 | ** | | US | NAR pending home sales |

| 28/12/2022 | 1630/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 28/12/2022 | 1800/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.