Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

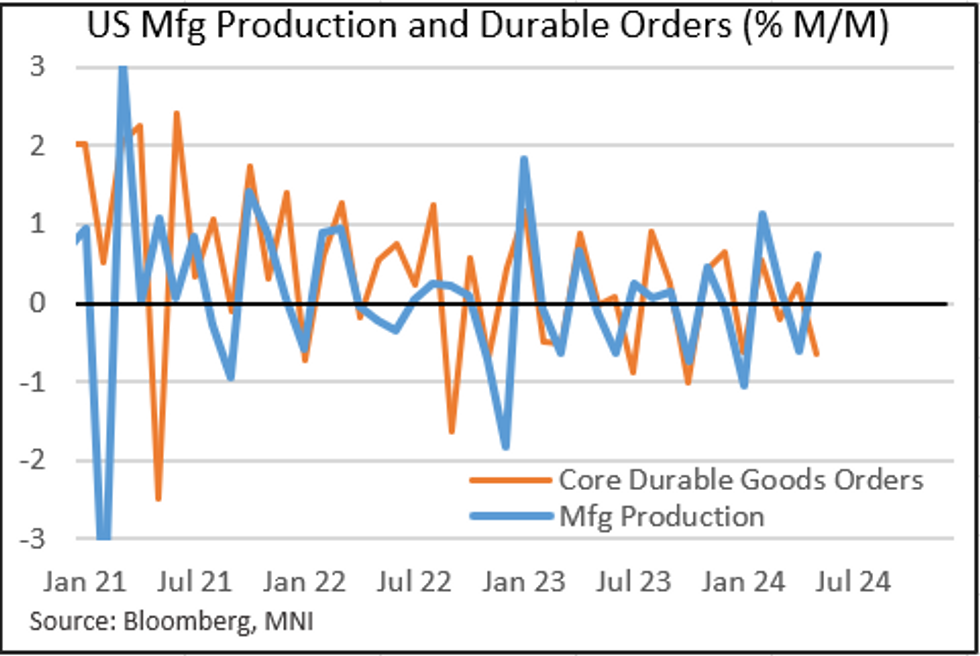

Factory orders were much weaker than expected in May, contracting by 0.5% vs +0.2% survey for the first decline in 4 months, and downward revisions to prior (0.4% Apr down from 0.7%).

- The 3M/3M annual run rate actually jumped to a 6-month high 3.9% , mostly reflecting the dropping out of the sharp declines at the start of 2024. But the level of SA factory orders is at levels seen previously in mid-2022, and mid-2023 - in other words, orders have been basically flat for a couple of years.

- Ex-transport factory orders came in at -0.7% M/M (after +0.5% in April), essentially flatlining over the last couple of years as well.

- The durable goods report was little changed in the final, with core capital goods orders confirming the 0.6% contraction in the advance report.

- With the May Shipments, Inventories and Orders data set in hand, business capex and goods output appears to be softening, reflected in contractionary ISM manufacturing readings and sub-0.5% Y/Y growth in industrial production.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok