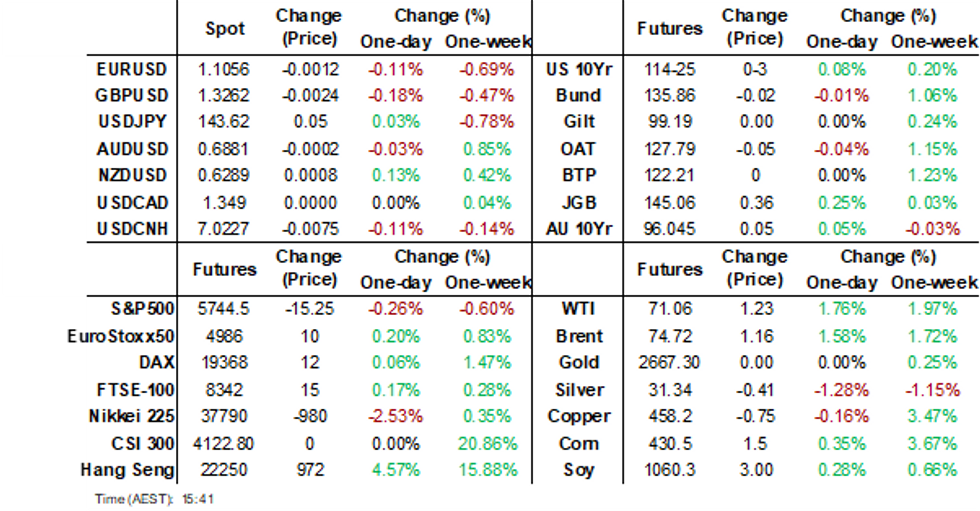

- Focus has been on potential Israel retaliation in the aftermath of Iran's missile attack. Nothing meaningful has eventuated at this stage, but headlines have crossed that Israel will strike back within days.

- This has curbed the earlier risk on feel to markets, as Hong Kong markets returned and continued to rally very strongly, amid China stimulus optimism. Oil prices are firmer, but haven't breached intra-session highs from Tuesday. US Tsys futures have traded in very tight ranges today.

- Looking ahead, we have some ECB speak, EU unemployment figures, while in the US the ADP report will be in focus. We also have further Fedspeak.

MARKETS

US TSYS: Tsys Futures Trade In Tight Ranges Ahead Of Jobs Data

- Tsys futures have traded in very tight ranges today TU is + 00⅞ at 104-06⅝, while TY is +02+ at 114-24+, there has been a small move higher over the past 30 minutes and we now trades near session highs.

- Headlines has been light today, with little coming out of the Vice Presidential debate. Looking at APAC markets, the focus again has all been on Hong Kong listed Chinese equities, with the BBG China Property Gauge surging over 30% on huge volumes.

- Cash tsys curve has done nothing today with yields all trading wrapped around unchanged for the session. The 2yr at 3.604% just off recent lows of 3.54%, while the 10yr is trading at 3.733%.

- Traders are reducing their bets on a further rally in US Treasuries, scaling back expectations of a half-point rate cut by the Fed in November. This unwind is ahead of the September jobs report out on Friday and follows comments from Powell suggesting a gradual approach to rate cuts.

- Projected rate cut pricing into year end gaining some momentum vs. this morning's levels (*): Nov'24 cumulative -34.9bp (-35.4bp), Dec'24 -70.8bp (-68.9bp), Jan'25 -102.3bp (-102.1bp).

- Focus will turn to MBA Mortgage Applications & ADP Employment Change later today

JGBS: Richer, BoJ Noguchi Speech & 10Y Supply Tomorrow

JGB futures are stronger but off session highs, +22 compared to settlement levels.

- Outside of the previously outlined monetary base, the market has had comments from Japan's new PM and his LDP team to digest.

- "I don't believe that we have completely overcome deflation at this point, and I still cannot deny the possibility of falling back" into deflation, Ryosei Akazawa, the minister in charge of economic revitalization, said at a news conference. (per BBG)

- Cash US tsys are slightly cheaper in today’s Asia-Pac session after yesterday’s haven-induced rally. The US calendar will see MBA Mortgage Applications and ADP Employment Change data later today. Nevertheless, the market will remain on Middle East headlines watch.

- Cash JGBs are richer across benchmarks beyond the 1-year, with yields 1-3bps lower. The benchmark 10-year yield is 2.6bps lower at 0.830% versus the cycle high of 1.108%.

- The swap curve has twist-steepened, pivoting at the 10-year, with yields 1bp lower to 4bps higher. Swap spreads are wider.

- The local calendar will see Jibun Bank Composite & Services PMIs tomorrow alongside 10-year supply. BoJ Board Noguchi will also give a speech in Nagasaki.

AUSSIE BONDS: Richer, Narrow Ranges, Focus On Middle East

ACGBs (YM +3.0 & XM +4.5) are stronger after dealing in narrow ranges in today’s Sydney session. With the domestic calendar empty today, the local market was on Middle East headlines watch.

- Cash US tsys are slightly cheaper, in today’s Asia-Pac session after yesterday’s haven-induced rally. The US calendar will see MBA Mortgage Applications and ADP Employment Change data later today.

- Cash ACGBs are 3-4bps richer with the AU-US 10-year yield differential at +23bps.

- Today’s ACGB Jun-35 auction once again demonstrated solid pricing, with the weighted average yield coming in below prevailing mid-yields and the cover ratio increasing to 3.7563x.

- TCorp issued A$500mn of its 3.00% 20 March 2028, 3.00% 20 April 2029 and 3.00% 20 February 2030 benchmark bonds via Yieldbroker tender. The auction was conducted on an exchange for a physical basis against the December bond futures contracts.

- The bills strip is slightly richer, with pricing flat to +1.

- RBA-dated OIS pricing is little changed across meetings. Nevertheless, 2025 meetings are 2-4bps firmer than pre-RBA levels. A cumulative 13bps of easing is priced by year-end.

- Tomorrow, the local calendar will see Judo Bank Composite & Services PMIs and Trade balance data.

AUSSIE BONDS: AU-US 10-Year Yield Differential Above Fair Value

Today, the AU-US 10-year cash yield differential is 2bps wider at +23bps.

- At +23bps, the differential is near the upper bound of the +/-30bps range observed since November 2022.

- However, a simple regression of the AU-US cash 10-year yield differential against the AU-US 1Y3M swap differential over the past 12 months indicates that the 10-year yield differential is around 6bps above fair value (i.e. +18bps).

- The 1y3m differential is a proxy for the expected relative policy path over the next 12 months.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: MNI – Market News / Bloomberg

BONDS: NZGBS: 44bps Of Easing Priced For RBNZ Next Week

NZGBs closed richer across benchmarks, with yields 1-3bps lower. Nevertheless, the local market finished well off the session’s best levels. With the domestic calendar empty today, the local market was on Middle East headlines watch following yesterday’s events.

- Cash US tsys are slightly cheaper, in today’s Asia-Pac session after yesterday’s haven-induced rally. The US calendar will see MBA Mortgage Applications and ADP Employment Change data later today.

- Swap rates closed flat to 1bps lower.

- RBNZ dated OIS pricing closed flat to 1bp softer across meetings, with 44bps or a 76% chance of a 50bp cut next week. The market is pricing in 92bps of cuts now by November.

- ANZ expects the RBNZ will cut the OCR by 50bps to 4.75% next week. “Now that most economists are calling it and the market is pretty much fully pricing it, one has to conclude that on balance the likeliest scenario is that the RBNZ will just take what’s on the table”. (per BBG)

- The calendar is light for the remainder of the week, with just ANZ Commodity prices tomorrow.

- Tomorrow, the NZ Treasury plans to sell NZ$250mn of the 1.50% May-31 bond, NZ$200mn of the 4.25% May-34 bond and NZ$50mn of the 1.75% May-41 bond.

ASIA: Asian Equities Mixed, HK Stocks Surge On Stimulus Measures

- Asian markets are trading with mixed results today, influenced by geopolitical tensions and optimism surrounding China’s economic recovery.

- Chinese shares listed in Hong Kong extended their rally as the HS China Enterprises Index climbed 7.25%, reflecting a bullish sentiment on the back of China’s stimulus measures, despite ongoing geopolitical concerns. Property stocks have been the top performing with BBG property gauge trading up 30% and now up 140% from the September lows, Tech stocks have also surged with HSTech Index up 8.50%

- Japanese equities are lower today as tensions mount in the Middle East and dampen demand for exporters, semiconductor stocks have seen the bulk of the losses with Tokyo Electron -2.45%, Advantest -3.50% & lasertec -3.40%. Investors are also cautious following the new prime minister being announced which saw equities sell off last week, while the yen holds onto recent gains which has been hurting exporters. The Topix is -0.75%, while the Nikkei is -1.45%

- Elsewhere, South Korea's KOSPI is little changed today with major tech stocks like SK Hynix and Samsung Electronics posting mixed performances. Foreign investors have been better sellers of local tech stocks today with total outflows of $233m. Australia's ASX 200 is also little changed today as gains in Metals & Mining stocks are offset by losses in Financials, Health Care & Real Estate stocks.

ASIA: Foreign Investors Sell Asian Equities

- South Korea: Market closed on Monday

- Taiwan: Saw outflows of $211m Monday, with the past 5 sessions netting +807m, while YTD flows are -12.21b. The 5-day average is +161m, above the 20-day average of -122m, but below the 100-day average of -132m.

- India: Saw outflows of $767m Friday, with the past 5 sessions netting +46m, while YTD flows are +24.03b. The 5-day average is +55m, below both the 20-day average of +313m and the 100-day average of +112m.

- Indonesia: Saw inflows of $33m Monday, with the past 5 sessions netting -476m, while YTD flows are +3.28b. The 5-day average is -95m, below the 20-day average of +69m, but above the 100-day average of +30m.

- Thailand: Saw outflows of $53m Monday, with the past 5 sessions totaling -196m, while YTD flows are -2.63b. The 5-day average is -39m, below the 20-day average of +44m, but above the 100-day average of -8m.

- Malaysia: Saw outflows of $15m Monday, with the past 5 sessions netting -161m, while YTD flows are +792m. The 5-day average is -32m, below both the 20-day average of +4m and the 100-day average of +11m.

- Philippines: Saw inflows of $8m Monday, with the past 5 sessions totaling +115m, while YTD flows are +30m. The 5-day average is +23m, above both the 20-day average of +17m and the 100-day average of +3m.

Table 1: EM Asia Equity Flows

FOREX: Hong Kong Equity Surge Drives FX Risk On

Risk appetite has recovered in the FX space, aided by a further surge in Hong Kong equity markets, which have returned after yesterday's break. NZD//USD is up close to 0.40%, while the A$ and NOK are both up 0.30%. Yen has underperformed, down 0.20%, steady trends have been evident elsewhere.

- Early focus was on the potential Israel response to the overnight missile launches from Iran. Further fighting has taken place in Lebanon, but Israel has not retaliated directly against Iran yet. Oil prices are up, but away from Tuesday intra-session highs.

- So lack of fresh meaningful further escalation has likely been welcomed by the market. Returning Hong Kong equity markets have been the other positive for FX risk appetite. The main headline HSI is up 6%, with strong gains in China-related sub indices. Property gauges continue to surge as Beijing became the latest major city to ease home buying restrictions.

- NZD/USD is back up to 0.6305, so 0.40% stronger for the session. A 50bps cut from the RBNZ next is rapidly becoming a consensus view, this hasn't weighed on NZD though. Market pricing for a 50bps cut is close to fully priced (around -44bps off implied OIS).

- AUD/USD has lagged NZD gains slightly, but is still back above 0.6900 level, so still within striking distance of recent highs just above 0.6940.

- Yen has lost ground, last near 143.80/25. Some selling interest in the pair appears above 144.00. Outside of the risk one tone from HK equities, commentary from new government officials has been in focus, with on-going caution around further BoJ rate hikes, including from new PM Ishiba. This looks to be in line with BoJ thinking.

- Looking ahead, we have some ECB speak, EU unemployment figures, while in the US the ADP report will be in focus.

OIL: Oil Price Steadies as Israel Retaliation Awaited

- Iran airstrikes on Israel steps up escalations in the region and represents one of the most significant attacks.

- It is reported that Iran fired as many as 200 ballistic missiles at Israel, though reports as to their effectiveness remain scarce.

- Whilst at this stage it appears (as with the attacks in April) the missiles were largely thwarted by Israel’s defence systems, the attack is a clear indication that tensions are escalating further.

- Oil is pricing off some earlier gains as the impact of Iranian missile strikes on Israel become clearer, but uncertainty surrounds the response.

- WTI approached US$72 in US trade but last tracked near $70.89 in by Asia Pac lunchtime.

- Brent too spiked on news of the missiles jumping as high as $75.40 before settling back at $74.50/55 in latest dealings.

- For WTI futures, key resistance remains at the 50-day EMA of $71.69, which is the key upside hurdle for bulls. A move lower would refocus attention on $64.61, the Sep 10 low and bear trigger.

- Israel’s Prime Minister Bejamin Netanyahu has vowed to retaliate stating that ‘Iran made a big mistake tonight and will pay for it.’

- US President Joe Biden has ordered the US military to continue to support the defence of Israel. US Naval destroyers were heavily involved in the firing of interceptors aimed at destroying the incoming missiles from Iran.

GOLD: Haven Buying Drives Solid Gain

Gold is slightly lower in today’s Asia-Pac session, after closing 1.1% higher at $2663.23 on Tuesday.

- Bullion benefited from a flight to safety as the markets monitored Israel's invasion of Southern Lebanon and Iran's missile attack on Israel.

- Geopolitical risks overshadowed yesterday's ISM Mfg miss and higher-than-expected job openings data.

- US job openings unexpectedly increased in August after two straight monthly decreases, but hiring was soft and consistent with a slowing labour market.

- The ISM’s manufacturing employment measure dropped to 43.9 from 46.0 in August. Its measure of prices paid by manufacturers decreased to 48.3, the lowest level since December 2023, from 54.0 in August.

- Gold has rallied nearly 30% this year, hitting a series of record highs.

- Recent gains have been fueled by anticipation of interest rate easing by the Federal Reserve, which last month kicked off its cutting cycle with a 50bp move.

- Lower rates are typically positive for gold, which doesn’t pay interest.

- According to MNI’s technicals team, the focus is on $2690.2 next, a Fibonacci projection. Firm support lies at $2589.8, the 20-day EMA.

METALS: Iron Ore & Copper Tracking Higher With China Property Optimism

Iron ore is tracking back towards $109/ton in terms of the active SGX contract. This leaves us short on intra-session highs from end Sep, ($113.55/ton), but sentiment is being aided by optimism around the China property market outlook. The 20-day EMA for iron ore is back sub $100/ton. Copper is back above $462 on a CMX basis, also short of late September highs, but likewise appears to have a positive technical backdrop.

- The return of Hong Kong markets, after yesterday's back, has seen the equity rally continue, with China property names the standout. A Bloomberg gauge of China property stocks is up over 100% from its recent lows.

- Beijing became the latest large city to ease property restrictions (from late yesterday). Commentary from CGS-CIMB per BBG noted: "New home sales in 30 key cities in China last week surged by 61%-106% w/w, an encouraging sign following policymakers’ proactive support for the sector"

- With China onshore markets still closed until next Tuesday, there may be lighter interest in iron ore. There is no steel futures trading in China either.

SOUTH KOREA: CPI Slips Below Target.

- Against a target of 2.0%, South Korea’s CPI printed today at 1.6% yoy for September.

- Korea is in a push pull environment with respect to interest rates with the Bank of Korea focused on the strength of house prices whilst the government is focused on the declining consumer sentiment (largely driven by rising house prices).

- The decline in CPI now provides the backdrop for a cut in rates. It is now with the BOK to decide whether they can cut rates without fuelling further growth in house prices in Seoul.

SOUTH KOREA: PMI Decline to Lowest in More Than a Year.

- South Korea’s PMI fell to 48.3 for September.

- This follows 51.9 in August and the lowest since June 2023.

- Output component the lowest in 1 year.

- New orders fell versus August.

- Following on from this morning’s CPI decline, this puts the next BOK meeting in play for a change in monetary policy.

SOUTH KOREA: Bond Wrap.

- Korean CPI fell below the BOK’s 2% target, leaving room for a potential cut in rates.

- Korean PMI moved to contraction, hitting lowest level since June 2023.

- Equity markets gave back recent gains as Middle East tensions drove risk aversion and the KOSPI 0.50% lower.

- Bonds reacted to the weaker data and growing tensions, with yields significantly lower across the curve.

2yr 2.806% (-6.5bp) 5yr 2.89% (-0.5bp) 10yr 2.942% (-9bp) 30yr 2.826% (-5bp)

INDONESIA: Bond Wrap.

- Risk aversion was evident today as Middle East tensions saw risk appetite diminished and equity markets down almost 1%.

- The IDR was impacted by the rush to USD assets as a safe haven.

- Bonds also were affected by risk aversion with bond yields higher across the curve.

2yr 6.178% (+0.5bp) 5yr 6.237% (+2bp) 10yr 6.477% (+1bp) 30yr 6.884% (+1bp)

ASIA FX: Won Rebounds With HK Equities, CNY & TWD Out

It has remained reasonably quiet in North East Asia FX, with China markets still closed and Taiwan markets also out today. South Korean markets have returned, but are out again tomorrow.

- Returning Hong Kong markets have given broader risk appetite a positive boost. The HSI is up 6% at the lunch time break, after stimulus optimism continues to buoy sentiment. Beijing is the latest city to announce easier property buying conditions. Property gauges in Hong Kong have surged today. One Bloomberg measure is more than 100% firmer from recent lows.

- The USD/CNH has moved lower as a result, but found some buying interest sub 7.0100. CNH hasn't been helped at the margins by higher USD/JPY levels.

- Spot USD/KRW has risen as on markets return, but is off earlier highs, the pair last near 1318 (earlier highs at 1323.6). The 1 month NDF was last near 1316, so around 0.50% stronger in won terms versus end Tuesday levels in the US. Local equities are down, but away from worst levels, (Kospi last -0.65%). The gains in HK and China-related indices providing some offset. On the data front, headline CPI was softer in September at 1.6%y/y, below the BoK's 2% target. Core inflation though was at 2.0%y/y, in line with the market's expectation. This should increase focus on next week's BoK meeting.

- The South Korean Sep PMI was also noticeably weaker (48.3, from 51.9 per S&P). This hints at a less supportive external backdrop.

ASIA FX: Spot Weakness Mostly Evident In SEA FX

In South East Asia FX, trends have been mixed, albeit with a mostly firmer USD backdrop. THB and MYR have lost a little more ground, although more so for the baht. IDR is also weaker in spot terms, although its 1 month NDF is little changed from NY closing levels suggesting today's spot move is catch up with weakness post yesterday's onshore close. The regional data calendar has been empty today.

- USD/THB sits close to session highs in latest dealings, last near 32.66. This is close to 0.25% weaker in baht terms. We are still comfortably sub key resistance levels which lie above 33.00. Local equities are weaker by around 0.65%, while offshore investors have sold both local equities and bonds since the start of the week.

- USD/MYR rests above 4.1600, but is only marginally weaker in MYR terms. Recent highs in the pair rest near 4.1800.

- UISD/IDR has pushed above 15240, around 0.30% weaker in IDR terms. The 1 month NDF is little changed though at 15265/70, so close to NY close levels from Tuesday trade.

- The market is awaiting Israel's response to the missile launches from Iran overnight. The return of Hong Kong equities, which have continued to surge, has provided some offset to such concerns and regional equity market weakness elsewhere.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 02/10/2024 | 0715/0915 |  EU EU | ECB's De Guindos speech at SUERF and Latvijas Bankas conference | |

| 02/10/2024 | 0730/0930 | EU | ECB's De Guindos in panel discussion on financial architecture | |

| 02/10/2024 | 0900/1100 | ** | EU | Unemployment |

| 02/10/2024 | 0900/1000 | ** |  GB GB | Gilt Outright Auction Result |

| 02/10/2024 | 0930/1130 | EU | ECB's Lane chairing policy panel at Joint BoC - ECB - NY FED Conference | |

| 02/10/2024 | 1100/0700 | ** |  US US | MBA Weekly Applications Index |

| 02/10/2024 | 1200/1400 | EU | ECB's Elderson participates in European Affairs Webinar | |

| 02/10/2024 | 1215/0815 | *** | US | ADP Employment Report |

| 02/10/2024 | 1300/0900 | US | Cleveland Fed's Beth Hammack | |

| 02/10/2024 | 1430/1030 | ** | US | DOE Weekly Crude Oil Stocks |

| 02/10/2024 | 1500/1100 | US | Fed Governor Michelle Bowman | |

| 02/10/2024 | 1615/1215 | US | Richmond Fed's Tom Barkin | |

| 02/10/2024 | 1645/1845 | EU | ECB's Schnabel Walter Eucken Lecture |