Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

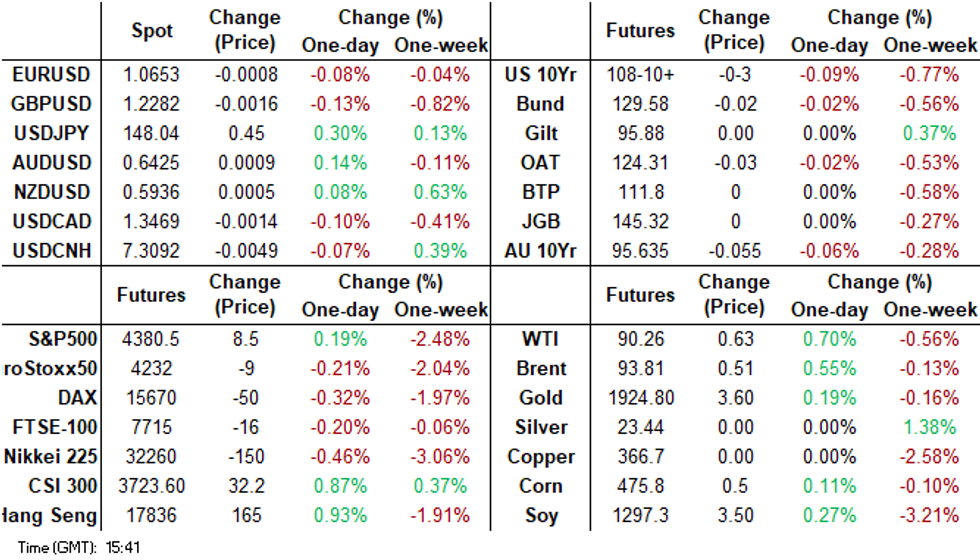

- The BOJ delivered arguably a dovish hold today. All major policy parameters were left unchanged, as was the forward guidance. The BoJ described the outlook as extremely uncertain. Focus now shifts to Governor Ueda's press conference in a little while.

- Yen is the weakest performer in the G-10 space at the margins, back near 148.00, but remains sub Thursday highs. JGB futures spiked to a fresh Tokyo session high in the early rounds of the afternoon session. However, those gains were unwound. US 10yr yields edged above 4.50% in early trade, making fresh cyclical highs, but sit slightly lower now in yield terms.

- In the equity space, sentiment has stabilized somewhat, particularly in HK and China. This has helped the likes of AUD and some Asian FX.

- Looking ahead, retail Sales from the UK provides the highlight in Europe today. Further out we have flash S&P Global PMIs, as well as Fedspeak from Gov Cook, SF Fed President Daly and Minneapolis Fed President Kashkari.

MARKETS

US TSYS: Narrow Ranges In Asia

TYZ3 deals at 108-11+, -0-02, a 0-04+ range has been observed on volume of ~105k.

- Cash tsys sit little changed across the major benchmarks.

- Tsys have observed narrow ranges with little follow through on moves through a muted session in Asia today.

- There was a brief move lower however support came in ahead of yesterday's lows and losses were pared.

- The space looked through the latest BOJ monetary policy decision.

- Retail Sales from the UK provides the highlight in Europe today. Further out we have flash S&P Global PMIs, as well as Fedspeak from Gov Cook, SF Fed President Daly and Minneapolis Fed President Kashkari.

ECB: ECB's Lane - Policy To Stay Restrictive For As Long As Necessary

ECB Chief Economist Philip Lane has stated, during a speech in NY, that the central bank will keep rates sufficiently restrictive for as long as necessary to achieve the 2% inflation objective in the medium term. He noted "The high level of two-sided uncertainty around the baseline means that we will remain data dependent in determining the appropriate level and duration of restrictiveness in our monetary stance.”

- Watch points for the central bank are wages and profit dynamics. There are signs that firms are absorbing rising wage pressures, which is a process that will have to continue for further disinflation in 2024.

- Lane wouldn't speculate on future balance sheet policy. Policy tightening is impacting the economy, particularly housing and business investment, but lag effects meant there was still considerable tightening to come.

JGBS: Post-BOJ Decision Spike In Futures Unwound

JGB futures spiked to a fresh Tokyo session high in the early rounds of the afternoon session after the arguably dovish hold by the BOJ. However, those gains were unwound. JBZ3 is currently holding an uptick, +2 compared to settlement levels.

- The BOJ kept all the policy parameters unchanged. The policy rate stays at -0.1%, 10yr yield target around 0%, with a -/+0.50% band on this and a firm cap at 1.0%, which was introduced at the last policy meeting in July. Forward guidance was also unchanged, with the central bank maintaining its easing stance until the 2% inflation target is achieved in a stable manner. It will also not hesitate to take additional easing measures if necessary.

- Focus now shifts to Governor Ueda's press conference, (1530 Tokyo time, 0730 BST), particularly in light of his recent media interview, which came across as hawkish, but the ruling party pushed back on this notion (see this link for more details).

- The cash JGB curve has unwound the twist flattening seen early in the afternoon session to be slightly cheaper across the curve. The benchmark 10-year yield is 0.2bp higher at 0.745% versus the fresh post-YCC tweak high of 0.756% seen earlier in the session.

- Swap rates are lower out to the 30-year, with pricing 0.2bp to 1.5bps lower. Swap spreads are tighter across maturities.

- Next week the local calendar sees Dept Sales on Monday and PPI Services on Tuesday. BOJ Minutes for the July Meeting, Leading and Coincident Indices and Machine Orders are on Wednesday. The MOF plans to sell Y700bn of 40-year JGBS on Tuesday.

BOJ: Dovish Hold

The BOJ delivered arguably a dovish hold today. The central bank kept all the policy parameters unchanged. The policy rate stays at -0.1%, 10yr yield target around 0%, with a -/+0.50% band on this and firm cap at 1.0%, which was introduced at the last policy meeting in July. Forward guidance was also unchanged, with the central bank maintaining its easing stance until the 2% inflation target is achieved in a stable manner. It will also not hesitate to take additional easing measures if necessary.

- The central bank described the economic recovery as moderate and expects it to stay that way. Pent up domestic demand is a positive, but slowing external conditions are a downside risk the other way.

- CPI y/y (ex fresh food) is expected to moderate further as pass through from higher import costs are expected to wane. Beyond this, price pressures are expected to accelerate modestly, as the output gap improves and longer term inflation and wage expectations firm.

- The BoJ noted extremely high uncertainties regarding both the economic and price outlook. This reflects overseas demand, commodity prices and domestic price and wage setting behavior. The BoJ noted that this backdrop meant attention needs to be paid to developments in financial and FX markets and their impact on Japan's economy and inflation.

- Focus now shifts to Ueda's press conference, (3:30pm Tokyo time, 07:30 BST), particularly in light of his recent media interview, which came across as hawkish, but the ruling party pushed back on this notion (see this link for more details).

JAPAN DATA: Transport & Higher Services Inflation Offset Further Utilities Dip

Japan's national August CPI was a touch firmer than expected. The headline printed at 3.2% y/y, versus 3.0% forecast (3.3% prior). The ex fresh-food measure rose 3.1% y/y, versus 3.0% forecast and 3.1% prior. The core measure (ex fresh-food and energy) was as expected at 4.3% y/y, which was also the prior outcome.

- The series that excludes all food and energy was also steady in y/y terms at 2.7%, the same as the July outcome.

- In terms of the detail, good prices rose 0.3% m/m (0.5% prior), while services inflation ticked up to 0.1% m/m from flat in July.

- Food prices rose in m/m terms, but were down from the July pace. Utilities (-2.3%m/m), household goods (-0.8%m/m) and clothing, footwear (-0.8% m/m) were the main drags. Offsets came from transport and communication (+1.0% m/m) and entertainment (+1.8% m/m).

- In y/y terms the biggest drag remains from utilities, -12.3% y/y. Food inflation remained elevated at 8.6% y/y, while transport and entertainment saw further gains in y/y terms.

JAPAN DATA: Offshore Investors Dump Japan Equities

The highlight from Japan's weekly investment flow data (ending September 15th) was sharp selling of local equities by offshore investors. There were -¥1583.9bn in outflows, the largest since 2019. This build on outflows from the week prior of -¥851.8bn. Offshore investors have now sold local stocks in 4 out of the past 5 weeks. Both the TOPIX and Nikkei hit recent peaks at the end of last week and have fallen sharply this week, although a more hawkish Fed backdrop has been a driving factor as well.

- Offshore investors purchased Japan bonds, +¥439.4bn, up on the prior week's modest inflow.

- In terms of Japan outflows, local investors bought ¥885.5bn of offshore bonds, down from the prior week's sharp outflow. Local investors also purchased offshore stocks but at tepid pace of ¥62.6bn.

Table 1: Japan Weekly Investment Flows

| Billion Yen | Week ending September 15 | Prior Week |

| Foreign Buying Japan Stocks | -1583.9 | -851.8 |

| Foreign Buying Japan Bonds | 439.4 | 83.7 |

| Japan Buying Foreign Bonds | 885.5 | 3631.5 |

| Japan Buying Foreign Stocks | 62.6 | 96.8 |

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Cheaper, Narrow Ranges, Tracking JGBS & US Tsys, CPI Monthly Next Wednesday

ACGBs (YM -1.0 & XM -5.5) are cheaper after dealing in a relatively narrow range during the Sydney session. With the domestic calendar light (Judo Bank preliminary PMIs only data), local participants have been on headlines, JGBs and US tsys watch.

- JGBs pared US tsy-linked morning weakness into the BOJ policy decision. The arguably dovish hold by the BOJ saw JGB futures spike higher in the early rounds of the Tokyo afternoon session. However, those gains have been unwound. The market now awaits BOJ Governor Ueda’s press conference at 3:30pm Tokyo time, 07:30 BST.

- After pushing to multiyear highs on Thursday, long-dated US tsys are dealing little changed in Asia-Pac trade.

- Cash ACGBs are 1-5bps cheaper, with the AU-US 10-year yield differential 1bp lower at -14bps.

- The 3s10s swap curve has twist-steepened, with rates 2bp lower to 4bps higher. EFPs are tighter.

- The bills strip is richer, with pricing +1 to +2

- Next week the local calendar is light until the release of the CPI Monthly for August on Wednesday.

- Monday sees panel participation by RBA Assistant Governor Jones at a Conference on Financial Technology, Climate Change, and Challenges.

- Next Wednesday the AOFM plans to sell A$800mn of the 2.25% May-28 bond.

NZGBS: Closed With A Twist Flattening Of the Curve

NZGBs closed with a twist-flattening of the 2/10 curve. Benchmark yields closed 1bp lower to 2bps higher. NZGBs opened on a weaker note, influenced by the negative performance of US tsys during the NY session. However, they rebounded from their session cheaps as JGBs rallied in anticipation of the BOJ’s policy decision.

- However, the local market couldn't sustain its best levels either, primarily due to a paring of JGB gains after the BOJ decision.

- US tsys have probed their NY session lows in Asia-Pac trade, although ranges have been narrow.

- Nevertheless, it's worth noting that NZGBs outperformed their counterparts in the $-bloc, with the NZ-US and NZ-AU 10-year yield differential 3-4bps lower.

- The swaps curve has twist-flattened at the close, with rates 3bps lower to 2bps higher.

- RBNZ dated OIS pricing closed little changed.

- NZ's trade deficit widened to NZ$2.291bn in August from a revised NZ$1.177bn in July. Exports to China declined 5.8% m/m (-18% y/y), while exports to Australia rose 1.3% m/m (-9% y/y).

- Next week the local calendar is empty until ANZ Business Confidence on Thursday.

- Next Thursday the NZ Treasury plans to sell NZ$225mn of the 3.0% Apr-29 bond, NZ$200mn of the 4.25% May-34 bond and NZ$75mn of the 2.75% May-51 bond.

FOREX: Yen Pressured In Asia

The Yen is the weakest performer in the G-10 space at the margins. The BOJ left policy unchanged and left its forward guidance unchanged, arguably delivering a dovish hold.

- USD/JPY prints at ¥148.15/20, the pair is ~0.4% firmer today. Technically the uptrend remains intact, resistance comes in at ¥148.60, 2.236 projection of the Jul 14-21-28 price swing.

- AUD/USD is a touch firmer, the pair was supported ahead of $0.64 in early trade and last prints at $0.6425/30. The trend condition is unchanged and remains bearish. Support comes in at $0.6357, low from Sep 6 and bear trigger.

- Kiwi is marginally firmer however narrow ranges have persisted for much of todays session. NZD/USD last prints at $0.5935/40.

- Elsewhere in G-10; EUR and GBP are a touch lower. NOK is the strongest performer in the G-10 space however liquidity is generally poor in Asia.

- Retail Sales from the UK provides the highlight in Europe today.

EQUITIES: HSI Bounces Off August Support Levels, Japan Equities Off Lows As BoJ Holds Steady

Asia Pac equities are mixed so far in Friday trade. This comes despite negative leads from US and EU markets through Thursday trade. US futures have recovered some ground, but are only modestly higher at this stage. Eminis were last near 4380, around +0.17% higher, while Nasdaq futures were +0.23% firmer. Eminis are only a touch above fresh lows going back to early June this year.

- Positive sentiment has been evident in terms of both Hong Kong and China equities. HK markets opened weaker, but at the break the HSI sits +1.20% firmer, with the tech sub-index +2.39% higher at this stage, tracking for its first gain this week.

- The HSI appeared to find some support around the 17570/80 region, which was also close to August lows.

- The CSI is also firmer, +1.0% higher to the break, with the index back above 3700. Further efforts to boost private economy development have been highlighted by the regulator, which was also something the Premier spoke about yesterday. Another focus point has been efforts in Beijing and Shanghai to allow the free-flow of foreign investor funds (see this link for more details).

- Japan stocks are down, last off -0.20% in terms of the Topix, but we are above session lows. The yen is weaker post the on hold BoJ outcome, which is aiding exporter related stocks.

- Other markets aren't showing strong trends. The Taiex is around flat, the Kospi modestly higher. In SEA Indonesian and Philippine bourses are both in the green at this stage.

OIL: Weekly Losses Pared

Brent crude is firmer in the first part of Friday dealing, last near $93.90/bbl. This is a ~0.60% gain, and puts us close to unchanged on levels at the end of last week. WTI is back to $90.35/bbl, a +0.80% gain, although this is still modestly down on last Friday closing levels ($90.77/bbl).

- Risk appetite has stabilized somewhat in the equity space, with US futures ticking higher and HK/China markets firmer. This has likely helped oil at the margins.

- The other focus point has been Russia's diesel and gasoline export ban. This threatens an already tight supply backdrop. However, some supply side analysts, including those from J.P. Morgan, expect the ban to be short lived.

- The US is also pressing Iraq to re-open the Iraq-Turkey crude pipeline as soon as possible.

- For Brent, the 20-day EMA sits back near $90.74/bbl, while recent highs rest near $96/bbl.

LNG: Union To End Strike Action At Chevron Facilities In Australia

Chevron and labor unions have reached a deal to end strikes at two LNG facilities in Australia. The Union stated workers have accepted an agreement put forward by the country's Labor Market regulator. Chevron had accepted the terms on Thursday.

- The Labor Union stated it will cease strike action at the facilities, which had started on September 8 and ramped up recently to 24 hour work stoppages.

- The Gorgon and Wheatstone facilities, which were impacted by the industrial action, accounted for around 7% of global LNG supply last year.

- This should help allay global supply fears, at the margin, as we head into the northern hemisphere winter period.

GOLD: Back-To-Back Declines For Bullion As Long-Dated Yields Push Higher

Gold is +0.3% in the Asia-Pac session, after closing -0.5% at $1920.02 on Thursday. Bullion came under pressure from a sizeable twist steepening of the US Treasury curve with longer-dated yields up strongly. The 30-year bond’s yield rose 13bps to 4.57%, its highest level since 2011. The 10-year approached 4.5%, last seen in 2007.

- While the Bank of England followed the US Fed with a hawkish hold, stronger labour markets and persistent inflation raise the prospect of rates remaining higher for the foreseeable future.

- Bloomberg reports that Oanda analyst Edward Moya said the peak in US Treasury yields is almost here, but until recession risks become the base case for the US, the precious metal might struggle to stabilise.

- From a technical standpoint, Thursday’s close was a significant retracement off yesterday’s pre-FOMC high of $1947.5, although the low of $1913.98 didn’t test support at $1901.1 (Sep 14 low).

- With climate-related disruptions accelerating, the metal will almost certainly remain a safe haven during rough times, according to analysts at HSBC Global Research. (See link)

INDIA: Government Bonds To Be Included In J.P. Morgan GBI-EM Index In 2024

J.P. Morgan announced that Indian bonds will be included in its GBI-EM index from mid next year. Inclusion in the index will start on June 28th 2024 and extend over the next 10 months. India's weighting is expected to reach a maximum of 10% (going up in 1% increments over this 10 month period).

- J.P. Morgan notes $236bn in funds track the GBI-EM index. 23 Indian Government Bonds with a combined notional value of $330bn are eligible. These bonds fall under the category of fully accessible for offshore investors.

- Speculation will now be around whether other bonds indices also add Indian government bonds to their respective indices.

- So far this year there has been much stronger inflows into Indian equities, nearly $16bn, while net bond inflows have been close to +$3.5bn.

- USD/INR sits just below record highs but has outperformed most other Asian FX so far this year. Currency strength tends to more closely aligned with equity inflows than bond inflows though, with a tendency for offshore investors to hedge equity exposure less.

ASIA FX: USD/Asia Pairs Lower, INR Firms On Debt Index Inclusion

USD/Asia pairs are mostly lower in the first part of Friday trade. A more resilient regional equity backdrop has helped, while US yields haven't been able to hold earlier gains, which has been another positive. INR is modestly firmer as J.P. Morgan announced it will include the country's government bonds in its EM debt index from mid next year. 1 month USD/KRW continues to find selling interest above 1340.

- USD/CNH got to lows of 7.2957, after opening near 7.3140. Supports have come from an equity rebound, a record fixing support (relative to expectations) and reports of state bank USD selling and reduced CNH liquidity. We sit slightly higher now, last near 7.3075, with HK and China equities slightly away from best levels.

- 1 month USD/KRW is down from Thursday highs above 1342. The pair last sat at 1333/34, around 0.40% stronger in won terms versus NY closing levels. Resistance above 1340, which is also where the pair topped out in August, has again been apparent. Local equities are weaker, but at -0.35%, haven't fallen as much as implied by tech weakness elsewhere.

- USD/HKD has seen some support emerge in the past week. Spot sits back near 7.8190 in recent dealings. This is against early highs from yesterday just above 7.8260. We are above lows from earlier in the week though near 7.8140. We are below all key EMAs with the majority clustered near the 7.8280/90 region, while the 200-day sits just above 7.8300. US-HK rate differentials, at the short end have stabilized somewhat in recent sessions, with Wednesday's hawkish Fed outcome helping at the margins. The 3 month differential is around +22bps, we were near +100bps at the turn of the month. The 3 month Hibor fix was steady at 5.22% today, the 1 month at 5.23%.

- Rupee has firmed in early dealing, USD/INR is down ~0.2% and has breached its 20-Day EMA (82.96). The pair sits at 82.91/92. JPMorgan Chase & Co. will add Indian government bonds to its benchmark emerging-market index, a keenly awaited event that could drive billions of foreign inflows to the nation’s debt market.

- USD/MYR is consolidating recent gains in narrow ranges today, the pair has risen ~4.2% since the start of August and printed a fresh YTD high yesterday. In early dealing today the pair is marginally lower, last printing at 4.6860/90. CPI in August came in as expected at 2.0% Y/Y.

- The SGD NEER (per Goldman Sachs estimates) is little changed in early dealing on Friday, the measure sits well within recent ranges and is ~0.6% below the top of the band. Broader USD flows dominated yesterday as the hawkish hold from the Fed saw USD/SGD extend recent gains to print a fresh YTD high. Looking ahead; the next data of note is Monday's August CPI print. Headline CPI is forecast to tick lower to 3.9% Y/Y and core CPI is expected to ease to 3.5% Y/Y from 3.8%.

- USD/PHP sits modestly lower, last under 56.80. We remain within recent ranges. The PHP didn't receive much support earlier, when BSP Governor Remolona stated there was a good chance of a November rate hike. He did state FX wasn't the overriding concern in terms of warranting tighter policy. Focus remains supply side pressures.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 22/09/2023 | 0600/0700 | *** |  | UK | Retail Sales |

| 22/09/2023 | 0700/0900 | *** |  | ES | GDP (f) |

| 22/09/2023 | 0715/0915 | ** |  | FR | S&P Global Services PMI (p) |

| 22/09/2023 | 0715/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 22/09/2023 | 0730/0930 | ** |  | DE | S&P Global Services PMI (p) |

| 22/09/2023 | 0730/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 22/09/2023 | 0800/1000 | ** |  | EU | S&P Global Services PMI (p) |

| 22/09/2023 | 0800/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 22/09/2023 | 0800/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 22/09/2023 | 0830/0930 | *** | | UK | S&P Global Manufacturing PMI flash |

| 22/09/2023 | 0830/0930 | *** | | UK | S&P Global Services PMI flash |

| 22/09/2023 | 0830/0930 | *** | | UK | S&P Global Composite PMI flash |

| 22/09/2023 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 22/09/2023 | 1100/1300 | | EU | ECB's de Guindos Speaks at Event | |

| 22/09/2023 | 1230/0830 | ** |  | CA | Retail Trade |

| 22/09/2023 | 1250/0850 |  | US | Fed Governor Lisa Cook | |

| 22/09/2023 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 22/09/2023 | 1345/0945 | *** | | US | S&P Global Services Index (flash) |

| 22/09/2023 | 1400/1000 | | US | Boston Fed's Susan Collins | |

| 22/09/2023 | 1700/1300 | | US | San Francisco Fed's Mary Daly | |

| 22/09/2023 | 1700/1300 | | US | Minneapolis Fed's Neel Kashkari |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.