Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

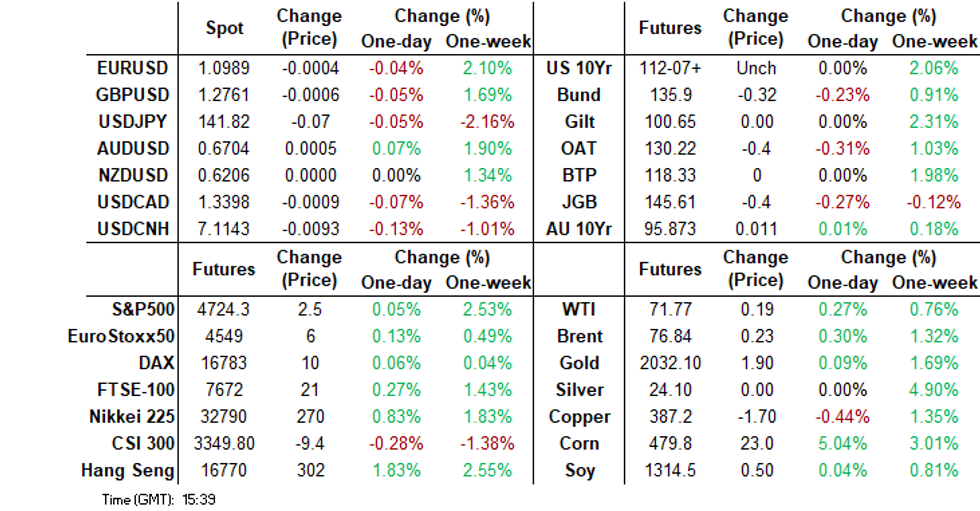

- USD sentiment stabilized somewhat in early trade, as US Tsy futures moved off recent highs. However, there was little follow through and the market was happy to fade USD upticks.

- Regional equities were buoyed by China easing property curbs, which was announced late yesterday, while the MLF injection added liquidity support. Still, aggregate China indices have struggled to hold gains. USD/CNH got close to 7.1000 before rebounding.

- Elsewhere, oil is tracking for its first weekly gain since October.

- Looking ahead, we have PMIs on tap for the UK and EU. In the US, the calendar sees Empire Manufacturing, Industrial Production, Flash S&P Global US Manufacturing PMIs and TIC Flow data. Fed's Williams is also due to speak on CNBC.

MARKETS

US TSYS: Profit Taking After A Massive Post-FOMC Rally

TYH4 is trading at 112-12+, -0-04 from NY closing levels.

- So far today, there has been no noteworthy news flow.

- Cash US tsys are sitting 3bps cheaper so far in the Asia-Pac session, with local participants possibly profit-taking following an assertive post-FOMC rally.

- Considering that the US STIR market has priced 130bps of easing by November 2024, compared to the dot plot median easing of 75bps for 2024, a cautious view towards the near-term outlook for the market probably makes sense.

- Later today the US calendar sees Empire Manufacturing, Industrial Production, Flash S&P Global US Manufacturing PMIs and TIC Flow data. Fed's Williams is also due to speak on CNBC.

JGBS: Cheaper Across The Curve, BOJ Policy Decision Next Tuesday

JGB futures are holding cheaper, -38 compared to the settlement levels, and marginally above the session’s worst level.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Flash Jibun Bank PMIs. The Tertiary Industry Index has recently printed -0.8% m/m in October versus a +0.1% estimate and a revised -1.2% prior.

- Cash US tsys are sitting 3bps cheaper so far in the Asia-Pac session, with local participants possibly profit-taking following an assertive post-FOMC rally. Considering that the US STIR market has priced 130bps of easing by November 2024, compared to the dot plot median easing of 75bps for 2024, a cautious view towards the near-term outlook for the market probably makes sense.

- Cash JGBs are cheaper, with the futures-linked 7-year (3.5bps higher) underperforming. The benchmark 10-year yield is 2.7bps higher at 0.701%. The 20-year is 3.4bps higher at 1.437% versus yesterday’s pre-auction low of 1.36%.

- Swap rates are 1-4bps higher across maturities.

- On Monday, the local calendar is empty, ahead of the BOJ Policy Decision on Tuesday. While certain investors interpreted recent statements from BOJ officials as a sign of an imminent policy shift, we are inclined to view it as a step in the extended process of preparing for a seamless transition.

- The BOJ will also conduct Rinban operations covering 1- to 25-year JGBs on Monday.

AUSSIE BONDS: Cheaper, Light Calendar, Subdued Session, RBA Minutes On Tuesday

ACGBs (YMH4 -3.8 & XMH4 -0.9) are cheaper and near Sydney session lows after a subdued data-light local session. With US tsys paring their post-FOMC gains in today’s Asia-Pac session, local participants appear to have been content to sit on the sidelines. Considering that the market has priced 130bps of easing by November 2024, compared to the dot plot median easing of 75bps for 2024, a cautious view towards the near-term outlook for the market makes sense. Cash US tsys are currently dealing 3-4bps cheaper.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Judo Bank Flash PMIs.

- Cash ACGBs have reversed early strength to be 1-4bps cheaper, with the 3/10 curve flatter and the AU-US 10-year yield differential 2bps wider at +19bps.

- Swap rates are 2-5bps higher, with EFPs tighter.

- The bills strip has cheapened, with pricing -4 to -6.

- RBA-dated OIS pricing is 2-6bps firmer across meetings, with 57bps of easing priced by Feb’25.

- The local calendar is empty on Monday, ahead of the RBA Minutes for the December Policy Meeting on Tuesday.

- The AOFM plans to provide further details on issuance plans (including any new planned bond lines) for the second half of 2023-24 on 5 January 2024.

NZGBS: Closed Little Changed, Narrow Ranges

NZGB benchmarks closed little changed after dealing in narrow ranges in today’s local session. Following a positive lead from US tsys overnight, which extended their post-FOMC rally, there has been a slight cheapening of 3-4 basis points in today's Asia-Pac session. Local participants may be engaging in profit-taking after the robust post-FOMC rally.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined manufacturing PMI.

- Swap rates closed flat to 5bps higher, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed 1-4bps firmer across meetings. The market still has 100bps of easing priced by Nov’24.

- "We think it’s likely, absent any further surprises, that the RBNZ will revert to something like their August 2023 view that the OCR will remain at 5.5% until the latter part of 2024. We continue to see them as remaining much more cautious than markets on the prospects for lower rates. All going well, we can see a path to where they get that confidence by the time of the August 2024 Monetary Policy Statement.": Westpac

- On Monday, the local calendar sees Westpac Consumer Confidence and the Performance Services Index.

FOREX: Dollar Upticks Sold, A$ Outperforms Modestly

Dollar upticks have generally been sold through Friday's Asia Pac session. The BBDXY last tracked just under 1221, which is right on Thursday lows for the index. Earlier highs were at 1223.60.

- Some early USD support was evident, as US TSY futures ticked lower. This saw USD/JPY get back to 147.47, but we now sit back at 141.85/90. There wasn't much follow through to the US Tsy move. Cash US Tsys sit around 3-4bps firmer in yield terms.

- Elsewhere, Japan FinMin Suzuki stated its important FX markets reflect fundamentals and that FX moves are being watched closely. The comments didn't impact FX sentiment.

- AUD/USD has grinded higher, last near 0.6720, up 0.30% for the session. The better tone to Hong Kong and China equities, following property easing measures and more liquidity support have been A$ positives.

- NZD/USD is trailing modestly but still higher, last in the 0.6215/20 region. Both currencies remain sub early Thursday highs.

- EUR/USD hasn't been able to meaningfully breach the 1.1000 handle.

- Looking ahead, we have PMIs on tap for the UK and EU, likewise for the US later.

EQUITIES: Property Support Aids HK/China Market Rebound

Regional Asia Pac equities are up strongly across most of the major markets. Hong Kong markets are the standout (+3% for the HSI), as China easing housing restrictions late yesterday. US equity futures have ticked higher as the session has progressed, albeit ranges have been fairly tight. Eminis were last near 4779, +0.10%, while Nasdaq futures were 0.16% higher.

- At the break, Hong Kong's HSI is +3% higher, slightly down from session best levels. The mainland properties sub index is up nearly 4.7%.

- China announced late yesterday easing curbs for housing markets in both Beijing and Shanghai, (see this link for more details). Elsewhere as expected the 1yr MLF rate was held steady at 2.5%, but we saw larger liquidity injection (800bn yuan). Nov activity data was mixed.

- The latest piece from the MNI China Policy team suggests a growth target of around 5% next year, with a narrower fiscal deficit compared to this year (see this link).

- The CSI 300 is up nearly 0.7% to the break, also off session highs.

- The Kospi is +0.80%, away from session bests, while the Taiex is only just above flat at this stage. Japan's Nikkei 225 has rebounded, up nearly 1.2%.

- The ASX 200 is up nearly 1%, led by the materials sector following firmer commodity prices.

- In SEA, most markets are higher, with the Thailand SET rebounding further (+1.25%).

OIL: Set For The First Weekly Gain Since October

Oil has built on Thursday's impressive rally, with gains extending in the first part of Friday trade. Brent crude was last just above $77/bbl, +0.57% higher for the session. At this stage we are tracking +1.60% firmer for the week, which would be the first gain since mid October. For WTI we were last near $72/bbl (tracking +1% firmer for the week).

- The sharp USD sell-off, along with the plunge in US yields in the past week, has clearly aided the oil recovery. Firmer risk appetite in the equity space has also been a positive.

- On the demand outlook, global oil demand growth forecast for 2024 has been revised up by 130kbpd to 1.1mbpd. Still, expectations for this year’s demand growth have been lowered as the weakening economic climate is slowing down oil demand growth, according to the IEA Monthly Oil Market Report.

GOLD: Primed For A Weekly Gain After FOMC’s Change Of Heart

Gold is little changed in the Asia-Pac session, after closing 0.4% higher at $2036.36 on Thursday.

- Bullion is headed for a weekly gain after the Federal Reserve sent its strongest indication yet that it will pivot to easing monetary policy next year. While the Fed held the funds rate steady, as expected, Fed Chair Powell delivered little to no pushback to market expectations of significant rate cuts next year.

- The Dot Plot pointed to a 2024 median of 75bp of rate cuts, a sharper pace than indicated in September’s projections, with reductions expected by 17 of 19 members.

- US Treasuries extended their post-FOMC rally on Thursday on heavy volume. The 10-year yield fell to a 5-month low of 3.88%.

- That said, cash US Treasuries are sitting 3-4bps cheaper so far in the Asia-Pac session, with local participants possibly profit-taking following an assertive post-FOMC rally.

- According to MNI’s technicals team, recent strength in gold has signalled the end of the corrective Dec 4-13 pullback. A continuation higher would signal scope for a climb toward key resistance and the Dec 4 all-time high at $2135.39.

CHINA DATA: House Price Falls Broadened In November

China's Nov home sale prices were -0.37% m/m, very close to October's -0.38% (BBG). New home prices in y/y terms were -0.7%, versus -0.6% in Oct (BBG).

- The number of cities were there was a fall in new home prices (in m/m terms) was 59, versus 56 in Oct. Only 9 cities recovered a rise in new home prices (versus 11 in Oct). For existing homes, 69 cities saw a decline in existing home prices (67 in Oct).

- By major city, Shanghai was the only bright spot, seeing a 0.6%m/m rise in new home prices, while Beijing and Shenzhen saw falls. All of these cities saw a fall in existing home sale prices in m/m terms.

- Housing developments will remain a key focus point. We had easing restrictions for first home buyers in Beijing and Shanghai announced yesterday.

- Coming up soon we get Nov activity data, along with property investment/sales updates.

- The 1yr MLF was held steady at 2.50% but the net injection was noticeably stronger at 800bn Yuan.

ASIA FX: USD/CNH Gets Close To 7.1000, KRW & IDR Lag Somewhat

USD/Asia pairs are lower across the board, albeit to varying degrees. The KRW 1 month NDF is underperforming modestly, likewise for spot IDR (despite the continued sharp pull back in US real yields). USD/CNH has broken to fresh multi month lows sub 7.1100. Equity sentiment is mostly positive in the region, while USD upticks have been faded against the majors. Still to come today is Nov India trade figures.

- USD/CNH's down move has only gained traction in the second half of the Asia Pac Friday session. Earlier highs were at 7.1321. Onshore equities are higher, while HK's bourse surged +3%, amid easing property curbs (announced late yesterday) and a fresh liquidity support via the MLF (the MLF rate was held steady). Onshore equities have struggled somehwat though. Mixed Nov activity data was largely ignored. For USD/CNH we currently track near 7.1100, just above session lows (7.1030). A clean move lower could see early June lows at 7.0670 targeted.

- The 1 month USD/KRW NDF hasn't been able to get back sub 1290 in any meaningful way. The won has underperformed broader higher beta FX gains, and continued offshore equity inflows (+$464.6mn). The Kospi is just off multi month highs (last +0.70%).

- Spot USD/THB is back sub 35.00 but not at fresh lows for Dec. The pair continues its recent high vol run (earlier highs this week were near 35.84). Equities are continuing to recover from recent lows, while offshore investors added $100mn to local shares yesterday. Dec as a whole still remains negative from a flow standpoint. Bond outflows have also been recorded in Dec to date.

- USD/IDR spot has struggled to see much meaningful downside, the pair last at 15485. The rupiah has underperformed the pull back in US real yields post the Fed this week. Nov trade figures were close to expectations. The trade surplus at $2412m ($2970mn forecast). IDR bulls will target a move back sub 15400 to late Nov lows.

- USD/PHP maintains its low beta with respect to overall USD moves. The pair is down modesty to 55.65/70 today, around 0.20% firmer in PHP terms. The PHP has lagged the Asia region in the past week. BSP Governor Remolona stated earlier that the central bank didn't overtighten and it would stick with its hawkish bias. On PHP the Governor stated the BSP is 'somewhat comfortable' with current levels (CNBC).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/12/2023 | 0700/0800 | ** |  | SE | Unemployment |

| 15/12/2023 | 0745/0845 | *** |  | FR | HICP (f) |

| 15/12/2023 | 0815/0915 | ** | | FR | S&P Global Services PMI (p) |

| 15/12/2023 | 0815/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 15/12/2023 | 0830/0930 | ** |  | DE | S&P Global Services PMI (p) |

| 15/12/2023 | 0830/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 15/12/2023 | 0900/1000 | ** |  | IT | Italy Final HICP |

| 15/12/2023 | 0900/1000 | ** |  | EU | S&P Global Services PMI (p) |

| 15/12/2023 | 0900/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 15/12/2023 | 0900/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 15/12/2023 | 0930/0930 | *** |  | UK | S&P Global Manufacturing PMI flash |

| 15/12/2023 | 0930/0930 | *** | | UK | S&P Global Services PMI flash |

| 15/12/2023 | 0930/0930 | *** | | UK | S&P Global Composite PMI flash |

| 15/12/2023 | 1000/1100 | * | | EU | Trade Balance |

| 15/12/2023 | 1000/1000 | | UK | BOE's Ramsden Speech at Deloitte on Bank resolution regime | |

| 15/12/2023 | 1315/0815 | ** |  | CA | CMHC Housing Starts |

| 15/12/2023 | 1330/0830 | * | | CA | International Canadian Transaction in Securities |

| 15/12/2023 | 1330/0830 | ** | | CA | Wholesale Trade |

| 15/12/2023 | 1330/0830 | ** |  | US | Empire State Manufacturing Survey |

| 15/12/2023 | 1415/0915 | *** | | US | Industrial Production |

| 15/12/2023 | 1445/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 15/12/2023 | 1445/0945 | *** | | US | S&P Global Services Index (flash) |

| 15/12/2023 | 1630/1630 | | UK | BoE announce APF Sales schedule for Q124 | |

| 15/12/2023 | 1725/1225 | | CA | BOC Governor Macklem speech/press conference | |

| 15/12/2023 | 1800/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

| 15/12/2023 | 2100/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.