Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- US Dollar falls ahead of Jackson Hold later this week, Asian FX rally ahead of key central bank meeting this week

- Asian equities are mixed today, China & Hong Kong Markets outperform driven by strong earnings from tech giants like Alibaba and JD.com

MARKETS

US TSYS: Tsys Futures At Session's Best, Curve Flattens

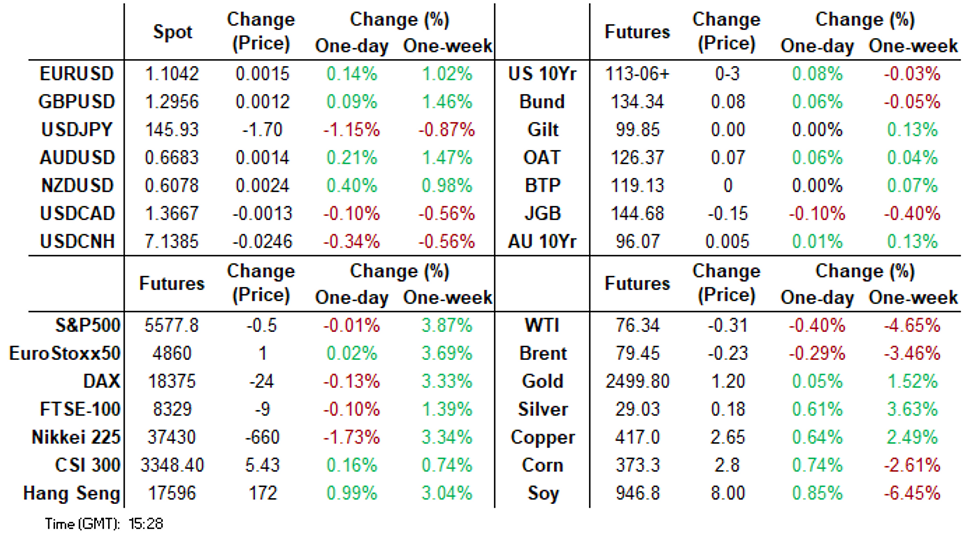

- Treasury futures are off earlier lows and now trade at session's best, although well within Friday's ranges, while volumes are elevated early however have dropped off in the afternoon. TUU4 -00⅝ to 103-04¾, while TYU4 + 00+ to 113-04.

- Cash treasury curve has twist-flattened over the day, with the 2yr yield +0.6bps to 4.056%, while the 10yr yield was -0.2bp at 3.881%, the 2s10s is back near pre-FOMC levels -0.773 at -17.907.

- Projected rate cuts into year end vs. this mornings pre-data levels (*): Sep'24 cumulative -33.8bp (-33.8bp), Nov'24 cumulative -64.2bp (-62.0bp), Dec'24 -96.8bp (-93.5bp).

- Looking ahead, the Fed's Waller to speak, Democratic Convention & Leading Index

ACGBS: Narrow Ranges During A Data-Light Session, RBA Minutes Tomorrow

ACGBs (YM -1.0 & XM -0.5) are slightly weaker, with tight ranges, in a data-light Sydney session.

- It is a relatively light week for local data/news flow, with tomorrow’s release of the RBA’s August 6 meeting minutes the highlight. With the statement and Governor Bullock sounding slightly more hawkish, the minutes will be scrutinised, especially around the rate hike discussion to determine how serious it was. Upside risks to inflation will be another area of focus.

- Cash US tsys are slightly mixed, with a flattening bias, in today’s Asia-Pac session after modest gains on Friday.

- Attention now turns to the KC Fed-hosted Jackson Hole economic symposium "Reassessing the Effectiveness and Transmission of Monetary Policy," which will be held Aug. 22-24. Fed Chairman Powell speaks at 1000ET Friday Morning.

- Cash ACGBs are flat to 1bp cheaper, with the AU-US 10-year yield differential at +5bps.

- Swap rates are flat.

- The bills strip has bear-flattened, with pricing flat to -2.

- RBA-dated OIS pricing is little changed. A cumulative 18bps of easing is priced by year-end.

- The AOFM plans to sell A$800mn of the 3.00% 21 November 2033 bond on Wednesday and A$700mn of the 2.75% 21 November 2028 bond on Friday.

NZGBS: Some Profit-Taking After Strong Post-RBNZ Rally, New May-36 Bond Priced Tomorrow

NZGBs closed on a weak note, with benchmark yields 4bps higher. NZ Treasury’s announcement of the launch of a new May 2036 nominal bond possibly weighed on the market. The issue will be priced tomorrow with NZ treasury expecting to issue at least NZ$3bn.

- Today's price movement also likely reflects profit-taking after the strong post-RBNZ decision rally. Nevertheless, NZGBs remain 5-21bps richer, with the 2/10 curve 16bps steeper.

- NZGBs have also underperformed their $-bloc counterparts, with the NZ-US 6bps wider at +29bps.

- The AU-NZ 10-year yield differential is -4bps today, now standing at -24bps compared to the recent high of -5bps in late July.

- The recent move lower in the 10-year yield differential coincided with a move lower in the AU-NZ 1Y3M spread leading up to the RBA’s August policy meeting. However, this move has reversed, with the AU-NZ 1Y3M spread now approaching cyclical highs. Interestingly, the increase in the 1Y3M spread has not been reflected in the AU-NZ 10-year yield differential.

- Swap rates closed 3-5bps higher.

- RBNZ dated OIS pricing closed 4-7bps firmer across meetings. A cumulative 73bps of easing is priced by year-end.

- The local calendar will see REINZ House Sales and Trade Balance data tomorrow and Q2 Retail Sales Ex Inflation on Friday. Also, RBNZ Deputy Hawkesby will speak tomorrow.

JGBS: Futures Hovering Near Session Cheaps, 20Y Supply Tomorrow

JGB futures are weaker and hovering near session lows, -19 compared to the settlement levels.

- Outside of the previously outlined Machina Orders, there hasn't been much in the way of domestic drivers to flag.

- (MNI, ICYMI) The BoJ will be watching to see whether the US manages to avoid a steep economic slowdown, former BoJ chief economist Toshitaka Sekine told MNI. “The BoJ is unlikely to raise its policy interest rate amid low visibility and volatile markets. I don’t think the low visibility will disperse by the September and October policy-setting meetings,” he said.

- Sekine, who correctly anticipated the BoJ’s July hike in its short-term rate target to 0.25%, said there was a danger it could fall behind the curve if it leaves real interest rates below equilibrium levels for too long, feeding inflation and other economic distortions.

- Cash US tsys are slightly mixed, with a flattening bias, in today’s Asia-Pac session.

- Attention now turns to the Jackson Hole economic symposium, which will be held Aug. 22-24. Fed Chairman Powell speaks at 1000ET Friday morning.

- Cash JGBs are 2-5bps cheaper across benchmarks, with the 20-year underperforming ahead of tomorrow’s supply.

- The swaps curve has bear-steepened, with rates 1-5bps higher. Swap spreads are mixed.

- Tomorrow, the local calendar will see Tokyo Condominiums for Sale data.

ASIA STOCKS: Asian Equities Mixed, Tech Outperforms, Asia FX Surges

Asian markets are trading mixed today, with Japan's stocks falling due to a stronger yen, which pressured technology firms, leading to a decline in the Nikkei 225 and Topix Index. In contrast, Hong Kong's market saw gains, driven by strong earnings from tech giants like Alibaba and JD.com. The broader sentiment in the region is cautious, with investors closely monitoring upcoming comments from Federal Reserve Chair Jerome Powell at the Jackson Hole symposium, which could influence global monetary policy expectations.

- Japanese stocks are slightly lower today, after strong returns since the August 5 sell-off. In June, Japanese machinery orders fell by 6%, but rose 7.4% in the April-June quarter, with private-sector orders slightly up by 2.1% in June but marginally down by 0.1% for the quarter, while a 3.8% decline is forecast for total orders in the July-September quarter. The yen has rallied about 1% which has heavily weigh on tech stocks with the Nikkei falling 0.90% while the TOPIX is 0.65% lower.

- Hong Kong and Chinese markets are trading higher today, led by strong gains in technology stocks following better-than-expected earnings reports. The Hang Seng China Enterprises Index rose as much as 1.8%, with major contributors like Alibaba, JD.com, and Meituan posting significant advances. Investor sentiment is buoyed by speculation around potential fiscal stimulus from Beijing and easing measures, which could support economic growth. The rally is also driven by expectations of a softer U.S. economic landing and possible Fed rate cuts in 2024.

- South Korean equities are a touch lower today, the market has seen gradual recovery since the sharp 8.77% drop on August 5, driven by easing recession fears in the U.S. Technology stocks like Samsung Electronics and SK hynix weighed on the market, while automotive and financial stocks, such as Hyundai Motors and KB Financial have seen gains. The KOSPI is 0.60% lower, while the KOSDAQ is down 0.65%.

- Taiwan equities are higher this morning, following strong inflows into the region to end last week. TSMC is unchanged this morning, while the Taiex is up 0.20%.

- Australian equities are unchanged today with losses in Consumer Staples & Discretionary offset gains in Utilities and Healthcare stocks. New Zealand equities are the worst performing in the region today with the NZX50 down 0.80% after A2 Milk dropped 18% on the back soft guidance.

- Asia EM is mostly higher today with Asian FX rallying, Indonesian's JCI is up 0.10%, India's Nifty 50 is 0.15% higher, Philippines PSEi is 0.90% higher, Malaysia's KLCI is 1.10% higher while Singapore's Strait Times is is unchanged,

ASIA STOCKS: Foreign Investors Return, Tech Stocks See Bulk Of Inflows

- South Korea: South Korea recorded an inflow of $967m Friday, contributing to a net inflow of $1.267b over the past five trading days. The 5-day average inflow is $253m, contrasting with the 20-day average outflow of $59m, and a 100-day average inflow of $78m. Year-to-date, South Korea has seen substantial inflows totaling $18.028b.

- Taiwan: Taiwan saw a significant inflow of $1.642b Friday, with a net inflow of $3.371b over the past five trading days. The 5-day average inflow is $674m, while the 20-day average shows an outflow of $447m, and the 100-day average reflects an outflow of $145m. Year-to-date, Taiwan has experienced outflows totaling $8.099b.

- India: India had an outflow of $283m Thursday, resulting in a net outflow of $863m over the past five trading days. The 5-day average outflow is $173m, compared to a 20-day average outflow of $87m and a 100-day average inflow of $15m. Year-to-date, India has seen inflows totaling $1.510b.

- Indonesia: Indonesian equities registered an inflow of $49m Friday, leading to a net inflow of $187m over the past five trading days. The 5-day average inflow is $37m, with a 20-day average inflow of $22m and a 100-day average outflow of $8m. Year-to-date, Indonesia has accumulated inflows totaling $326m.

- Thailand: Thailand saw an inflow of $10m Friday, with a slight net inflow of $14m over the past five trading days. The 5-day average inflow is $3m, matching the 20-day average inflow of $2m, but there is a 100-day average outflow of $25m. Year-to-date, Thailand has experienced outflows amounting to $3.312b.

- Malaysia: Malaysia recorded an inflow of $65m Friday, contributing to a net inflow of $68m over the past five trading days. The 5-day average inflow is $14m, while the 20-day average shows an outflow of $7m, and the 100-day average reflects an inflow of $2m. Year-to-date, Malaysia has seen inflows totaling $29m.

- Philippines: The Philippines saw an inflow of $11m Friday, leading to a net inflow of $25m over the past five trading days. The 5-day average inflow is $5m, in line with the 20-day average inflow of $1m, but there is a 100-day average outflow of $7m. Year-to-date, the Philippines has experienced outflows totaling $475m.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | 967 | 1267 | 18028 |

| Taiwan (USDmn) | 1642 | 3371 | -8099 |

| India (USDmn)* | -283 | -863 | 1510 |

| Indonesia (USDmn) | 49 | 187 | 326 |

| Thailand (USDmn) | 10 | 14 | -3312 |

| Malaysia (USDmn) | 65 | 68 | 29 |

| Philippines (USDmn) | 11 | 25 | -475 |

| Total | 2461 | 4069 | 8008 |

| * Up to Date 15-Aug-24 |

OIL: Crude Little Changed, Key Events Later In The Week

Oil prices are little changed today and have been trading in a narrow range as the market waits for the outcomes of further meetings in the Middle East. Continued lacklustre data from China have added to existing worries regarding crude demand from the world’s largest importer. The USD index is down 0.3% today but has only managed to lift crude off its intraday low.

- WTI is down 0.2% to $75.40/bbl off today’s low of $75.10, while Brent is 0.1% lower at $79.58/bbl after falling to $79.26 earlier. The tightness implied by the spread between Brent’s two nearest contracts has eased.

- Gaza ceasefire talks continue with conflicting reports on progress towards an agreement. Uncertainty over Iran’s response to the attack on Hamas’ political leader in Tehran also persists. There had been a lot of diplomatic pressure for it to hold until peace talks had concluded.

- Later the Fed’s Waller speaks and US July leading index prints. The focus of the week for oil markets will be Wednesday’s EIA inventory data & FOMC minutes, Thursday’s preliminary August US PMIs & the start of the Jackson Hole symposium followed by Fed Chair Powell’s speech on Friday.

GOLD: Consolidating After Hitting An All-Time High On Friday

Gold is 0.2% lower in today’s Asia-Pac session, after soaring to a fresh all-time high on Friday, notably above the psychological $2,500/oz mark.

- The rise followed US data indicating inflation slowed last month while retail sales surged, easing recession worries while strengthening expectations the Federal Reserve can begin easing in September.

- Lower rates are typically positive for gold, which doesn’t pay interest.

- "Gold's data dependency remains paramount, as jobs, inflation, and economic data all have the potential to clarify the Fed's path and future monetary policy," a strategist at RBC Capital Markets, said in a note. (per BBG)

- Attention now turns to the KC Fed-hosted Jackson Hole economic symposium "Reassessing the Effectiveness and Transmission of Monetary Policy," which will be held Aug. 22-24. Fed Chairman Powell speaks at 1000ET Friday Morning.

- According to MNI’s technicals team, the technical break above $2483.7, the Jul 17 high and the bull trigger resumes the uptrend. The initial target of note is $2528.4, the 3.00 projection of the Oct 6 - 27 - Nov 13 price swing.

LNG: With Robust Asian Demand, Europe Nervous Re Ukraine

European LNG prices were slightly lower on Friday but are still around 10% higher in August to date. They fell 0.4% to EUR 39.43 off the intraday low of EUR 39.12. Prices have been supported by Ukraine’s move into Russia’s Kursk province and the acquisition of gas infrastructure at Sudzha, the last pipeline taking gas from Russia to Europe through Ukraine.

- Ukraine’s incursion into Russia is yet to disrupt gas flows though, but Europe remains alert to possible outages.

- US natural gas fell 3.1% to $2.13 on forecasts for cooler weather in the east and west. Prices are currently around $2.11 and still up 3.3% this month. The market has looked through the first summer inventory drawdown in eight years as output has been cut back and cooling demand has been robust. Production on Friday was up 1.8% y/y while demand rose 4.1% y/y.

- North Asian prices increased 4.8% on Friday to be up over 15% in August as hot weather continues to drive strong cooling demand. India’s LNG imports rose 15% y/y in July. High Asian demand continues to compete with Europe for shipments.

RATES: AU-NZ 10Y Yield Differential Too Low

The AU-NZ 10-year yield differential is -3bps today, now standing at -23bps compared to the recent high of -5bps in late July, which marked the highest level since August 2022.

- The recent move lower in the 10-year yield differential coincided with a move lower in the AU-NZ 3-month swap rate 1-year forward (1Y3M) spread leading up to the RBA’s August policy meeting.

- However, this move has reversed following the RBNZ’s decision to cut the OCR by 25bps on August 14, with the AU-NZ 1Y3M spread now approaching cyclical highs.

- Interestingly, the increase in the 1Y3M spread has not been reflected in the AU-NZ 10-year yield differential.

- A simple regression of the AU-NZ 10-year yield differential against the AU-NZ 1Y3M spread over the past 12 months suggests that the differential is 16bps below its regression fair value (i.e., -23bps versus -7bps).

- The 1Y3M differential is a proxy for the expected relative policy path over the next 12 months.

Figure 1: AU-NZ: 10-Year Yield Differential Vs. 1Y3M Swap Differential

Source: MNI – Market News / Bloomberg

Data: Malaysia - Exports Surge.

- The trade data surged today, ahead of expectations.

- With exports up July 12.3% yoy (prior 1.7%); this was significantly ahead of market expectations for a 9.0% increase.

- Despite the slowdown in China, petroleum products were significantly higher.

- Malaysian electronic exports continue to be strong up significantly on last month.

- By country, Malaysia saw exports to US surge at a time where exports to China have contracted.

- Malaysian Prime Minister Ibraham has sought to position his country as a neutral proposition for the chip industry caught up in the US-China technology war.

CHINA Data Preview: Loan Prime Rates Likely on Hold Tomorrow.

- Commercial banks will likely keep their 1 and 5 year Loan Prime Rates (“LPR”) on hold tomorrow after July’s cut.

- The one-year LPR which is used as the benchmark for commercial loans and the five-year LPR, which is used as the reference rate for mortgages, will likely remain at 3.35% and 3.85% respectively.

- Whilst the PBOC has reiterated its support for the economy, it has cautioned that it won’t be adopting ‘drastic’ measures.

- We read this as allowing time for existing policies to flow through to the economy.

DATA: Thailand - GDP Surprises

- With political uncertainty returning in Thailand, today’s GDP numbers are a welcome respite for financial markets.

- Expectations were for GDP to expand 2.2% for the second quarter, having expanded 1.5% in the first.

- Today’s release surprised to the update at 2.3% yoy with Q1 revised up to 1.6%.

- Thailand’s exports rose 4.8% yoy whilst imports rose 0.5% yoy.

- The numbers reflect a better-than-expected result given the political uncertainty.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 19/08/2024 | - |  | SE | Riksbank Meeting | |

| 19/08/2024 | 2350/0850 | * |  | JP | Machinery orders |

| 19/08/2024 | - |  | UK | DMO to hold quarterly consultation investors / GEMM consultation | |

| 19/08/2024 | 1315/0915 |  | US | Fed Governor Christopher Waller | |

| 19/08/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 19/08/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.