Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

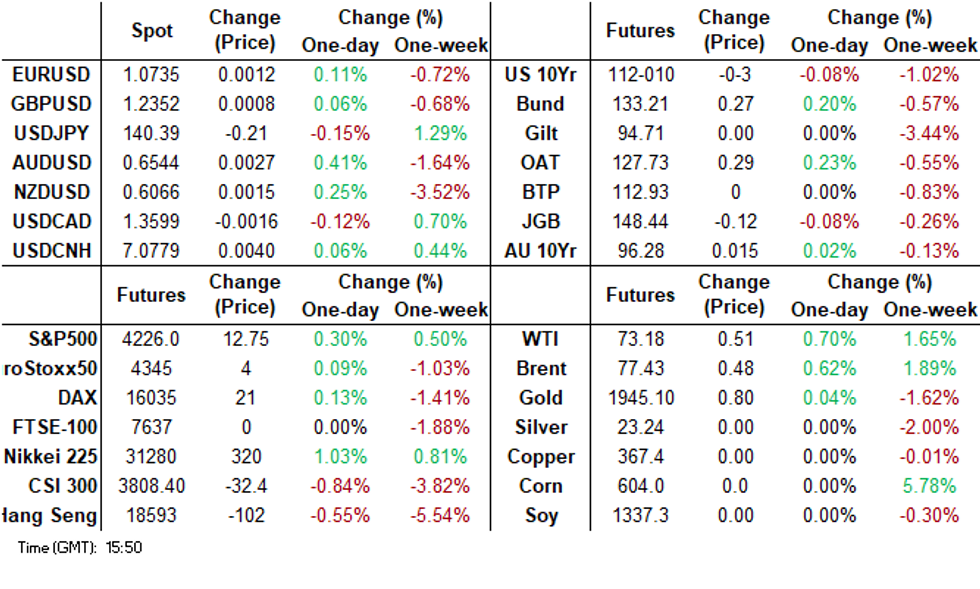

- Early focus was on the US debt ceiling announcement from the weekend. US Equity futures opened higher, while Treasury futures opened weaker. These moves were somewhat reversed as the session progressed. TYM3 is currently trading at 112-10+, -2+ from NY closing levels, after initially cheapening to 112-03+ in early trade.

- The USD was also higher, but gains were not sustained. The BBDXY got to a high of 1246.77, but now sit back around 1245. The early move was largely thanks to USD/JPY climbing to fresh highs, just above 140.90, but from there the pair dipped back sub 140.50, which is where we have spent much of the rest of the session.

- Regional equities are once again mixed. Tech related plays are outperforming, following strong gains for US indices in Friday trade. US Futures but we are away from best levels. The Hang Seng China Enterprise Index is down 0.59%. This puts the index close to bear market territory (-19% off late January highs).

- May bank holiday in the UK, Whit Monday observed in parts of Europe and Memorial Day in the US leaves the data calendars empty, with markets likely to be on headline watch.

MARKETS

US TSYS: Little Changed, Reverses Initial Cheapening On Debt Ceiling Deal News

TYM3 is currently trading at 112-10+, -2+ from NY closing levels, after initially cheapening to 112-03+ in early Asia-Pac trade on news of a debt ceiling deal. However, the ultimate challenge lies in gaining support from lawmakers across the political spectrum.

- Although a deal, if approved by Republican lawmakers, would prevent a default, US tsys will still face the challenge of managing the Treasury's need to replenish its cash balance through T-bill issuance.

- With the Asian calendar light today, local participants are likely to be headlines watch.

- Cash tsys are closed today for the Memorial Day holiday.

JGBS: Futures Weaker, At Cheaps, Rinban Operations Pressure 10-25-Years Zone

JGB futures are at Tokyo session lows in afternoon trade at 148.44, -12 compared to settlement levels as US tsy futures sit slightly weaker in Asia-Pac trade. Cash tsys are closed today for the Memorial Day holiday.

- Cash JGBs cheapen in afternoon trade, primarily driven by the 10-25-year maturity zone. This movement followed BoJ Rinban operations which revealed a higher offer cover ratio and an increased positive spread. However, the cover ratios for the 3-5-year, 5-10-year, and 25-year+ buckets showed a slight decrease.

- Cash JGBs exhibit a mixed trading pattern, displaying yield fluctuations ranging from 0.5bp lower for the 5-year maturity to 1.3bp higher for the 20-year zone. The benchmark 10-year yield has increased by 1.1bp, reaching 0.432%. Meanwhile, the benchmark 2-year yield, ahead of tomorrow's 2-year supply, is trading unchanged lower at -0.063%, showing no sign of concession on the curve.

- The swap curve has twist steepened in afternoon Tokyo trade with rates -0.5bp to +1.8bp and a pivot point at the 4-year zone. Swap spreads are wider beyond the 3-year.

- The local calendar tomorrow sees the Jobless Rate for April released tomorrow ahead of Retail Sales (Apr), IP (Apr P) and Housing Starts (Apr) on Wednesday.

- The MoF plans to sell Y2.9tn of 2-year JGBs tomorrow.

AUSSIE BONDS: Slightly Stronger, Narrow Range, CPI & RBA Lowe’s Testimony On Wednesday

ACGBs are slightly stronger (YM flat & XM +2.0) but off Sydney session's bests as US tsy futures trade slightly lower in a narrow range in Asia-Pac trade. With local headlines and economic data light today, local participants have watched US tsy futures for guidance as the market digests news of a debt ceiling deal.

- Cash tsys are closed today for the Memorial Day holiday. US tsy futures are at 112-10+, -2+ versus Friday’s close, after initially cheapening to 112-03+.

- Cash ACGBs are 1-2bp richer with the AU-US 10-year yield differential -2bp at -9bp.

- Swap rates are 2-3bp lower with the 3s10s curve 1bp flatter and EFPs slightly tighter.

- Bills strip twist flattens with pricing -2 to +2.

- RBA-dated OIS pricing is flat to 2bp firmer for meetings out to October but 1bp softer for meetings beyond.

- The local calendar sees April Building Approvals released tomorrow. Overall, an increase in non-high-rise constructions is expected to contribute to a 2% m/m rise in total dwelling approvals. However, the high-rise sector remains uncertain and poses a significant variable in the equation.

- However, the focus of the week is likely to be RBA Lowe’s appearance and April CPI data on Wednesday.

NZGBS: Closed Richer, At Bests, Headlines Watch

NZGBs finished the session on a high note, experiencing a 2-3bp richening. In the absence of domestic catalysts, local participants have primarily been monitoring US tsy futures and news headlines. In Asia-Pacific trading, US tsy futures are currently trading slightly lower as the market digests the announcement of a bipartisan debt ceiling agreement reached on Saturday. It's important to note that the US market is closed today in observance of the Memorial Day holiday.

- Swap rates are 2-4bp lower with the 2s10s curve 2bp flatter.

- RBNZ dated OIS closed mixed with meetings out to Feb'24 flat to 3bp firmer and meetings beyond 2-3bp softer.

- Westpac’s Monthly Employment Indicator showed a more-than-expected 0.6% m/m rise in-filled jobs to +3.8% y/y, the fastest since January 2022. The series is based on income tax data, which is not only comprehensive but also monthly, whereas Stats NZ labour market data is quarterly.

- On-farm inflation accelerated to 16.3% in the year through March, according to a Beef+Lamb New Zealand report Monday in Wellington.

- The local calendar sees April Building Permits slated for release tomorrow. The number of new dwelling consents rose 7% in March, driven by a large rise in multi-unit consent numbers. A reversal of this strength is expected.

NZ DATA: Westpac’s Monthly Jobs Indicator Points To Strong Labour Market

Westpac’s Monthly Employment Indicator showed a more-than-expected 0.6% m/m rise in-filled jobs to +3.8% y/y, the fastest since January 2022. The series is based on income tax data, which is not only comprehensive but also monthly, whereas Stats NZ labour market data is quarterly with the Q2 release not due until August 2.

- Westpac notes that the robust April outcome has been boosted by the surge in immigration. Recent net inward migration has been running at a 100k annualised rate. But employment growth is still exceeding that of the increase in the overall working-age population and thus not signalling a collapse in the labour market any time soon.

- The RBNZ moved to neutral at its May 24 meeting and while its unemployment rate forecasts were revised down, it observed that pressures were easing in the labour market (see MNI RBNZ Review here.) Westpac said that “the MEI is one indicator that the RBNZ will need to watch closely, as a reminder that the demand for labour is as much a factor as the supply when it comes to inflation pressures.”

EQUITIES: US Futures Higher, China Shares In HK Close To Bear Market Territory

Regional equities are once again mixed. Tech related plays are outperforming, following strong gains for US indices in Friday trade. US Futures are higher following the debt deal announcement from the weekend between Biden and McCarthy, with both leaders expressing confidence that the agreement with pass both US houses. Futures are away from earlier highs though. Eminis last around 4224, +0.25% (opening highs were just above 4243). Nasdaq futures are +0.42%.

- China markets are mixed, with the CSI 300 off by 0.60% to the break. We did see some support around the 3820 region, which is close to recent lows. Some jitters in the local government debt market are likely weighing. The Shanghai Composite is doing better, up 0.15% at this stage.

- Hong Kong markets have returned today, with the HSI off by 0.26% at the break, while the HS China Enterprise Index down 0.59%. This puts the index close to bear market territory (-19% off late January highs).

- The Topix (+0.70%) and Nikkei 225 (+0.99%) are faring better, with tech related strength spilling over. The Taiex is also higher again, +0.85%. South Korean markets are closed today.

- The ASX 200 is up nearly 1%, with firmer commodity prices in the metals space helping.

- The JCI is Indonesia has struggled, down 0.70% at this stage, lower palm oil prices not helping, while slower bank lending is likely raising question marks over the growth outlook.

FOREX: USD/JPY Hits Fresh Highs Before Reversing, A$ Outperforms Modestly

Earlier USD index gains were not sustained, as US Tsy futures have moved away from their lows, as the market continues to digest the debt ceiling agreement. The BBDXY got to a high of 1246.77, but now sit back around 1245.40. The early move was largely thanks to USD/JPY climbing to fresh highs, just above 140.90, but from there the pair dipped back sub 140.50, which is where we have spent much of the rest of the session.

- AUD/USD has outperformed modestly, we got to highs around 0.6545, but now sit back closer to 0.6530, still +0.20% above NY closing levels from last Friday. Some firmness in commodity prices has helped, with iron ore back above the $100/ton level, although copper is down a touch.

- NZD/USD dips sub 0.6050 have been supported, but the pair has been unable to make much headway above this level.

- EUR and GBP are up from earlier lows but have maintained tight ranges. GBP/JPY got close to 174 in early dealings, fresh highs back to 2016, but we sit back at 173.50/55 now.

- With UK and US markets out, the event/data calendar is very light. ECB's De Cos is due to speak.

OIL: Crude Rallies Further But Continues To Face Significant Uncertainty

Oil prices have risen further during APAC trading following Friday’s rally, supported by better risk sentiment following the US debt agreement. The next stage is passing it through Congress which both Biden and McCarthy were confident would occur. WTI is up 0.8% to $73.26/bbl and Brent +0.7% to $77.55. The USD index is flat.

- Brent closed just below $77/bbl on Friday but has spent Monday above that key level with even the intraday low at $77.31. WTI has held above $73 with the low at $73.06.

- Once the US debt-ceiling deal passes Congress, there will be one less concern for the oil market but others remain. It is still worried about further Fed tightening and the resultant recession risk, and the lacklustre recovery in China. On the supply side, Russia doesn’t seem to have reduced its output, but there is the chance that OPEC will reduce quotas again at its upcoming June 3-4 meeting.

- There is a holiday in the US and UK today, so upcoming events are thin. The ECB is observing the Whit Monday holiday. Liquidity in the oil market is expected to be light.

GOLD: Safe Haven Demand Wanes, Debt Ceiling Deal

Gold is little changed at 1945.63 in the Asia-Pacific session, after touching the lowest level since March 22 on Friday, before closing at 1946.46 (+0.2%).

- Demand for safe havens may continue to wane after news of a bipartisan debt ceiling agreement. The agreement entails the suspension of the debt limit for the next two years, while non-defence spending remains unchanged for the upcoming year (with a subsequent 1% increase in the second year). The announcement was made on Saturday.

- The real challenge lies ahead: garnering enough support from lawmakers on both sides of the political spectrum. According to The New York Times, Republican lawmakers have a track record of employing every possible means to hinder spending deals they oppose. They possess the necessary leverage to potentially derail the agreement since McCarthy's majority stands at a mere nine votes.

- Bullion will also face the challenge of coping with the hawkish re-pricing of the Fed funds path observed last week. This challenge may intensify if this week's jobs report continues to show strong numbers.

ASIA FX: Asia FX Underperforms The Majors

USD/Asia pairs are somewhat mixed, with USD/CNH generally supported on dips today. USD/TWD has continued to push lower amid further tech related equity gains. In SEA FX, the USD is mostly firmer. Tomorrow, we have Thai customs trade figures for Apr in a quiet start to the week data wise.

- USD/CNH got to fresh highs near 7.0850, while dips sub 7.0700 have been supported. The pair last tracked 7.0760. The CNY fixing was again neutral, while China equities continue to struggle. In HK, the China Enterprise Index is close to bear market territory, down 19% from late January highs.

- South Korean markets have been closed today, but 1 month USD/KRW upticks have mostly been sold. The pair was last around 1321.

- USD/TWD continues to track lower amid buoyant equity market sentiment related to the tech sector. Spot was last around 30.63, the 1 month NDF near 30.58. Onshore equities are +0.75% for the session. Last Friday saw well over a $1bn flowing into local equities from offshore investors.

- USD/IDR continues to gravitate higher, the pair last in the 14970/75 region, slightly down from session highs. Spot USD/IDR is right on the simple 50-day MA (14974), while beyond round figure resistance at 15000, we also have late March lows near 15050, which may act as upside resistance. BI stated last week at the policy decision it will continue aim towards IDR stability.

- USD/THB got to fresh highs near 34.90, before selling interest emerged. The pair is last back in 34.70/75 region, still 0.15% weaker in baht terms versus closing levels on Friday. Election uncertainty persists, which is weighing on portfolio flows, although onshore equities are tracking higher today, the SET last around 0.55% higher.

- USD/PHP is higher, the pair back above 56.00, last at 56.05, just shy of the simple 200-day MA. Gains in the pair above the 56.00 region haven't been sustained in recent months. On Friday BSP Governor Medalla stated a RRR cut is likely in June, although the central bank would not make it as part of the monetary policy announcement, as it should not be seen as part of the broader monetary policy backdrop.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 30/05/2023 | 2301/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 30/05/2023 | 2350/0850 | * |  | JP | labor forcer survey |

| 30/05/2023 | 0130/1130 | * |  | AU | Building Approvals |

| 30/05/2023 | 0600/0800 | *** |  | SE | GDP |

| 30/05/2023 | 0700/0900 | *** |  | ES | HICP (p) |

| 30/05/2023 | 0700/0900 | *** |  | CH | GDP |

| 30/05/2023 | 0700/0900 | ** | | SE | Economic Tendency Indicator |

| 30/05/2023 | 0700/0900 | * | | CH | KOF Economic Barometer |

| 30/05/2023 | 0800/1000 | ** |  | EU | M3 |

| 30/05/2023 | 0800/1000 | ** |  | IT | PPI |

| 30/05/2023 | 0900/1100 | ** | | EU | EZ Economic Sentiment Indicator |

| 30/05/2023 | 1230/0830 | * |  | CA | Current account |

| 30/05/2023 | 1300/0900 | ** |  | US | S&P Case-Shiller Home Price Index |

| 30/05/2023 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 30/05/2023 | 1300/0900 | ** | | US | FHFA Quarterly Price Index |

| 30/05/2023 | 1400/1000 | *** | | US | Conference Board Consumer Confidence |

| 30/05/2023 | 1430/1030 | ** | | US | Dallas Fed manufacturing survey |

| 30/05/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 30/05/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 30/05/2023 | 1700/1300 | | US | Richmond Fed's Tom Barkin | |

| 30/05/2023 | 1700/1300 | * | | US | US Treasury Auction Result for Cash Management Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.