Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: 2-Way Flow Ahead Of Risk Events

Negative news flow evident over the weekend (centred on the lockdown situation in Europe & the UK) resulted in risk-off flow early on in Asia-Pac dealing, this added to a degree of caution ahead of this week's risk-laden U.S. docket, providing a bid for Tsys, with weak crude oil prices (partly driven by idiosyncracies) also providing support. However, T-Notes are now back from best levels, last +0-00+ at 138-07+, after the Nikkei 225 traded on the front foot, which allowed 5&P 500 e-minis to bottom out and unwind early losses. Cash Tsys sit unchanged to 1.5bp richer across the curve, with 10s leading. A ~2.5K block sale of T-Notes also helped the space back from early highs. Headline flow has generally been light since the re-open, outside of a stronger than expected round of Chinese Caixin manufacturing PMI data, which had no real impact on the space.

- As a reminder, weakness into Friday's close saw T-Notes go out at worst levels of the day, with bear steepening of the curve, as the cash Tsy space cheapened by up to ~6.0bp. The major Wall St. cash indices managed to edge away from lows, but the S&P 500 still finished ~1.2% weaker come the bell. There was little in the way of outright, clear catalysts for the late move, with 30-Year swap spreads moving back from intra-day wides. It may have just been a case of some notable position squaring ahead of this week's impending risk events after month-end support evaporated.

- October's ISM m'fing survey is due to be released today, although focus is set to fall on the impending round of local risk events in the coming days, namely the U.S. election and latest FOMC decision.

U.S. TSYS: MNI Analysis: November Treasury Refunding Estimate Preview

- MNI has published a preview of sell-side analyst expectations for the Treasury quarterly refunding announcement next week Wednesday, November 4 at 0830ET. Expectations are mixed but TIPS are widely expected to increase - for more details please contact sales@marketnews.com.

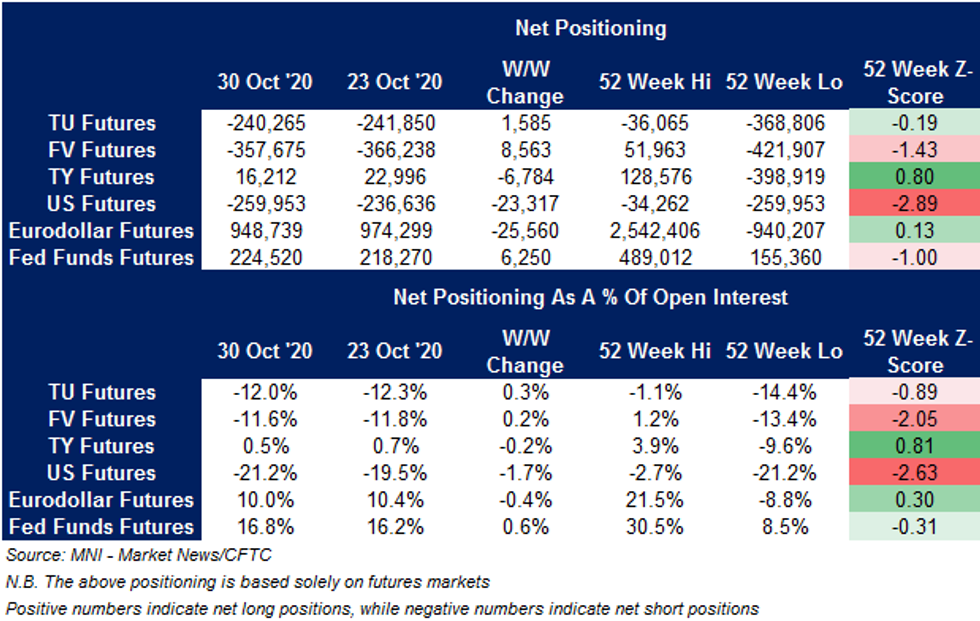

US TSYS: Futures Positioning Twist Steepens Again

Weekly CFTC positioning, covering the week through October 27, pointed to another week of twist steepening in U.S. fixed income futures positions, with another record short position lodged in US (30-Year) futures.

- STIR positioning was a little more mixed, with marginal trimming of net longs in the Eurodollar futures space, while Fed Funds futures positioning gained marginal net length.

RATINGS: Sovereign rating reviews of note from after hours on Friday included:

- Fitch affirmed Finland at AA+, Outlook Stable

- DBRS Morningstar confirmed Italy at BBB (high), Negative Trend

JGBS: Mixed Drivers Ahead Of Local Holiday

JGB futures unwound the bulk of their overnight losses in early Tokyo trade, before holding a narrow range for the remainder of the session.

- Futures sit 6 ticks softer than settlement levels ahead of the close as a result, with the uptick in the Nikkei 225 helping to unwind some of the broader risk-off feel that crept into markets in early trading this week, keeping JGBS in check.

- Cash JGB yields are marginally mixed.

- Comments from Japanese PM Suga offered little new.

- A reminder that Friday saw the BoJ cut the number of monthly Rinban ops covering up to 1-Year, 1-3 & 3-5 Year paper, although it did up the lower and upper ends of the purchase bands covering those Rinban buckets.

- Japanese markets will be closed on Tuesday, owing to a national holiday.

- Locally, 10-Year JGB supply is due Wednesday,

AUSSIE BONDS: XM Off Lows, Heavy Risk Docket Eyed

XM ticked away from early lows, allowing the space to flatten at the margins, and there was little in the way of retracement, with YM closing unchanged and XM settling +0.5.

- As mentioned earlier, the market was willing to look through domestic PMI data, and indeed the firmer than expected Chinese m'fing PMI print, while the remainder of the local data slate was mixed. ANZ job ads and building approvals data firmed, while Melbourne Institute inflation data softened.

- A firm A$1.5bn ACGB 0.25% 21 November 2025 auction was seen, with the bond falling in the proverbial sweet spot of the potential 5-10 Year RBA purchase scheme that could be outlined tomorrow.

- Aussie 10s tightened vs. U.S. 10s ahead of tomorrow's RBA decision.

- Bills finished unchanged to -1 through the reds.

- There is plenty of local and international risk on the docket this week. For the former, the latest RBA decision and SoMP headline (with a broad round of monetary easing expected, our full preview should be published during the London morning), with the U.S. election & subsequent FOMC decision set to dominate elsewhere.

AUCTION/DEBT SUPPLY

AUSSIE BONDS: The AOFM sells A$1.5bn of the 0.25% 21 Nov '25 Bond, issue #TB161:

The Australian Office of Financial Management (AOFM) sells A$1.5bn of the 0.25% 21 November 2025 Bond, issue #TB161:- Average Yield: 0.2745% (prev. 0.3143%)

- High Yield: 0.2750% (prev. 0.3175%)

- Bid/Cover: 6.2733x (prev. 6.1867x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield 81.7% (prev. 19.0%)

- bidders 45 (prev. 49), successful 11 (prev. 13), allocated in full 2 (prev. 6)

TECHS

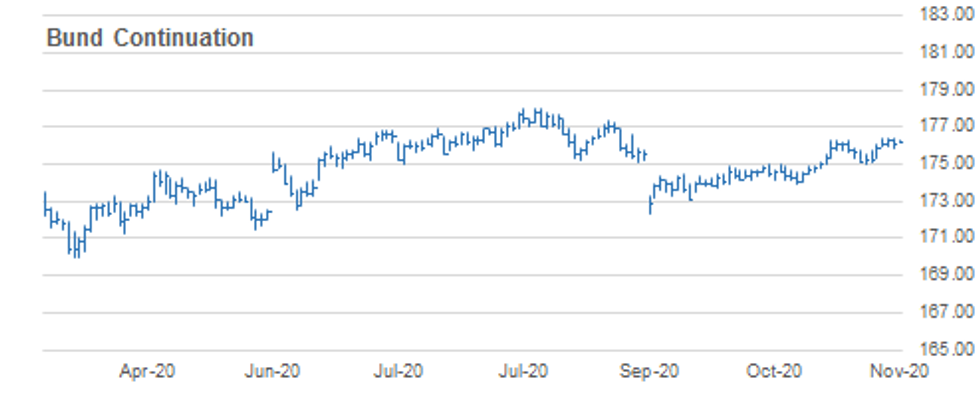

BUND TECHS: (Z0) Holding Onto Recent Gains

- RES 4: 177.00 Round number resistance

- RES 3: 176.89 1.764 proj of Aug 28 - Sep 9 rally from the Sep 10 low

- RES 2: 176.57 1.618 proj of Aug 28 - Sep 9 rally from the Sep 10 low

- RES 1: 176.44 High Oct 29 and the bull trigger

- PRICE: 179.29 @ 04:56 GMT Nov 2

- SUP 1: 175.92 Low Oct 29

- SUP 2: 175.45 20-day EMA

- SUP 3: 175.27 Low Oct 27

- SUP 4: 175.02 Trendline support drawn off the Sep 1 low

Bunds are holding onto recent gains and maintain a positive tone. This follows last week's gains. Futures traded above the key resistance at 176.29, Oct 16 high confirming a resumption of the underlying uptrend that opens 176.57 next, a Fibonacci projection. Moving average studies maintain a positive structure reinforcing bullish conditions. Initial support lies at 175.90, Friday's low. Bullish!

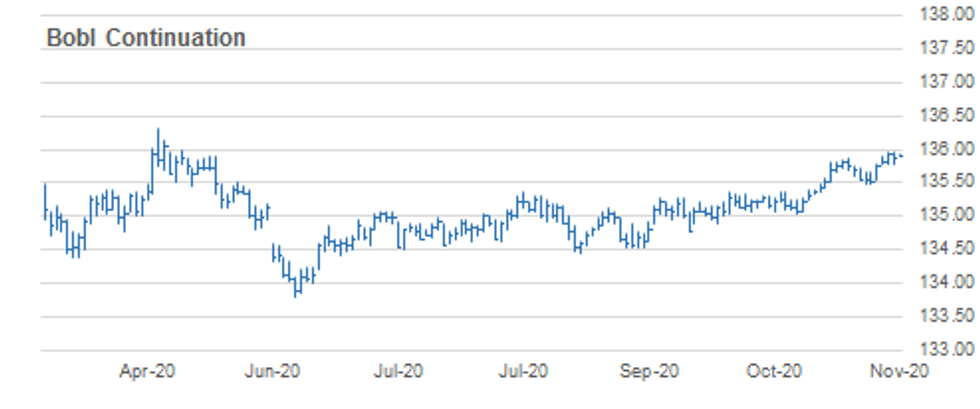

BOBL TECHS: (Z0) Needle Still Points North

- RES 4: 136.14 High May 5 (cont)

- RES 3: 136.060 2.000 proj of Sep 1 - Sep 9 rally from Sep 10 low

- RES 2: 136.000 Round number resistance

- RES 1: 135.960 High Oct 29 and the bull trigger

- PRICE: 135.900 @ 04:52 GMT Nov 2

- SUP 1: 135.770 Low Oct 28

- SUP 2: 135.595 20-day EMA

- SUP 3: 135.530 Low Oct 27

- SUP 4: 135.470 Low Oct 23 and 26

BOBL futures are firm following last week's gains that extended the recovery off 135.470, Oct 23 and 26 low. Price last week traded above key resistance at 135.860, Oct 20 high confirming a resumption of the underlying uptrend. Scope is seen for gains towards 136.00 next ahead of 136.060, a Fibonacci projection. Initial support is at 135.770, Oct 28 low. A move below this support, would expose 135.530, Oct 27 low.

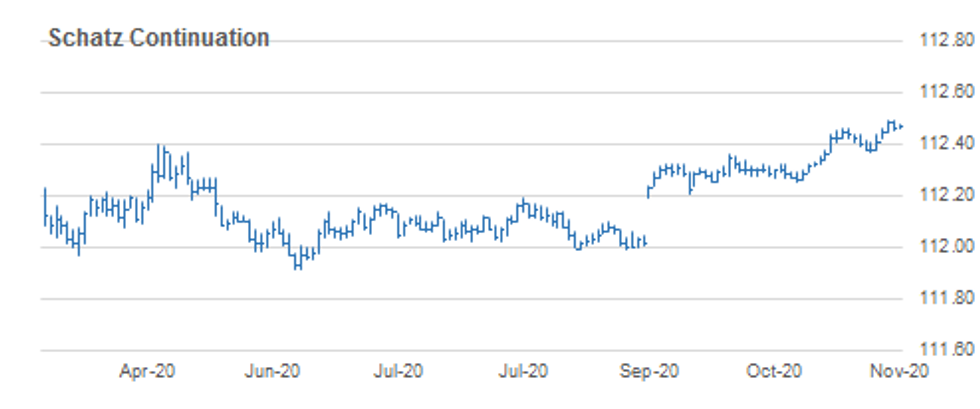

SCHATZ TECHS: (Z0) Bullish Following Key Resistance Break

- RES 4: 112.543 2.382 proj of Aug 26 - Sep 9 rally from the Sep 10 low

- RES 3: 112.523 2.236 proj of Aug 26 - Sep 9 rally from the Sep 10 low

- RES 2: 112.505 61.8% retracement of the Mar - Jun sell-off (cont)

- RES 1: 112.495 High Oct 29

- PRICE: 112.475 @ 05:12 GMT Nov 2

- SUP 1: 112.445 Low Oct 29

- SUP 2: 112.425 Low Oct 27

- SUP 3: 112.394 20-day EMA

- SUP 4: 112.365 Low Oct 26 and key near-term support

Schatz futures traded higher last week, resulting in a convincing break of key resistance at 112.460, Oct 19 /20 and 28 high. The break confirms a resumption of the underlying uptrend and paves the way for strength towards 112.505, a Fibonacci retracement and 112.523, a Fibonacci projection. Key trend support has been defined at 112.365, Oct 26 low where a break is required to reverse the direction. Initial support lies at 112.445.

GILT TECHS: (Z0) Bullish Despite Sharp Retracement

- RES 4: 136.97 High Oct 16 and the bull trigger

- RES 3: 136.38 Low Oct 20 and a gap high on the daily chart

- RES 2: 136.37 High Oct 29

- RES 1: 136.08 High Oct 30

- PRICE: 135.68 @ Close Oct 30

- SUP 1: 135.60 Low Oct 30

- SUP 2: 135.34 Low Oct 27

- SUP 3: 135.04 Low Oct 23 and the near-term bear trigger

- SUP 4: 134.99 1.00 proj of Sep 21 - Oct 7 downleg from Oct 16 high

Strong gains last week were somewhat neutralised Friday following a sharp pullback. Despite the retracement, the near-term outlook remains bullish while futures hold above support at 135.34, Oct 27 low. Attention is on 136.38, Oct 20 low where a print would fill a gap in the chart. This would also expose key resistance at 136.97, Oct 16 high. On the downside, sub 135.34 levels would instead expose the key support at 135.04, Oct 23 low.

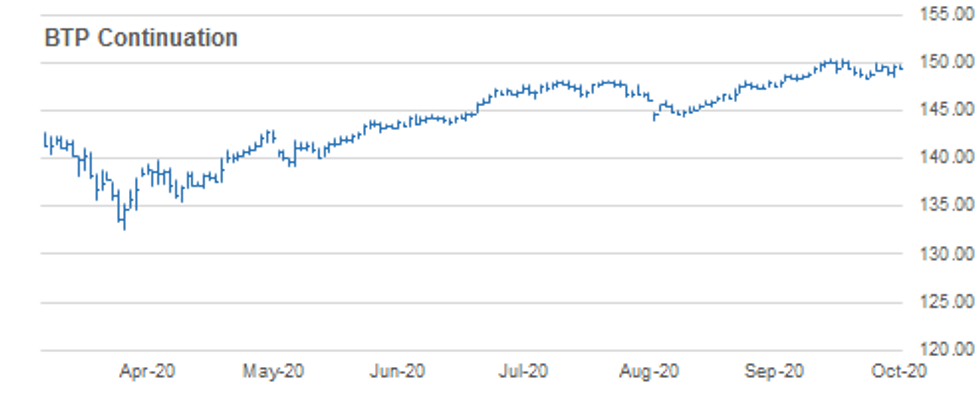

BTPS TECHS: (Z0) Corrective Cycle

- RES 4: 152.00 Round number resistance

- RES 3: 151.17 0.764 of Jun 10 - Aug 20 swing from Sep 9 low (cont)

- RES 2: 150.46 High Oct 16 and the bull trigger

- RES 1: 150.12 Oct 26 high

- PRICE: 149.59 @ Close Oct 30

- SUP 1: 148.68 Low Oct 29

- SUP 2: 148.37 Low Oct 22 and key near-term support

- SUP 3: 148.03 38.2% retracement of the Sep 1 - Oct 16 rally

- SUP 4: 147.68 50-day EMA

BTPS outlook is bullish however futures remain in a corrective cycle and below recent highs. The Oct 26 gap higher failed to deliver a bullish extension and price traded lower on the day to fill the gap. Key S/T support has been defined at 148.37, Oct 22 low. A break of this level would signal scope for a deeper pullback, potentially towards 148.03, a Fibonacci retracement. Key resistance and the bull trigger is at 150.46.

EUROSTOXX50 TECHS: Bearish Conditions Dominate

- RES 4: 3217.96 High Oct 23 and the near term key resistance

- RES 3: 3201.12 50-day EMA

- RES 2: 3135.48 Low Oct 22

- RES 1: 3058.93 Bear channel base drawn off the Jul 21 high

- PRICE: 2958.21 @ Close Oct 30

- SUP 1: 2920.87 Low Oct 29

- SUP 2: 2912.96 Low May 25

- SUP 3: 2877.00 50.0% retracement of the Mar - Jul uptrend

- SUP 4: 2854.07 Low May 22

A bearish EUROSTOXX 50 session dominated last week in line with a general risk-off mood in markets. The index cleared a key support on Oct 28 at 3064.10, the base of a bear channel drawn off the Jul 21 low. This followed a breach on Oct 27 of key support at 3097.67, Sep 25 low. The focus turns to 2877.00 next, 50% retracement of the Mar - Jul rally. Initial resistance is at 3058.93, the former channel base. Heavy!

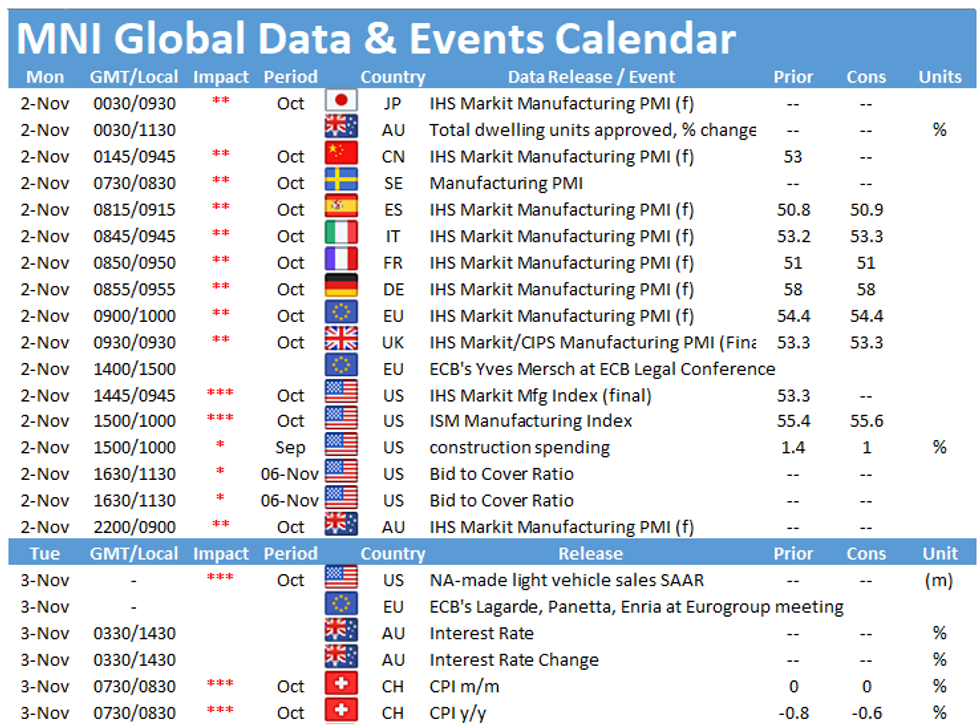

LOOK AHEAD

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.