Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- DXY on the defensive to start the week, with copper and iron ore rallying.

- FOMC adjusted U.S. Tsy supply eyed on Monday.

- Several central banks convene this week (Fed, BoJ, NBH).

BOND SUMMARY: Modest Pressure For Core FI

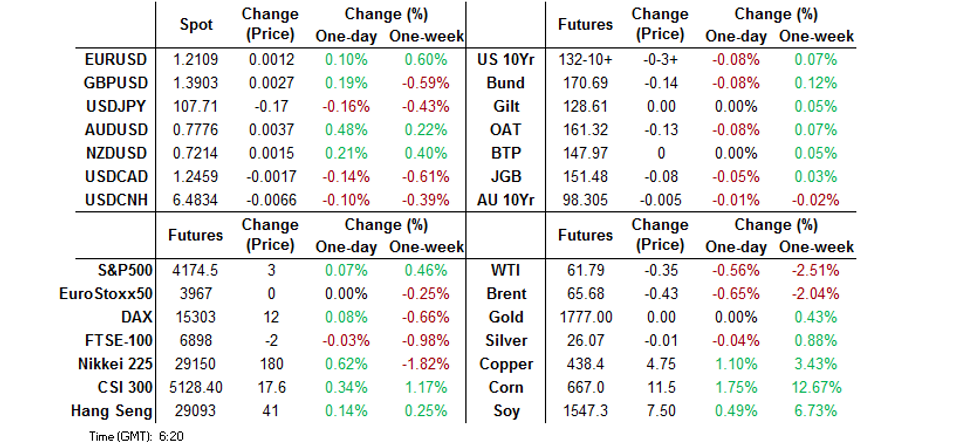

Headline flow was muted during Asia-Pac hours, with the NYT providing comments from EU Commission chief Von Der Leyen pointing to U.S. tourists being able to visit the EU in the summer of '21. Headline flow was also light over the weekend, with most of the focus falling on the world looking to help India through its COVID outbreak and continued insistence on the need for targeted fiscal stimulus (and resistance to the use of the reconciliation measure to pass any linked legislation) on the part of moderate U.S. Democratic Senator Manchin. The U.S. Tsy space has nudged lower, with T-Notes -0-03+ at 132-10+, 0-01 off lows. There is some light steepening in play in cash trade, 5+-Year Tsys have cheapened by ~1.5bp as of typing. Ranges remain tight. E-minis are now in the green, albeit marginally, while the USD has struggled. Focus turns to a condensed pre-FOMC supply schedule from the Treasury. Monday's issuance is headlined by the 2- & 5-Year Tsy auctions. Preliminary U.S. durable goods readings are also due to be released on Monday.

- JGB futures ticked lower during the Tokyo morning, with the move extending during the Tokyo afternoon after an uptick in the offer/cover ratio in the latest round of 5- to 10-Year BoJ Rinban ops. Futures last print -9. The cash curve was subjected to some modest twist steepening. Swap spreads are a touch wider across most of the curve. The weekend saw Japan's ruling LDP Party lose 3 by-elections across Hiroshima, Nagano and Hokkaido, hardly a stamp of approval for PM Suga. The BoJ's latest monetary policy decision will be issued tomorrow (see our full preview for more details on that matter).

- Very little to report for Aussie bonds. The presence of the RBA's scheduled ACGB purchases may have provided a light bid early on, but there has been a modest downtick since (although Aussie outperformance remains evident, likely on the back of the aforementioned RBA purchases). YM -0.5, XM unch., with the contracts sticking to the confines of their respective overnight ranges. The COVID lockdown in Perth (which went into play on Friday night) is set to come to an end at midnight tonight, although 4 days of interim restrictions will be in play in the city & surrounding areas.

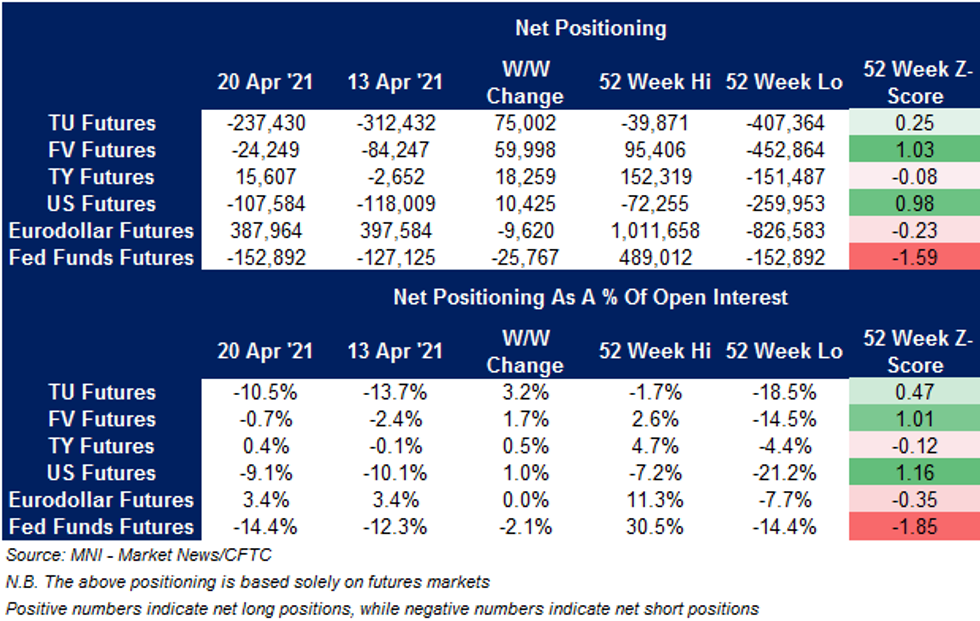

US TSY FUTURES: CFTC CoT Shows Net Shorts Trimmed In Major Tsy Futures Contracts

A quick look at the latest CFTC CoT report revealed a one-way direction of travel for net positioning across the major Tsy futures contracts, which saw net shorts pared back in the TU, FV & US contracts, while TY positioning flipped net long again (as the choppy, unidirectional, nature of that particular contract's net positioning remained evident), in the week ending Tuesday 20 April.

- In STIR futures, net length in Eurodollar futures saw another (modest) reduction. Meanwhile, net shorts in Fed Funds futures extended, hitting the shortest outright levels seen since Aug '19.

FOREX: AUD Gains On Iron Ore Rally, Yuan Draws Support From Upbeat GDP Outlook

Iron ore caught a bid and futures on SGX printed all-time highs, bolstering AUD at the start to the week. The Aussie drew additional support from broadly positive sentiment, reflected in upticks across most regional equity benchmarks.

- NZD gained in tandem with its Antipodean cousin, with liquidity thinned out as New Zealand's markets were shut for the Anzac Day.

- USD headed in the opposite direction, as the DXY faltered to its worst levels since early March. The FOMC are in their blackout period ahead of Wednesday's monetary policy decision.

- The BoJ also hold their policy meeting this week, but USD/JPY was happy to hold Friday's range. BoJ decision announcement is scheduled for tomorrow.

- The PBoC fixed its central USD/CNY mid-point at CNY6.4913, 20 pips above sell-side estimates, but USD/CNH slipped nonetheless. The redback gained as a Chinese gov't think tank said it expects the economy to grow 8% Y/Y this year.

- German Ifo Survey, flash U.S. durable goods orders as well as comments from ECB's Lane & Panetta take focus from here.

FOREX OPTIONS: Expiries for Apr26 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1900(E654mln)

- USD/JPY: Y107.97-108.03($471mln), Y108.15-20($815mln)

- USD/CHF: Chf0.9300($600mln)

- AUD/USD: $0.7945-50(A$732mln)

- AUD/JPY: Y81.50(A$753mln)

- USD/CAD: C$1.2700-10($570mln)

- USD/CNY: Cny6.45($500mln-USD puts)

- USD/MXN: Mxn19.60($650mln)

ASIA FX: Benefits From Higher Risk Appetite

The greenback fell to the lowest levels since early March as risk assets rose, a surge in metals also helped support EM FX.

- CNH: Yuan gained, a report from a government think tank sees GDP growth at 8% this year. Repo rates also rose as the PBOC held off injecting liquidity again even as demand rise ahead of holiday's next week.

- SGD: Singapore dollar strengthened, building on gains after a strong CPI report on Friday. Markets await the industrial production figures later today.

- TWD: Taiwan dollar rose, USD/TWD dipping below the 28.00 handle, it remans to be seen if the rate will close below the level, but NDF's indicate further TWD upside.

- KRW: The won strengthened as coronavirus cases fell back below 600, health authorities warned of tighter restrictions should case numbers pick up gain. GDP data awaits participants tomorrow.

- MYR: Ringgit gained, public support for PM Muhyiddin remains high and stable, according to the latest poll from Merdeka Center. Muhyiddin's approval rating slipped to 67% this month from 68% in March, still up from January's 63%. 70% of respondents were satisfied with the gov't's Covid-19 policies.

- IDR: Rupiah is stronger, the ASEAN summit held over the weekend brought no game-changers. Indonesia pushed for a Myanmar-led dialogue on the ongoing political crisis in that country and joined Vietnam in calling for the resumption of bilateral negotiations on the delineation of the border between their EEZs.

- PHP: Peso is higher, Philippine National Task Force Against Covid-19 said it expects delayed batches of Covid-19 vaccines supplied through the COVAX facility to be delivered next month, with 7-8mn doses due to arrive.

- THB: Baht bucks the trend and is weaker, Thailand's Public Health Emergency Operation Centre held an emergency meeting Sunday to discuss the resurgence of the local Covid-19 outbreak. Public Health Ministry off'l told the media that the gov't is planning to implement a new colour-coded system of targeted restrictions, which will effectively involve tighter curbs.

ASIA RATES: Divergence

Mixed performance as economic divergence becomes more pronounced.

- INDIA: Bonds gained on Friday after auctions saw sales of INR 220bn against a planned INR 320bn, the move provided some supply respite amid a weak appetite for debt, the move is extending so far today. Markets will also assess the worsening coronavirus situation. Chief Minister Arvind Kejriwal on Sunday announced extension of the ongoing lockdown in Delhi for another week, the lockdown imposed on April 19 night will now continue until May 3. While new cases continue to rise, India's vaccination drive is gathering steam, the health ministry claims 14m doses have been administered in 99 days. India is also stepping up support programmes, saying will spend 260 billion rupees ($3.5 billion) to provide free food grain for two months to people covered under the state-run food programme.

- SOUTH KOREA: After initially rising bond futures dropped into negative territory. 10-Year breaking out of Friday's range to print fresh lows, hitting the lowest since April 8. The 5-year auction was well received, cover for the issue rose despite the higher sale size and lower yield. Elsewhere, the MOF said it plans to issue KRW 300bn each of 2-, 3-year bonds in April on a non-competitive basis. This compares to KRW 600bn total in 2-,3- and 30-year bonds in March. The non-comp sales are part of the yield curve monitoring exercise the MOF flagged in March. There were reports on Friday that South Korea's ruling Democratic Party will discuss cash handout for all citizens. It remains to be seen how it will be funded. There have already been a number of special budgets to finance stimulus measures, the extra issuance associated with this has pushed yields higher.

- CHINA: The PBOC matched maturities with injections for the thirty fourth straight session, the last time the bank injected funds into the financial system was Feb 25. The overnight repo rate rose 5 bps to 2.0696% as liquidity demands increase heading into holiday's next week. Bond futures are lower. More woes for China's Huarong who's bonds come under pressure today after the company said its 2020 results would be delayed past an April 30 deadline, after missing a March 31 deadline already. The report did not affect broader markets though, with 5-year corporate bond spreads barrowing to the tightest since March.

- INDONESIA: Yields mixed across the curve, the belly selling off while the wings see buying. The ASEAN summit held over the weekend brought no game-changers. Indonesia pushed for a Myanmar-led dialogue on the ongoing political crisis in that country and joined Vietnam in calling for the resumption of bilateral negotiations on the delineation of the border between their EEZs. Local headline flow has been dominated by the news that Indonesia has found the wreckage of a missing submarine and declared all of the crew members dead.

EQUITIES: Start The Week Higher

Most markets in the Asia-Pac region in the green, though gains are fairly modest for most. Taiwan led gains, up over 1%, the semiconductor sector driving gains after strong industrial production data on Friday. Mainland China is in the green, buoyed by reports that China regulators asks banks to boost lending to SME's. A rally in iron ore and copper has also helped support sentiment. The ASX 200 failed to sustain early gains though, despite the metals rally, as AUD rose. Futures in the US are higher, focus this week will be on the FOMC meeting on Wednesday, while a slew of earnings will also help dictate price action.

GOLD: Consolidating After Another Failure Ahead Of $1,800/oz

The downtick in the DXY evident during Asia-Pac hours supported gold prices in early trade this week, with spot adding a handful of dollars to last print just above $1,780/oz. This comes after Friday's pullback which was facilitated by cheapening in the U.S. Tsy space, resulting in yet another failed run at $1,800/oz. Participants eye this week's U.S. Tsy issuance schedule and Wednesday's FOMC decision.

OIL: Crude Lower As Demand Concerns Weigh

Oil is lower to start the week, with WTI & Brent softening by $0.40 apiece vs. settlement levels.

- Markets look ahead to the OPEC+ meeting on Wednesday this week, there had been discussions that the meeting could be downgraded from a full-scale ministerial meeting, but it appears it will go ahead as scheduled.

- Elsewhere, the preliminary signs of strain in India are starting to show; Mangalore Refinery & Petrochemicals has reduced its processing rates, while Bloomberg reports Indian Oil has so far failed to issue an expected tender to purchase West African crude further stoking demand concerns.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.