Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

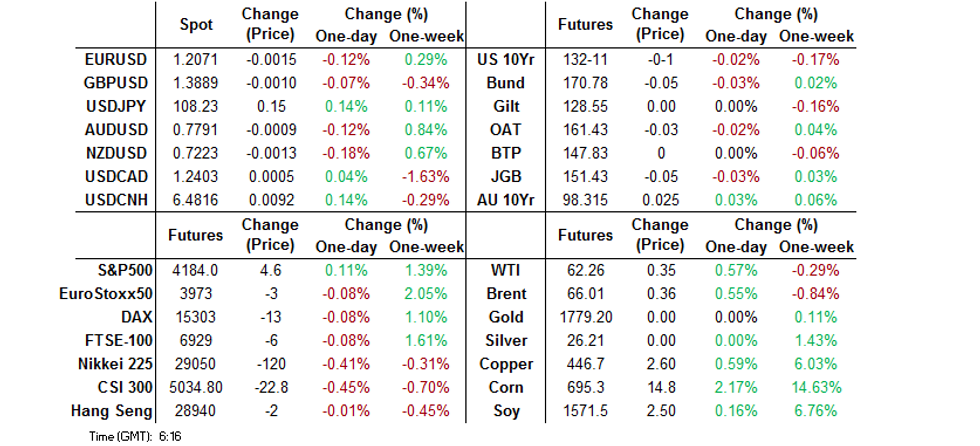

- A limited round of macro headline flow left markets searching for a catalyst overnight, the DXY nudged higher.

- The latest Bank of Japan decision and economic forecasts met broader expectations.

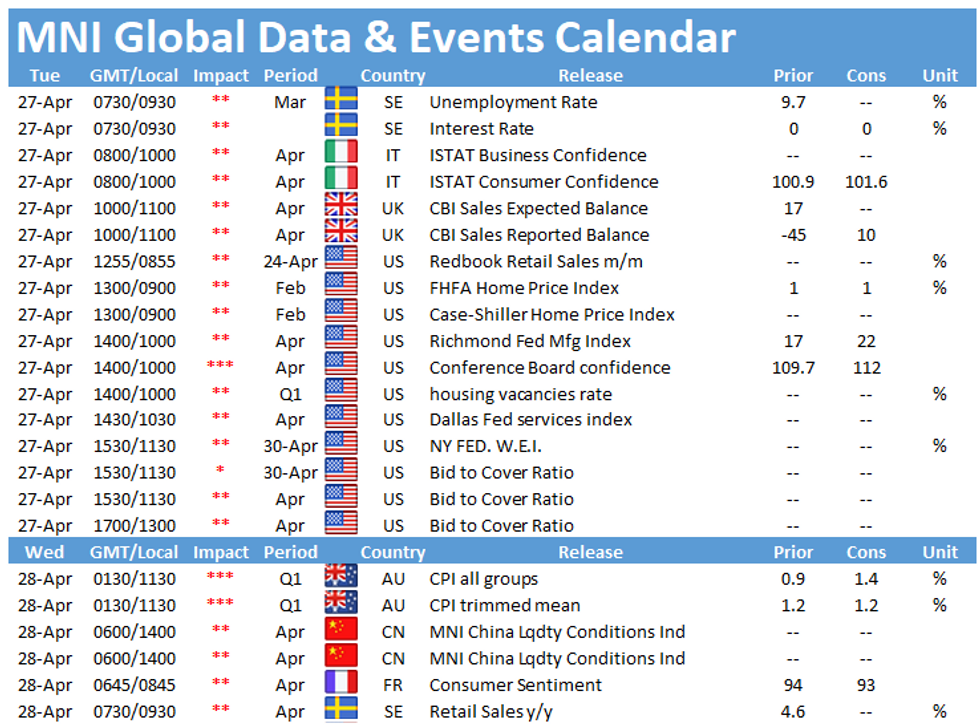

- Monetary policy decisions from the Riksbank & NBH are due today.

BOND SUMMARY: Mixed Fortunes, But Little In The Way Of Strong Direction

T-Notes have been happy to meander along, last -0-01 at 132-11, sitting within the confines of a 0-03+ range, with little in the way of meaningful macro headline flow apparent overnight. The cash Tsy curve has seen some light steepening, with longer dated Tsys cheapening by ~1.0bp vs. Monday's closing levels. Tuesday's 7-Year Tsy & 2-Year FRN auctions present the final issuance hurdles ahead of Wednesday's FOMC decision, while consumer confidence data headlines the local economic docket.

- Yields were marginally mixed across the cash JGB curve, with little in the way of definitive movement observed. Futures ticked lower during the morning but recovered from worst levels to trade 5 ticks lower on the day at typing, holding to a narrow range. The only real point of note on the local front saw Japan confirm that it will set up a mass vaccination centre serving Tokyo & the surrounding areas, although Chief Cabinet Secretary Kato stressed that decisions re: the scale and manufacturer of the vaccine have not been finalised. The latest BoJ monetary policy decision held no surprises, with the Bank's headline monetary policy settings and forward guidance maintained, while the Bank's immediate CPI outlook was shifted lower alongside an uptick in its GDP forecasts. The Bank stressed that the risks for prices are skewed to the downside, while the risks to economic activity are more balanced over the medium term, but hold a downward skew in the immediate term. Kataoka provided the usual dovish source of dissent. The decision and the tweaks to the Bank's economic forecasts were bang in line with wider expectations. Retail sales data headlines the local economic docket on Wednesday, with 2-Year JGB supply also due.

- The ACGB curve has flattened in Sydney trade. YM unch., XM +2.0. Local headline flow has once again been limited at best, although swappable A$ issuance is at the fore. Transurban Queensland Finance launched its previously touted round of 10.25-Year MTN issuance (set to price today), while Network Finance is taking IOIs on long 7-Year fixed/FRN issuance. Swappable A$ issuance can support ACGBs around the time of pricing. Local Q1 CPI data headlines on Wednesday. The reading has the ability to create some short-term volatility for bonds, but shouldn't result in anything like a meaningful shift in RBA pricing. Elsewhere, the latest round of weekly ABS payrolls data is due, as is the preliminary monthly trade balance reading.

FOREX: USD Gains On Defensive Feel In Asia

The greenback recovered from multi-month lows in the quiet Asia-Pac session, as most regional equity benchmarks traded on a heavier note, but other safe haven currencies remained limited. USD/JPY moved higher over the Tokyo fix, but rejected its 50-DMA and ebbed off highs as the BoJ left its monetary policy settings unchanged and tweaked its forecasts in line with expectations.

- The Antipodeans traded on a softer footing amid broadly cautious mood. The kiwi was the worst G10 performer, as local participants returned from a long weekend.

- The PBoC set its USD/CNY mid-point at CNY6.4924, 8 pips above sell-side estimates. USD/CNH crept higher, but yesterday's peak remained intact.

- U.S. Conf. Board Consumer Confidence, Italian sentiment gauges, Swedish unemployment, Riksbank MonPol decision are due today, with speeches coming up from ECB's de Cos & BoC's Macklem.

FOREX OPTIONS: Expiries for Apr27 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1935-50(E1.0bln-EUR puts), $1.2000(E727mln), $1.2070-75(E766mln-EUR puts), $1.2100-05(E847mln-EUR puts), $1.2120-25(E886mln-EUR puts)

- USD/JPY: Y108.50($505mln), Y108.74-75($1.5bln-USD puts), Y109.00-10($1.3bln-USD puts), Y109.45-65($1.3bln-USD puts), Y109.70-85($1.8bln-USD puts)

- USD/CHF: Chf0.9225($525mln-USD puts)

- AUD/USD: $0.7695-0.7700(A$516mln), $0.7710-25(A$1.4bln-AUD puts), $0.7830-35(A$1.2bln-AUD puts)

- USD/CAD: C$1.2500($602mln-USD puts), C$1.3050($676mln)

- USD/CNY: Cny6.52($710mln)

ASIA FX: Some Asia EM FX Strengthens Despite Stronger USD

The greenback rose, pressuring most Asia EM FX, but local dynamics played their part and saw some USD/Asia crosses lower, flying in the face of a stronger DXY.

- CNH: Offshore yuan is weaker, USD/CNH rose as high at 6.4850 before pulling back slightly. Data showed industrial profits rose 92.3% in March after a 20.1% rise previously. Some caution on reports of an antitrust crackdown.

- SGD: Singapore dollar is weaker, retreating from resistance and a two-month high. USD/SGD stays within its recent range.

- TWD: Taiwan dollar strengthened again, USD/TWD consolidating further below the 28.00 handle. It was reported the government plans to start a trial program for fully vaccinated arrivals to apply for shorter quarantine when entering Taiwan.

- KRW: The won is stronger, but off best levels seen at the open. Data released earlier showed preliminary Q1 GDP above estimates. Q/Q printing 1.6% vs estimates of 1.1%, Y/Y growth at 1.8% vs estimates of 1.2%. Exports, consumption and investment all helped lift the figure.

- MYR: Ringgit hovered around neutral levels; FinMin Zafrul added that Malaysia is in the "fifth stage" of its economic recovery and endorsed the central bank's 2021 growth forecast of +6.0-7.5% Y/Y.

- IDR: Rupiah weakened slightly. Health Min Sadikin announced that Indonesia will introduce tighter border measures in anticipation of the return of its migrant workers from abroad. Migrants typically return home for the Eid al-Fitr holidays in May.

- PHP: Peso weakened. Diokno said Monday that RRR cuts remain on the table and reiterated his pledge to keep monetary policy settings accommodative as economic recovery gains pace. He appeared in a briefing of economic managers alongside Finance Sec Dominguez, who said that the gov't looks to trim inessential spending and explore additional sources of revenue. Econ Planning Sec Chua noted that economic managers will wait for Q1 GDP report before revising growth targets.

- THB: Baht is weaker; tomorrow's meeting of the local Covid-19 task force will provide much interest, with officials set to consider stricter curbs. Dep PM & Health Min Anutin suggested that the situation is expected to "return to normal" in two or three months, while Dep PM Supattanapong denied that the resurgence of infections would derail plans to start re-opening tourism in July.

ASIA RATES: RBI Committed To GSAP, Bond Markets Unphased

Indonesian bonds buck the regional trend selling off ahead of an auction later, while COVID-19 concerns remain a concern in India. Declines in equity markets support bonds in China and South Korea.

- INDIA: Bonds under pressure in early trade. The RBI released its monthly bulletin yesterday and defended its bond purchase programme, saying the benefits outweigh the risks. The bulletin added "Policymakers know from painful experience it is perilous to withdraw stimulus too soon" and that the RBI could tolerate an overshoot in inflation to safeguard the recovery.

- SOUTH KOREA: Futures higher in South Korea, gaining through the session. Data released earlier showed preliminary Q1 GDP above estimates. Q/Q printing 1.6% vs estimates of 1.1%, Y/Y growth at 1.8% vs estimates of 1.2%. Exports, consumption and investment all helped lift the figure. The 20-Year auction was well received, bid/cover rose from the previous auction, the MOF sold above the planned amount.

- CHINA: The PBOC matched maturities with injections for the thirty sixth straight session, the last time the bank injected funds into the financial system was Feb 25. The overnight repo rate down 21bps to 1.7891%, the 7-day repo rate up 23bps at 2.28%, above the prevailing 2.20% rate. Futures are slightly higher in China as equity markets decline. Elsewhere Fitch downgraded China's Huarong's credit rating to BBB from A, warning of potential further downgrades if the Chinese government withholds indications of support.

- INDONESIA: Bonds sell off in Indonesia, yields higher across the curve with bear flattening seen. Health Min Sadikin announced that Indonesia will introduce tighter border measures in anticipation of the return of its migrant workers from abroad. Migrants typically return home for the Eid al-Fitr holidays in May. The government will target IDR 30tn at auction today, there is a one month gap until the next auction, which is expected to help participation today.

EQUITIES: Lower Despite Positive Lead From US

A broadly negative day for Asia-Pac indices, most major bourses in negative territory. Markets in mainland China are lower, but moves more muted than yesterday, having declined from the open on reports of an antitrust crack down. Markets in Japan also lower, the BoJ kept rates on hold as expected, the accompanying statement holding no surprises. Markets in South Korea lower, despite a beat in GDP. There are concerns around a surge in coronavirus cases in Asia, with India reporting record figures daily and many other countries considering additional lockdown measures. Futures in the US are higher, the Nasdaq the laggard after posting outsized gains yesterday. Tesla reported after market, but fell despite reporting record profit. Markets await another slew of earnings and the FOMC report on Wednesday.

GOLD: Between The Lines

Bullion is ultimately little changed over the last 24 hours, on net, with spot last dealing little changed at $1,780/oz, as the broad DXY retests yesterday's highs and U.S. yields print flat to marginally higher in the wake of Monday's modest cheapening in the U.S. Tsy space. Gold continues to operate within the confines of a well-defined technical picture, which leaves the recently observed bullish theme intact.

OIL: Crude Futures Squeeze Out Small Gains

Oil squeezed out some gains on Tuesday, following a round trip on Monday that saw crude finish with small losses. WTI & Brent sit ~$0.40 above settlement levels.

- A meeting of OPEC+ technical experts, who provide a formal recommendation to the ministers, began a virtual meeting on Monday. It was reported that the Indian virus issue was at the forefront of deliberations. Resurgent case numbers in Brazil and Japan are also said to have featured heavily in discussions over demand prospects. It was also reported that additional oil refiners in India are postponing maintenance as worker numbers fall, which could result in a reduction in run rates. According to Bloomberg the OPEC+ committee of technical experts forecast that oil consumption will rebound by 6m bpd in 2021 compared to last year, adding that most of the fuel inventories glut built up during the pandemic will have cleared by the end of Q2.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.