Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- UK headline flow was at the fore overnight, with pre-EU-UK summit reports and focus on the potewntial delay of the rollback of the remaining COVID restrictions evident.

- GOP Senator Caputo waters down hopes of imminent deal on infrastructure.

- USD a touch firmer in Asia hours.

BOND SUMMARY: Core FI A Touch Firmer In Asia

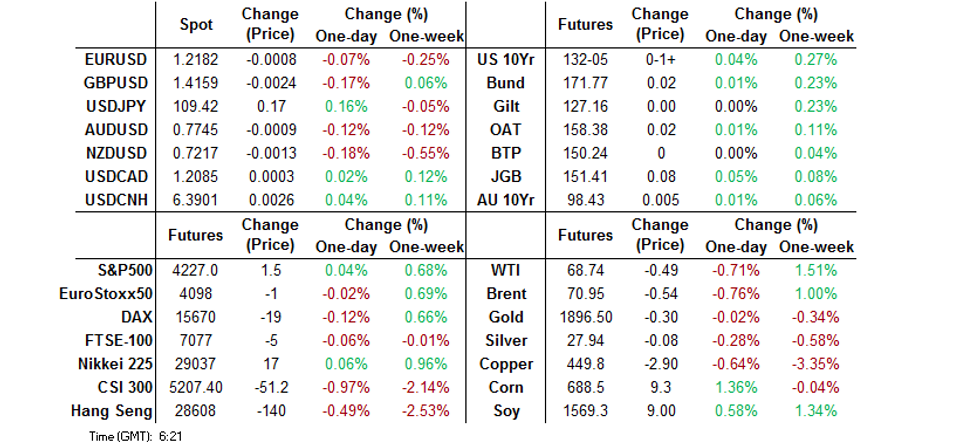

A lack of meaningful headlines and nothing in the way of notable broader market flow has allowed T-Notes to trade within the confines of a 0-02+ range overnight, with the contract last dealing +0-01+ at 132-05. Cash Tsys print unchanged to 1.5bp richer across the curve, with some light bull flattening evident. We should highlight that the NY-Asia crossover saw GOP Senator Capito stress that the GOP is not going to present a further counter-offer to President Biden's fiscal spending proposals ahead of another meeting on Tuesday. Tuesday's focus will fall on 3-Year Tsy supply, and, to a lesser extent, NFIB small business optimism and JOLTS job openings data.

- JGB futures held a narrow range during the Tokyo morning, trading either side of unchanged, before nudging a little higher in the afternoon to last deal +8. A light bid crept into the space despite a less than inspiring round of 30-Year supply all told, as there wasn't any signs of deterioration vs. last month's 30-Year JGB auction. The low price topped broader dealer estimates. The tail width was marginally tighter when compared to the previous round of 30-Year supply. The cover ratio nudged higher when compared to last month's offering but remains somewhat low (a reminder that last month's cover represented a multi-year low for 30-Year JGB supply). The auction result also drove some modest bull flattening. Elsewhere, domestic wage & final Q1 GDP data comfortably topped expectations this morning. Flash machine tool orders data and BoJ Rinban operations covering 1- to 10-Year JGBs headline locally on Wednesday.

- Aussie bond futures have held to very narrow ranges, with YM & XM both +0.5 at typing. Cash ACGBs have twist flattened, with 30s running 3.0bp richer on the day. The latest NAB business survey saw a modest downtick in the confidence component, while conditions moved to a fresh record high. A$1.0bn of ACGB 1.00% 21 Nov '31 supply is due on Wednesday, as is Westpac's monthly consumer confidence reading & ABS payrolls data. Elsewhere, RBA Assistant Governor Kent will appear at the KangaNews Debt Capital Markets Summit. We should also expect roll activity to pick up, with futures moving to smaller tick increments after hours today.

FOREX: GBP Slips In Quiet Asia-Pac Trade

Sterling underperformed its G10 peers in a lacklustre Asia-Pac session as the Times suggested that the UK might have to delay lifting Covid-19 restrictions by a fortnight, following a "downbeat" briefing on the local Covid-19 situation from chief medical officers. Bubbling trade tensions between London and Brussels provided another source of worry. Cable clawed back Monday's losses, with the greenback's buoyance helping the move.

- USD and CHF were broadly higher, but JPY lagged behind its safe haven peers, as Japan's final Q1 GDP numbers were revised higher, beating consensus forecasts.

- NOK traded on a softer footing as crude oil slipped, but CAD was unfazed.

- The PBOC set the central USD/CNY mid-point at CNY6.3909, 6 pips above sell-side estimate. Offshore yuan was happy to hug a narrow range.

- German ZEW Survey & industrial output, final EZ GDP as well as speeches from BoE's Haldane & BoJ's Amamiya headline the global economic docket today.

FOREX OPTIONS: Expiries for Jun08 NY cut 1000ET (Source DTCC)

- EUR/USD: E$1.2055-70(E1.6bln-EUR puts), $1.2175-85(E827mln-EUR puts), $1.2200(E952mln)$1.2225-35(E626mln), $1.2265-75(E631mln-EUR puts), $1.2300(E759mln-EUR puts)

- USD/JPY: Y108.45-50($1.3bln), Y109.00-05($867mln-USD puts), Y109.50($1.1bln-USD puts)

- AUD/USD: $0.7700-10(A$617mln-AUD puts), $0.7745-50(A$893mln)

- NZD/USD: $0.7150(N$601mln-NZD puts), $0.7260(N$1.2bln-NZD puts)

- USD/MXN: Mxn19.87($575mln-USD puts)

ASIA FX: Muted Moves

A quiet, directionless session with narrow ranges observed amid a lack of EM catalysts.

- CNH: Offshore yuan is hugging a tight range, marginally weaker. The PBOC fix came in broadly in-line with sell side estimates. Data late yesterday showed China's foreign reserves rose to $3.2218tn in May from $3.198tn in April, the second month of increase.

- SGD: Singapore dollar is flat, barely budging through the session. USD/SGD consolidated below the 1.3245% 76.4% retracement level, last down 1 pip at 1.3229. The June low of 1.3189 is now in focus for bears before targeting the 2021 low of 1.3157.

- TWD: Taiwan dollar is slightly stronger, markets look ahead to CPI, WPI and trade data later in the session.

- KRW: Won is weaker, reversing earlier gains. Data earlier showed the BoP current account balance narrowed to $1.909bn from $7.816bn, goods balance narrowed to $4.559bn from $7.92bn. Following the release the BoK said higher oil prices increased the price of imports.

- MYR: Ringgit is slightly higher, the Straits Times ran a source report noting that "the heads of Malaysia's nine royal households are set to hold an emergency meeting next Wednesday (June 16), to discuss the country's Covid-19 crisis". The meeting will be preceded by the King's consultations with leaders of Malaysian political parties.

- IDR: Rupiah is flat, Tourism Min Sandiaga Uno said that Bank Indonesia, Financial Services Authority and Investment Min will back the plan to reopen Bali in Jul and encourage tech companies to work from there. The gov't expects Bali's economy to return to growth by Q3/Q4.

- PHP: Peso weakened, headline unemployment rate rose to 8.7% in April from 7.1% recorded in the prior month, while underemployment increased to 17.2% from 16.2%, which occurred alongside a fall in the participation rate to 63.2% from 65.0%. There were just two regions where unemployment reached double-digit levels.

- THB: Baht is lower, Thailand achieved the target of administering more than 300,000 doses of a Covid-19 vaccine on the first day of its mass inoculation drive. AstraZeneca & Sinovac products were used as the country began its vaccination campaign on Monday.

ASIA RATES: Indian Bonds Boosted By Vaccine Announcement & Case Reduction

- INDIA: Yields lower today after PM Modi announced free inoculations for everyone over 18 in a state address yesterday, the plan will start on June 21 and follows criticism of the vaccination roll out. Modi promised to speed up the vaccination programme and also announced the central government would procure the doses for individual states rather than asking provinces to compete for supplies as previously outlined. Assets also given a boost by reports that daily COVID-19 cases are under 100k for the first time in two months. Markets look ahead to state debt sale later in the session.

- SOUTH KOREA: 10-Year future ground higher from the open as equity markets spent the session treading water. Data earlier showed the BoP current account balance narrowed to $1.909bn from $7.816bn, goods balance narrowed to $4.559bn from $7.92bn. Following the release the BoK said higher oil prices increased the price of imports.On the coronavirus front there were 454 new cases in the past 24 hours, in the 400's for the second straight day with authorities citing a pick up in the vaccination campaign

- CHINA: The PBOC matched injections with maturities again, repo rates holding their ground currently but remain elevated. The 7-day repo rate is up 2bps at 2.27%, above the PBOC's 2.20% rate. There was another piece in the China Securities Journal that said the PBOC may inject more liquidity at an appropriate time, very similar in tone to a piece in CSJ last week. Futures gapped higher at the open but are off best levels.

- INDONESIA: Yields slightly higher but seeing little movement ahead of a bond sale later in the session. The government aims to sell IDR 30tn of bonds in 5-, 10-, 15- and 20-year maturities. Data earlier in the session showed foreign reserves slipped slightly to $136.40bn while Danareksa consumer confidence rose 0.1pts to 80.2. A Deutsche Bank report was doing the rounds that noted rupiah bonds could lose support from domestic banks as the economic recovery picks up.

EQUITIES: Lacking Direction

Another mixed session for equities in the Asia-Pac region after a mixed finish for US equities. In Japan major indices are hovering around neutral levels after giving back early gains, Q1 GDP beat expectations earlier today, falling at a slower pace than expected. Markets in China in minor negative territory, while in Taiwan the Taiex is flat ahead of trade and inflation data. In the US futures are higher, the Nasdaq leading the way thanks to a boost from Biogen after its Alzheimer's drug was approved, while gains are moderated by international corporation tax plans.

GOLD: Testing $1,900/oz

Spot gold last deals little changed at $1,895/oz after adding roughly $10/oz on Monday. Our weighted U.S. real yield metric nudged higher on Monday, while the broader DXY softened a touch, providing conflicting inputs for bullion, although the latter has ticked away from Monday's lows. Bulls have ultimately failed to force a fresh, sustained break above $1,900/oz, despite a couple of shallow looks above. The technical picture remains unchanged as a result.

OIL: Crude Futures Retreat From 2018 High

Oil slipped in Asia-Pac trade on Tuesday after posting declines on Monday as markets push pause on the recent rally; WTI is down $0.58 from settlement levels at $68.65 while Brent is down $0.62 at $70.87. There were some positive comments from OPEC SecGen Barkindo yesterday, he said the group expected to see further inventory drawdowns in the months ahead and noted that vaccine rollouts and the "massive fiscal stimulus" aided an upbeat outlook, but that uneven global vaccine availability, high inflation and continued COVID-19 outbreaks were continued risks to oil demand. Markets will watch for any progress in talks with Iran, discussions are said to be at a decisive point, as well as US API stockpile data.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.