Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Investors pulled money from mainland China via the HK-CH Stock Connect schemes, with property tax worries and the local COVID situation the driving force there. Equities would have received some insulation from an uptick in the size of the liquidity deployed via the PBoC's OMOs, with the central bank looking to ease the burden of month-end cash flow demand and government bond issuance.

- USD/TRY tagged a fresh all-time high as President Erdogan made 10 foreign ambassadors to the country (including those from the U.S., Germany & France) persona non-grata.

- German Ifo data, regional Fed m'fing indices from the U.S. and a raft of central bank thetoric from across the globe headline on Monday.

BOND SUMMARY: Off Best Levels, Tight Ranges In Play

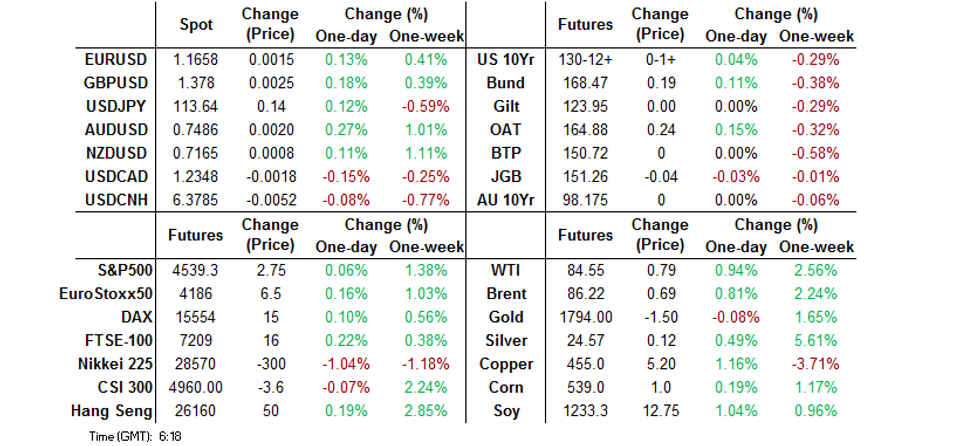

T-Notes last +0-02+ at 130-13+, operating within a 0-05+ range overnight, with cash Tsys running unch.-1.5bp cheaper across the curve, unwinding a small portion of Friday's late rally/bull flattening in the process. The moves witnessed early this morning have likely been geared towards regional Asia players looking to fade Friday's rally/profit taking on any short-term longs, in addition to fresh cycle highs for crude futures, as opposed to reaction to headline flow. The weekend saw Tsy Sec Yellen note that she exp. inflation to remain high through H122, while playing down worry of a loss of control when it comes to inflation. Elsewhere, headlines have pointed to progress in the fiscal back and forth amongst Democrats on the Hill, although no ultimate solution was offered. Regional Fed manufacturing indices will headline during Monday's NY session, with the Fed now in its pre-meeting blackout period.

- Cash JGB trade hasn't seen anything in the way of a convincing bid in the wake of Friday's U.S. Tsy rally, while futures only managed to briefly recover their overnight losses before turning lower again, with the contract last -4. Local headline flow remains light, with most of the focus falling on political matters flagged earlier today. This afternoon's liquidity enhancement auction for off-the-run 15.5- to 39-Year JGBs was fairly bland, with nothing in the way of notable movement in spreads and bid/cover vs. the previous liquidity enhancement auction covering 15.5- to 39-Year off-the-run paper.

- Aussie bond futures have ticked away from best levels after the early catch-up bid (with reference to Friday's late NY richening in U.S. Tsys) provided some support to the space. YM unch. & XM +0.5 at typing. Cash ACGBS have seen some bull flattening, with the longer end firming by ~2.0bp. The latest round of ACGB Nov-24 supply saw solid demand (see earlier bullet for more details), while the RBA stuck to its scheduled round of ACGB purchases, with no need to enforce its YCT mechanism after such purchases were made on Friday and given that favourable prices dynamics (from the point of view of the RBA) have been observed since.

FOREX: JPY Goes Offered, TRY Plunges To Record Low

Safe haven currencies sold off as U.S. e-mini futures reversed their initial losses, with participants assessing familiar themes. Implied USD/JPY volatilities rose across the board, while spot USD/JPY edged higher but stayed within the confines of the prior trading day's range.

- Riskier currencies found some poise, likely aided by firmer crude oil prices, but the kiwi lagged behind. Liquidity in NZD crosses was thinned out by a market holiday in New Zealand.

- The yuan see-sawed within a ~120 pip range as participants assessed China's worsening outbreak of the Delta Covid-19 variant and an upsized liquidity boost from the PBOC. Late-session greenback sales eventually drove USD/CNH lower.

- USD/TRY printed a fresh all-time high before trimming some gains. Geopolitical tensions were the main driver behind lira weakness, as Turkish Pres Erdogan declared 10 foreign ambassadors to Turkey, including those from the U.S., Germany and France, "persona non grata." The rate trades at TRY9.7317 into Europe, up ~1,230 pips on the day.

- German Ifo Survey, regional Fed m'fing indices and comments from ECB's de Cos & Centeno, BoE's Tenreyro, Norges Bank's Bache & Riksbank's Breman will take focus later today.

FOREX OPTIONS: Expiries for Oct25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600-15(E689mln), $1.1720-25(E638mln), $1.1883-00($1.2bln)

- USD/JPY: Y113.00($586mln), Y114.25-50($1.2bln)

- USD/CAD: C$1.2500($620mln)

- USD/CNY: Cny6.4000($631mln)

EQUITIES: Japan Lags, Chinese Stock Connect Net Inflow Streak Set To Halt

Regional equity indices traded either side of unchanged during Asia-Pac hours

- Japanese equities underperformed as PM Kishida continued to experience some early, albeit modest, political headwinds, perhaps bringing into question the ability of the ruling LDP Party to deliver its desired level of stimulus as we move forwards.

- A quick reminder that Friday saw Hong Kong-China northbound Stock Connect flows hit the highest net daily level seen since late June (CNY13.186bn), with net inflows to the mainland in double digit CNY bn territory for 2 consecutive days for the first time since '20. There have been many suggestions that the worst may be behind Chinese equities when it comes to regulatory crackdowns in the wake of recent policymaker rhetoric surrounding the property space, with the Stock Connect flows witnessed at the back end of last week suggesting that participants are starting to buy into that narrative. Note that 4 consecutive days of net buying have been witnessed when it comes to northbound Stock Connect flows. However, the streak looks like it may be broken today, with ~CNY10bn of net sales witnessed during the morning session, perhaps with caution evident surrounding the local COVID situation, with deeper restrictions once again evident in several cities/regions (including Beijing). Property tax fears may have also seen a withdrawal of capital, after state-owned media flagged an impending pilot run of such schemes in various regions over the weekend.

- E-minis are little changed on the day. This comes after a mixed end to last week saw the NASDAQ 100 struggle in the wake of Snapchat & Intel earnings.

GOLD: Off Friday's Highs

Spot gold has stuck to a narrow range during Asia-Pac hours, holding below $1,800/oz for much of the sessio, but still adding a few dollars vs. Friday's closing levels. Friday's break of technical resistance was fleeting, with Fed Chair Powell's lack of reaction to the recent moves in market pricing re: FOMC hikes, even as he sounded a little more concerned with the current inflationary pressures, headlining at the tail end of last week. This was followed up by weekend comments from U.S. Tsy Sec Yellen, who also sounded a little more concerned on the inflation front but played down worry that upward price pressures had spun out of control. Friday's high ($1,813.8/oz) now provides the initial point of resistance, with any breach there set to expose the Jul 15 high/bull trigger ($1,834.1/oz). Support comes in at the Oct 13 low ($1,758.3/oz).

OIL: Fresh Cycle Highs

WTI & Brent crude futures have added ~$0.70 apiece vs. Friday's settlement levels, with both contracts registering fresh cycle highs in the process. This comes after Saudi Arabia cautioned that oil producers should not consider themselves out of the woods yet, with the country once again playing down the need to hike oil production at a quicker than exp. rate on the back of the recent surge in gas prices. We also saw OPEC+ pact participants Nigeria & Azerbaijan play down the need for quicker than outlined rises in crude output re: OPEC+, falling in line with Saudi messaging. The uniform tone coming from those producers, coupled with follow through from Friday's rally & a modest downtick in the USD, has seemingly supported oil early this week.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.