Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

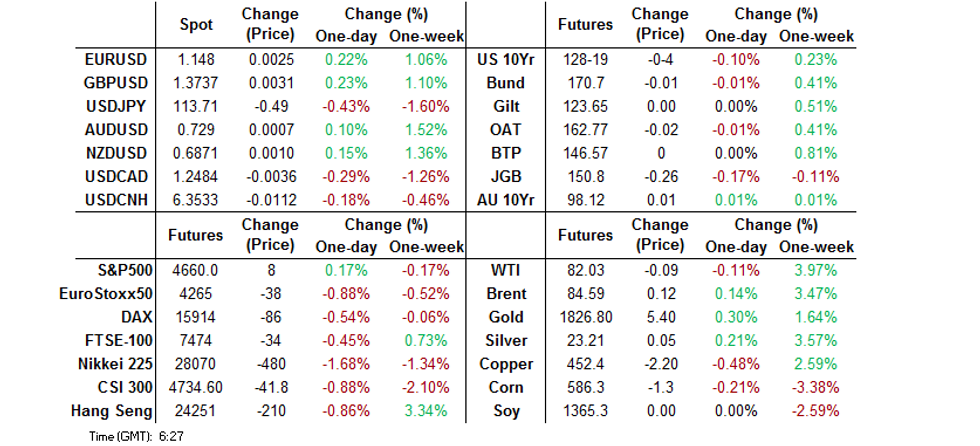

- The recent flow of hawkish Fedspeak continues to undermine market sentiment, as eyes are on policy tightening trajectories across the globe. The BoK hike their policy rate by 25bp to the pre-pandemic level of 1.25% and see inflation above mid-2% over the near term. Separately, Reuters runs report noting that the BoJ might raise interest rates before meeting their inflation target, albeit not imminently.

- Hawkish BoJ talk pressures JGBs, with 5-year yield hitting multi-year highs amid broader weakness in the core FI space. A firm 20-year JGB auction helps bring some stabilisation.

- The yen leads gains in G10 FX space while the Antipodeans falter alongside the greenback. The yuan shrugs off a solid round of trade data out of China and a narrowing bias in the daily fixing of USD/CNY reference rate.

- Asia-Pac equity benchmarks are down, taking their cue from Thursday's tech-led rout on Wall Street. Nonetheless, U.S. e-mini futures swing into positive territory as we head into the London session.

BOND SUMMARY: JGBs Lead Core FI Lower On Talk Of BoJ Considering Rate Hikes Amid Global Tightening

The growing expectation of an earlier/more aggressive policy tightening from the Fed and many of its peers across the globe applied pressure to core FI space, after Thursday saw several voices join the choir of hawkish Fed members. An article suggesting that the BoJ might hike rates before meeting inflation target played into this narrative. So did the BoK's decision to hike their policy rate by 25bp (a non-negligible minority of analysts expected them to stand pat) to the pre-pandemic level of 1.25%, while signalling that they see inflation above mid-2% "for a considerable time."

- T-Notes went offered and extended their pullback from Thursday's high of 128-27 before stabilising in the later part of the Asia-Pac session. TYH2 last changes hands -0-03+ at 128-19+ after bottoming out at 128-17+. Cash U.S. Tsy yields have crept higher, they last sit 1.4-2.1bp higher, as the belly underperforms. Eurodollar futures trade unch. to -3.5 ticks through the reds. Fed's Williams will address the Council on Foreign Relations today, while key data releases include industrial output, retail sales & flash U. of Mich Sentiment.

- Reuters circulated a widely cited source report which added to the general hawkish central bank narrative by noting that BoJ "policymakers are debating how soon they can start telegraphing an eventual interest rate hike, which could come even before inflation hits the bank's 2% target," albeit not imminently. The report knocked JGBs on their head, with futures losing ground in early trade. The contract has edged away from lows after the Tokyo lunch break and now trades at 150.79, 27 ticks shy of last settlement. Cash JGB yields sit higher across the curve, the belly underperforms. The yield on 5-Year Note showed at its highest level since the BoJ adopted their negative interest rate policy in Jan 2016. On the supply front, the lowest bid at today's 20-Year JGB auction topped dealer expectations (which was 90.300 per the BBG dealer poll), which may have provided some incremental relief to the space in the Tokyo afternoon.

- Aussie bonds were driven by offshore impetus, tracking moves in U.S. Tsys & JGBs. Futures have just edged away from session lows but remain below neutral levels (YM -2.5 & XM +0.5). Cash ACGB curve twist flattened a tad, with yields last seen +3.3bp to -1.3bp. Bills run 1-3 ticks lower through the reds. Little to write home about the local headline flow, with ACGBs unfazed by today's offering of ACGB 0.25% 21 Nov '25 and the AOFM's weekly issuance slate.

FOREX: Hawkish Central Bank Musings Spoil Sentiment, BoJ Chatter Supports Yen

The growing prominence of hawkish overtones in recent comments from Fed members continued to undermine appetite for risk assets, with Asia-Pac equity benchmarks taking their cue from Thursday's tech-driven rout on Wall Street. Expectations of global policy tightening were fuelled by a back-to-back rate hike from the BoK, who signalled that their policy rate remains below its neutral (i.e. neither expansionary nor contractionary) level. Elsewhere, Reuters reported that the BoJ are debating how to begin messaging an eventual interest rate hike, which could be delivered before the Bank meets its inflation target (albeit not imminently).

- The yen caught a bid on the back of broader risk aversion and hawkish BoJ musings. This allowed USD/JPY to extend this week's losses past the Y114.00 mark, which provided a layer of support on Thursday. Recall that the BoJ hold a monetary policy meeting next week and may modestly upgrade their FY2022 inflation forecast.

- The Antipodeans landed at the bottom of the G10 pile amid reduced appetite for risk proxies. The USD also traded on a softer footing, but the dollar index (DXY) struggled to break below its 100-DMA. This occurs ahead of a long weekend in the U.S. which may thin out liquidity on Monday.

- Yuan bulls breathed a sigh of relief after the PBOC set their central USD/CNY mid-point just 15 pips above average estimate (as per Bloomberg survey of analysts), a moderation from yesterday's 60-pips bias. A solid round of Chinese data, which showed that monthly trade surplus topped expectations and hit an all-time high, failed to move the redback.

- UK economic activity indicators as well as U.S. industrial output & retail sales take focus from here. The central bank speaker slate features Fed's Williams, ECB's Lagarde & Riksbank's Ingves.

FOREX OPTIONS: Expiries for Jan14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1235-50(E1.2bln), $1.1280-00(E3.9bln), $1.1320(E503mln), $1.1365-75(E1.5bln), $1.1395-05(E1.4bln), $1.1415-25(E2.5bln), $1.1460-70(E1.2bln)

- USD/JPY: Y110.75-00($1.8bln), Y111.80-00($560mln), Y113.35-50($1.6bln), Y113.65-80($1.1bln), Y114.45-55($835mln), Y114.90-10($1.7bln), Y116.00($1.5bln)

- GBP/USD: $1.3385-10(Gbp1.0bln)

- EUR/GBP: Gbp0.8350(E682mln)

- AUD/USD: $0.7125-40(A$1.3bln)

- NZD/USD: $0.6845-50(N$536mln)

- USD/CAD: C$1.2485($1.3bln), C$1.2500-10($2.0bln), C$1.2520-30($1.7bln), C$1.2540-50($929mln)

- USD/CNY: Cny6.35($620mln), Cny6.3750($555mln)

ASIA FX: Price Action Rangebound Despite BoK Hike, Strong Chinese Trade Report

Hawkish Fedspeak did the rounds across Asia, with most USD/Asia crosses holding tight ranges. The rupiah lagged behind its regional peers.

- CNH: Spot USD/CNH has stuck to a narrow range, as the PBOC set their yuan reference rate just 15 pips above sell-side estimate, which represents a moderation from yesterday's 60-pip deviation. The redback also turned a blind eye on China's trade data, which showed that monthly trade surplus hit an all-time high in Dec, while both imports and exports for the entire 2021 printed record highs, generating an annual trade surplus of $676bn.

- KRW: The won showed a very muted reaction to the monetary policy decision from the BoK. South Korea's central bank raised the benchmark interest rate by 25bp to 1.25%, with one dissenter voting to keep it unchanged. The Bank noted that they expect CPI to be above mid-2% this year, while Gov Lee suggested that the policy rate would not be at a contractionary level even if it reaches 1.50%.

- IDR: The rupiah was among the worst performers in the Asia-Pacific, as regional players digested hawkish Fedspeak.

- MYR: Spot USD/MYR snapped its five-day losing streak and crept higher after a failure to penetrate its 200-DMA on Thursday.

- PHP: The peso held a fairly tight range, even as the Philippines reported its highest daily Covid-19 case count on Thursday since the outbreak of the pandemic.

- THB: The baht traded on a marginally firmer footing, cementing its position as the best performer in the Asia EM basket this week.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/01/2022 | 0700/0700 | *** |  | UK | Index of Production |

| 14/01/2022 | 0700/0700 | ** | | UK | Output in the Construction Industry |

| 14/01/2022 | 0700/0700 | ** | | UK | Index of Services |

| 14/01/2022 | 0700/0700 | ** | | UK | UK monthly GDP |

| 14/01/2022 | 0700/0700 | ** | | UK | Trade Balance |

| 14/01/2022 | 0745/0845 | *** |  | FR | HICP (f) |

| 14/01/2022 | 0800/0900 | *** |  | ES | HICP (f) |

| 14/01/2022 | 0830/0930 | *** |  | SE | Inflation report |

| 14/01/2022 | 1000/1100 | * |  | EU | trade balance |

| 14/01/2022 | 1315/1415 | | EU | ECB Lagarde speech at COSAC | |

| 14/01/2022 | 1330/0830 | *** |  | US | Retail Sales |

| 14/01/2022 | 1330/0830 | ** | | US | import/export price index |

| 14/01/2022 | 1415/0915 | *** | | US | Industrial Production |

| 14/01/2022 | 1500/1000 | *** | | US | University of Michigan Sentiment Index (p) |

| 14/01/2022 | 1500/1000 | * | | US | business inventories |

| 14/01/2022 | 1500/1000 | | US | Philadelphia Fed's Patrick Harker | |

| 14/01/2022 | 1600/1100 | | US | New York Fed's John Williams | |

| 14/01/2022 | 1700/1200 |  | CA | BOC releases climate risk paper |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.