Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

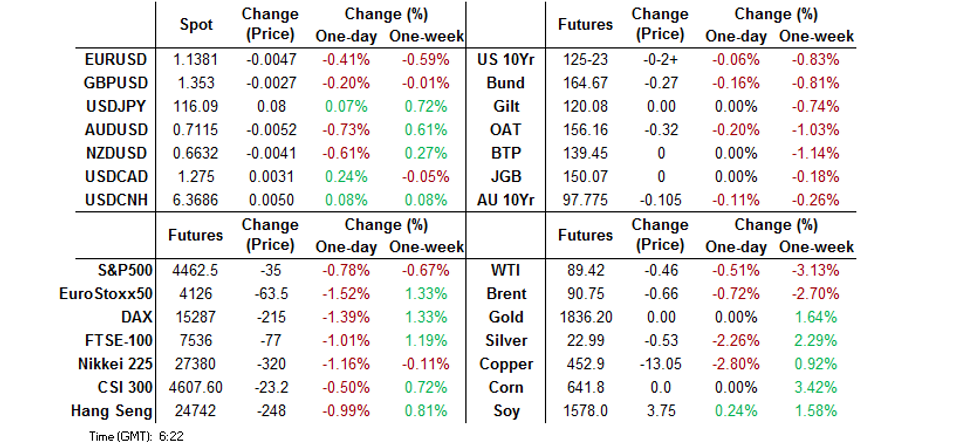

- Fedspeak has been a little bit more measured in the wake of Bullard's ('22 voter) hawkish Thursday utterances, with Daly & Barkin (both '24 voters) unconvinced re: the need for a 50bp hike in March.

- Core FI unwound early Asia upticks, with a hawkish tweak to Goldman Sachs' Fed call and some apparent confusion re: next week's Fed discount rate meeting seemingly at the core of that move.

- Preliminary quarterly growth data & monthly economic activity indicators out of the UK will take focus later today. Elsewhere, ECB's Elderson is due to take part in a panel discussion.

BOND SUMMARY: Early Asia Recovery Unwound

Early Asia-Pac trade saw the core global FI space draw support from continued messaging from ECB President Lagarde re: the need for a gradual removal of accommodation when it comes to altering policy, in addition to some regional demand on the back of Thursday’s U.S. Tsy-driven sell off.

- Later in the Asia session, a fresh round of pressure in the U.S. Tsy & Eurodollar space leaked through into Aussie bonds, with a lack of notable headline flow evident. Most of the initial focus seemed to fall on Goldman Sachs’ altered Fed call (they now look for 7x 25bp rate hikes in ’22 vs. 5x 25bp hikes previously).

- There was also some confusion amongst participants re: the protocol surrounding the regular, scheduled Fed discount rate meeting that is due to be held next week. The fact that the meeting is to be “expedited” was garnering some interest, but after some observation that appears to be the regular protocol (at least in recent times), with core FI markets unwinding some of the pressure after that was cleared up.

- An MNI interview with San Francisco Fed President Daly (’24 voter) saw her play down the need for a 50bp rate hike in March, while Richmond Fed President Barkin (’24 voter) noted that he would need to be “convinced” of the need to do so if he were to support such a move (which he is not conceptually opposed to). This came after St. Louis Fed President Bullard’s hawkish communique on Thursday (calling for 100bp of tightening come the start of July, as well the potential for an inter-meeting hike).

- TYH2 -0-02+ at 125-23, 0-04 off the base of the overnight range (0-05+ off yesterday’s low). Cash Tsys are closed until London hours owing to a Japanese holiday.

- In Australia, YM was -14.0, while XM was -10.5 come the bell, a little off worst levels. The latest round of ACGB supply was smoothly digested. Bills finished 5-25 cheaper through the reds.

AUSSIE BONDS: The AOFM sells A$1.0bn of the 0.25% 21 Nov ‘24 Bond, issue #TB159:

The Australian Office of Financial Management (AOFM) sells A$1.0bn of the 0.25% 21 November 2024 Bond, issue #TB159:

- Average Yield: 1.4898% (prev. 0.8779%)

- High Yield: 1.4925% (prev. 0.8825%)

- Bid/Cover: 4.4130x (prev. 3.3633x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield 46.8% (prev. 52.7%)

- Bidders 44 (prev. 40), successful 18 (prev. 14), allocated in full 10 (prev. 8)

AUSSIE BONDS: AOFM Weekly Issuance Slate

The AOFM has released its weekly issuance slate:

- On Monday 14 February it plans to sell A$500mn of the 2.75% 21 November 2028 Bond.

- On Wednesday 16 February it plans to sell A$1.0bn of the 4.50% 21 April 2033 Bond.

- On Thursday 17 February it plans to sell A$750mn of the 27 May 2022 Note & A$750mn of the 24 June 2022 Note.

- On Friday 18 February it plans to sell A$1.0bn of the 3.25% 21 April 2025 Bond.

FOREX: Hawkish Fed Talk Roils Risk

The dollar index (DXY) advanced towards Thursday's post-CPI highs, as the greenback outperformed in G10 FX space. The Asia-Pacific timezone played catch-up with hawkish Fed repricing, after U.S. CPI smashed expectations, while St. Louis Fed chief Bullard doubled down on his calls for bolder tightening steps, citing the need to contain runaway inflation. The policymaker expressed support for a full percentage point worth of rate increases by July, which could include a supercharged 50bp hike, and raised the prospect of a rate rise outside of the FOMC's scheduled meetings.

- The prospect of a more aggressive policy tightening from the Fed undermined appetite for riskier currencies, with the swap market now fully pricing in seven standard-size rate hikes by the end of the year. Traditional risk proxies such as AUD, NZD and NOK went offered, albeit CAD managed to stay afloat.

- The Aussie dollar underperformed as Gov Lowe told lawmakers that the Reserve Bank is prepared to tolerate inflation "above 3% for a period of time," adding that it is too early "to conclude that inflation is sustainably in the target range."

- The yen garnered some strength on the back of general risk aversion. Spot USD/JPY oscillated in close proximity to key resistance from Jan Feb 10/Jan 4 highs of Y116.34/35.

- Preliminary quarterly growth data & monthly economic activity indicators out of the UK will take focus later today, with ECB's Elderson due to take part in a panel discussion.

FOREX OPTIONS: Expiries for Feb11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1300(E1.4bln), $1.1340-60(E753mln), $1.1400(E701mln), $1.1475(E668mln), $1.1495-05(E3.1bln), $1.1550(E1.0bln)

- USD/JPY: Y115.75($750mln)

- EUR/GBP: Gbp0.8410-25(E608mln), Gbp0.8500-10(E613mln)

- USD/CAD: C$1.2650-60($4.66bln), C$1.2680-85($1.5bln)

ASIA FX: Circling Fed Hawks Undermine Asia EM FX

Fed repricing stoked by above-forecast U.S. CPI data & hawkish comments from St. Louis Fed chief Bullard provided a fillip for USD/Asia crosses, with resultant market impetus outweighing any idiosyncratic goings-on unfolding in Asia.

- CNH: Spot USD/CNH traded with a bullish bias, but held this week's range. The PBOC fix was uneventful, providing no impetus to the yuan.

- KRW: The South Korean won was among the worst performers in the region, owing to its sensitivity to moves in U.S. Tsy yields. FinMin Hong and BoK Gov Lee issued a statement in which they expressed concern over widening inflation pressures and pledged efforts to tackle inflation expectations and core inflation.

- IDR: Demand for the greenback pushed spot USD/IDR higher, even as fresh data showed that Bank Indonesia's consumer confidence index returned to pre-pandemic levels last month. The results of Danareksa Research's survey have not yet been published.

- MYR: Malaysia's economy returned to growth in the final quarter of 2021. The annual rate of GDP expansion printed at +3.6%, topping the median estimate of +3.3% and pushing full-year growth to +3.1% Y/Y. During a subsequent briefing, BNM Gov Shamsiah said that "premature withdrawal" of stimulus could affect economic recovery, adding that Bank Negara can "still afford to hold out a bit more unlike some of its EM peers." The ringgit showed a muted reaction to GDP data/BNM comments and slipped along other Asia EM currencies.

- PHP: Buying pressure returned to spot USD/PHP, with the rate still dangerously close to key resistance from PHP51.500.

- THB: The Thai baht weakened on the back of Fed-related flows, even as Thailand's own central bank flagged potential for an upgrade to the official CPI forecast for this year. The BoT noted that average inflation is expected to exceed the current forecast of +1.7% Y/Y this year and pledged to unveil an updated projection next month. Elsewhere, Thailand's Covid-19 panel gathered to discuss tightening curbs during upcoming holidays.

EQUITIES: Mixed Following U.S. CPI

The Hang Seng and CSI300 outperformed their major Asia-Pac peers, trading 0.1% and 0.3% firmer at writing. Real estate sub-indices helped the outperformance of both. This comes after Thursday media reports pointed to further regulatory easing in the sector i.e. easier access to presale proceeds from residential projects. High-beta Chinese stocks are worse off following Thursday’s U.S. CPI print/Fed-induced Tsy cheapening, with the Hang Seng Tech Index 0.5% lower, while China’s ChiNext trades down 1.4%, operating at the lowest level observed since April ’21.

- E-minis have struggled (the 3 major contracts trade 0.8-1.0% lower at typing), with Tsys receiving little respite during Asia-Pac dealing.

GOLD: Little Changed After Thursday’s Swings

Gold was ultimately little changed overnight, sticking to a narrow range, last dealing around the $1,825/oz mark. This comes after the precious metal was subjected to 2-way trade on the back of Thursday’s U.S. CPI print (marginally firmer than expected) and hawkish Fedspeak from ’22 voter Bullard. Still, spot has stuck to the confines of the upper end of the recently observed range, with the YtD high/bull trigger ($1,853.9/oz) remaining out of reach, for now.

OIL: A Touch Lower In Asia

WTI is -$0.10, while Brent is -$0.20 at writing. A downtick in U.S. e-mini futures has applied some pressure to crude, although both benchmarks operate off of session lows, within the confines of narrow ranges.

- To recap, Thursday’s U.S. CPI print saw both benchmarks whipsaw between gains and losses for the remainder of the session, ultimately closing little changed on the day.

- Hard progress in the indirect Iran-U.S. nuclear talks hasn’t been forthcoming, after hope surrounding the matter provided some pressure earlier in the week.

- From a technical perspective, the uptrend for both oil contracts remain intact. Support is seen at WTI’s Feb 9 low ($88.41) and Brent’s Feb 8 low ($89.93), while resistance holds at recent highs of $93.17 (for WTI) and $94.00 (for Brent). WTI and Brent must close above $92.31 and $93.27, respectively, to avoid their first lower weekly close since mid-December.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 11/02/2022 | 0700/0700 | ** |  | UK | UK monthly GDP |

| 11/02/2022 | 0700/0700 | ** | | UK | Output in the Construction Industry |

| 11/02/2022 | 0700/0700 | ** | | UK | Index of Services |

| 11/02/2022 | 0700/0700 | *** | | UK | Index of Production |

| 11/02/2022 | 0700/0700 | ** | | UK | Trade Balance |

| 11/02/2022 | 0700/0700 | *** | | UK | GDP First Estimate |

| 11/02/2022 | 0700/0800 | *** |  | DE | HICP (f) |

| 11/02/2022 | 0730/0830 | *** |  | CH | CPI |

| 11/02/2022 | 0805/0905 |  | EU | ECB Elderson on sustainable finance discussion at Finance Summit | |

| 11/02/2022 | 1500/1000 | *** |  | US | University of Michigan Sentiment Index (p) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.