Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- War worry surrounding Russia & Ukraine has seemingly pulled back from extremes given the continued push for a diplomatic situation, although risks clearly remain elevated.

- ECB speak continues to point to the need for a gradual adjustment in monetary policy settings when the time comes.

- In the absence of notable data releases today, focus turns to comments from Fed's Bullard & ECB's Lagarde, while the Russia-Ukraine situation continues to provide the obvious source of headline risk.

BOND SUMMARY: Off Of War Worry Extremes

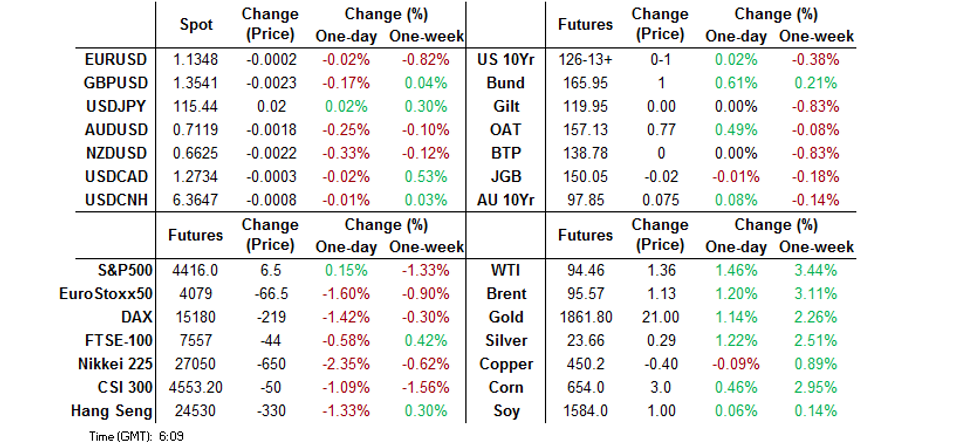

A lack of outright escalation surrounding the Russia-Ukraine situation, in addition to an apparent continued push for a diplomatic solution re: the matter saw core global FI markets back from late Friday/early Asia highs, with e-mini futures lodging gains of ~0.2% overnight after Friday’s sharp risk-off move surrounding the same Russia-Ukraine worry. TYH2 is unch. at 126-12+, with cash Tsys running 1.0-3.0bp cheaper across the curve (2s lead the weakness, while the 5- to 10-Year zone lags). Asia-Pac flow was headlined by a block buy of TU futures (+6,747). Looking ahead, Monday’s NY docket will be headlined by a television address from St. Louis Fed President Bullard (’22 voter, hawk). A reminder that Bullard pointed to the potential for an inter-meeting rate hike in the wake of Thursday’s CPI print, in addition to calling for 100bp of tightening by the start of July. There will of course be continued focus on the Russia-Ukraine situation, which adds the obvious source of headline risk.

- JGB futures pulled back from best levels, closing -1, with a lack of fresh upside catalysts apparent, while the lack of overt escalation surrounding the Russia-Ukraine situation is probably a source of downside pressure. The cheapening in super-long JGBs may give participants fresh ammunition to test the BoJ’s resolve re: the enforcement of its YCC programme after today’s fixed rate operation drew no offers to sell given yield dynamics in play since the 10-Year JGB operation was announced (a reminder that various senior BoJ officials, including Governor Kuroda, have pointed to no change in policy settings until the Bank achieves its inflation goal). Note that 10-Year JGB yields currently sit at 0.22%, while a close above 0.23% seemed to be the trigger for the announcement re: the BoJ’s fixed rate operations.

- There hasn’t been much to report for the ACGB space, with futures largely tracking gyrations witnessed in the wider core FI complex (albeit with a slightly different beta), allowing YM & XM to move away from their respective Friday peaks, before consolidating. YM +7.0 & XM +7.5 at the bell as a result. The 7- to 12-Year zone of the cash ACGB curve outperformed.

AUSSIE BONDS: The AOFM sells A$500mn of the 2.75% 21 Nov ‘28 Bond, issue #TB152:

The Australian Office of Financial Management (AOFM) sells A$500mn of the 2.75% 21 November 2028 Bond, issue #TB152:

- Average Yield: 1.9903% (prev. 1.1425%)

- High Yield: 1.9925% (prev. 1.1475%)

- Bid/Cover: 3.1100x (prev. 5.2980x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield 40.3% (prev. 10.1%)

- Bidders 41 (prev. 53), successful 19 (prev. 22), allocated in full 12 (prev. 11)

FOREX: Cautious Mood Takes Hold As Diplomatic Efforts Fail To Allay Geopolitical Risk

Antipodean currencies led losses in G10 FX space as weekend headline flow failed to alleviate jitters related to the Russo-Ukrainian standoff. Intensified diplomatic activity continued, albeit to no avail so far, with all parties sticking to familiar narratives. While the continuation of broader diplomatic push to defuse the crisis may have proved reassuring at the margin, participants were unwilling to take more risk when faced by the prospect of a potential escalation.

- Weak PSI data for January amplified pressure to the kiwi dollar by showing that New Zealand's services sector has plunged deeper into contraction, with all sub-indices registering losses. Meanwhile, the number of new community cases of Covid-19 reached a record high as the new week got underway.

- The greenback and Swiss franc gained on the back of better appetite for safer currencies, but the yen struggled to jump onto that bandwagon. Its underperformance relative to safe haven peers came as Japan returned from a long weekend to witness BoJ JGB purchase operation intended to cap the recent rise in yields.

- CAD topped the G10 pile as crude oil prices hit fresh cycle highs at the start to the week, underpinned by the unfolding Russo-Ukrainian crisis.

- The Russian rouble extended losses as onshore Moscow markets re-opened, following its most aggressive sell-off since the onset of the Covid-19 pandemic last Friday.

- In the absence of notable data releases today, focus turns to comments from Fed's Bullard & ECB's Lagarde.

FOREX OPTIONS: Expiries for Feb14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E608mln), $1.1480(E1.1bln)

- USD/JPY: Y116.00($532mln)

- AUD/USD: $0.6900(A$1.0bln), $0.7100-10(A$1.6bln)

EQUITIES: Asia Mostly Lower, Friday’s Lows Hold In E-Minis

Benchmark east Asian equity indices trade lower amidst a negative lead from Wall St., after heightened worry re: the Russia-Ukraine situation weighed on risk assets at the backend of last week’s final NY session. The Nikkei 225, TAIEX and KOSPI are 1.7% to 2.2% worse off at typing, after edging away from worst levels observed earlier in the session. The Hang Seng and CSI300 fell less than their major Asia-Pac peers, dealing 1.2% and 0.7% softer respectively.

- Australia’s ASX 200 provided the lone bright spot amongst Asia-Pac equity indices, as gains in energy and heavily weighted financials countered sharper losses in tech stocks, helping the ASX200 to add 0.4% by end of Monday’s trade.

- E-mini equity futures are ~0.2% better off at typing, after Friday’s lows held in early Asia-Pac trade. The lack of outright weekend escalation surrounding the Russia-Ukraine situation probably facilitated such a move (it would have also facilitated the bounce from lows for some of the major Asia-Pac indices).

GOLD: Off Of Friday’s Peak, But Hangs Onto Most Of Russia-Related Gains

U.S. real yields operate off their late Friday base, with gold a touch shy of its late Friday peak as a result, last dealing ~$5/oz lower on the day, just shy of $1,855/oz. Russia-Ukraine tensions remain front and centre, with a lack of clear escalation evident over the weekend. This has allowed markets to breathe a mini sigh of relief after Friday’s late risk-off price action was driven by worry re: the prospect of a fairly imminent invasion of Ukraine by Russia, which supported gold. Still, bullion holds on to the bulk of Friday’s gains. Technically, Friday’s rally took spot through its Jan 25 high/bull trigger, with the next level of meaningful technical resistance located at the Nov 18 high ($1,871.0/oz).

OIL: Still Underpinned

WTI is ~+$1.50, while Brent is ~+$1.40 at typing, with geopolitical unrest surrounding the Russia-Ukraine situation underpinning crude early this week. Both benchmarks hit fresh cycle highs in early Asia-Pac dealing ($94.94 for WTI & $96.16 for Brent), before backing off from best levels.

- Russia-Ukraine tensions remain elevated following Friday’s U.S. warning re: the potential for a Russian invasion “at any time.” Weekend calls between U.S. President Biden, Blinken (U.S. Secretary of State), Austin (U.S. Secretary of Defense), and their respective Russian counterparts produced no breakthroughs, but the continued push to find a diplomatic solution seems to have been welcomed by broader markets (and probably allowed crude to ease back after the early Asia bid).

- Elsewhere in the geopolitical sphere, an Iranian official noted that progress in the well-documented talks surrounding the discontinued nuclear accord was becoming “more difficult,” which may have provided another tailwind for oil early on.

- Crude specific news continues to be supportive. The IEA on Friday warned of “upward pressure” on oil prices due to OPEC+’s “chronic” issues with restoring production, highlighting increased strain on OECD oil inventories, which have declined to 7-year lows.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/02/2022 | 1600/1100 | ** |  | US | NY Fed survey of consumer expectations |

| 14/02/2022 | 1615/1715 |  | EU | ECB Lagarde Speech on anniversary of Euro at EU Parliament | |

| 14/02/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 14/02/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 14/02/2022 | 1630/1730 | | EU | ECB Lagarde Intro at ECB Annual Report 2020 Plenum | |

| 15/02/2022 | 2350/0850 | *** |  | JP | GDP (p) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.