Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

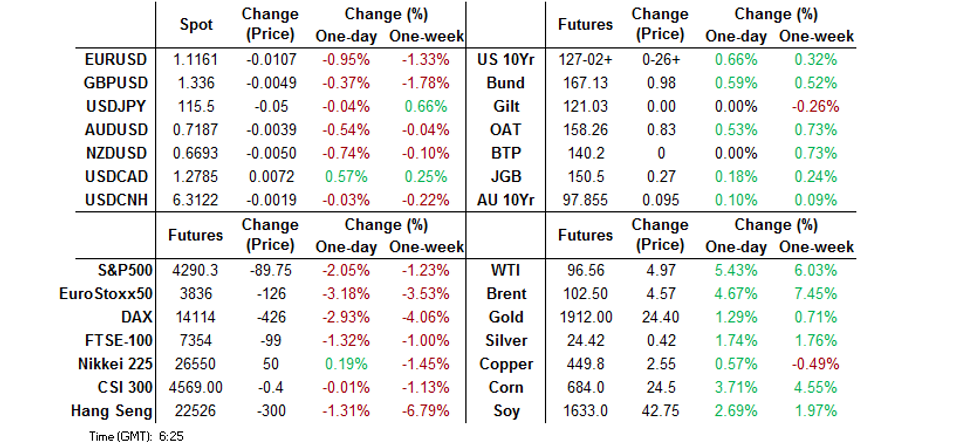

- The combination of Western sanctions on the Russian central bank (a move to try and limit the deployability of Russia’s FX reserves), partial removal of Russian banks from the SWIFT banking communication system and Russian President Putin’s move to raise the alert level of the country’s nuclear deterrent forces to high supported core fixed income markets in Asia. On top of that, the Russian military operation in Ukraine continued over the weekend. Note that Ukrainian President Zelensky has agreed to send a team to conduct talks with Russia near the Ukrainian border with Belarus, but the Ukrainian leadership remain sceptical re: the nature of the talks (the President will remain in Kyiv as a result). Note that the central bank of Russia just implement an emergency 10.5% rate hike.

- USD & JPY led G10 FX trade.

- U.S. MNI Chicago PMI & flash wholesale inventories, Swedish GDP and comments from Fed's Bostic, ECB's Lagarde & Panetta will draw attention later in the day. That is, of course, in addition to headlines surrounding the Russo-Ukrainian war.

BOND SUMMARY: Core FI Firms In Asia

The combination of Western sanctions on the Russian central bank (a move to try and limit the deployability of Russia’s FX reserves), partial removal of Russian banks from the SWIFT banking communication system and Russian President Putin’s move to raise the alert level of the country’s nuclear deterrent forces to high supported core fixed income markets in Asia. On top of that, the Russian military operation in Ukraine continued over the weekend. Note that Ukrainian President Zelensky has agreed to send a team to conduct talks with Russia near the Ukrainian border with Belarus, but the Ukrainian leadership remain sceptical re: the nature of the talks (the President will remain in Kyiv as a result).

- TYM2 continues to operate comfortably shy of best levels, last +0-25+ at 126-31 (operating on ~310K lots, only 15K of that is roll ahead of today’s first notice), while the front end of the cash Tsy curve leads the bid, with the major benchmarks 5.0-8.5bp richer on the session. The odds of a 50bp rate hike in the Fed’s March meeting have evaporated in the OIS space, which is supporting the front end of the Tsy curve. In the STIR space, note that EDH2 is actually lower on the day, -4.00, while the remainder of the whites and reds trade 6.0-12.0bp richer, with all of the contracts back from their early highs. FRA-OIS is wider. Some focus has fallen on the latest note from Credit Suisse’s Pozsar, who flagged the need for central banks to re-open USD swap lines in the wake of the SWIFT limitations placed on Russia, which has likely driven the FRA-OIS widening and EDH2 selling.

- JGBs firmed during Tokyo dealing, in pretty directional trade. That left futures +27 at the bell, a touch shy of best levels, while cash JGBs were 1-4bp richer, bull flattening. Swap spreads widened across the curve. In terms of local data, both industrial production and retail sales provided misses in M/M terms. Our policy team has subsequently flagged its understanding that “downside risks to the economy will be heightened at the March Bank of Japan policy meeting amid the latest tepid economic data and geopolitical risks driving up energy costs that could lead the central bank to issue a rare statement before the end of the fiscal year on maintaining financial market stability.”

- Aussie bond futures squeezed higher into the bell, led by YM as the 3-Year EFP metric jumped. YM was +13.0 with XM +9.5 come the close, with the former tapping fresh session highs late in the day. There wasn’t much to report in local news flow. The latest ACGB Nov-25 tender saw prices print comfortably through mid, although the cover ratio slipped below 3.00x. Bills were unchanged to +13 through the reds. Tomorrow’s RBA decision isn’t expected to be a gamechanger, given the lack of upside surprise in last week’s Q4 WPI print. No changes are expected when it comes to monetary policy settings. Note that the IB strip fully prices a 15bp hike come the end of the Bank’s July meeting.

AUSSIE BONDS: The AOFM sells A$1.0bn of the 0.25% 21 Nov ‘25 Bond, issue #TB161:

The Australian Office of Financial Management (AOFM) sells A$1.0bn of the 0.25% 21 November 2025 Bond, issue #TB161:

- Average Yield: 1.7154% (prev. 1.5056%)

- High Yield: 1.7175% (prev. 1.5075%)

- Bid/Cover: 2.6050x (prev. 4.3400x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield 50.0% (prev. 32.1%)

- Bidders 37 (prev. 42), successful 17 (prev. 11), allocated in full 10 (prev. 5)

FOREX: Western Sanctions Turn Rouble Into Rubble, Safe Havens Catch Bid

The rouble collapsed to historic lows in offshore trading after the West unleashed a barrage of sanctions aiming to isolate Russia from the global financial ecosystem. The decisions to disconnect selected Russian banks from the SWIFT network and restrict Russian central bank's access to its foreign reserves took their toll on RUB, with onshore trading set to reopen with a delay, at 10:00 local time. Anecdotal evidence from trading floors pointed to low turnover, with the rouble perceived as toxic, while press reports showed people queueing up to withdraw foreign currency deposits across various Russian cities. The CRB took measures to soothe the nerves and prevent capital flight, to little avail.

- Financial repercussions of Western sanctions were paralleled by a lingering threat of broader geopolitical escalation. President Putin raised the combat readiness level of Russian nuclear forces, while source reports suggested that Belarus might join the attack on Ukraine. Both steps were a bad omen for today's meeting between Russian and Ukrainian delegations, with Ukrainian President Zelensky sceptical about potential for any breakthrough.

- Contagion risk was a major driver of price action across G10 FX space, with Scandinavian currencies coming under pressure. The Eurozone's single currency went offered as the bloc took a more decisive posture in its response to Russian aggression against Ukraine. Safe haven currencies (USD, JPY, CHF) outperformed as fallout from the Russo-Ukrainian war sent participants looking for shelter.

- U.S. MNI Chicago PMI & flash wholesale inventories, Swedish GDP and comments from Fed's Bostic, ECB's Lagarde & Panetta will draw attention later in the day. That is, of course, in addition to headlines surrounding the Russo-Ukrainian war.

ASIA FX: Russo-Ukrainian War Generates Defensive Impulse

The greenback appreciated against most Asia EM currencies after the West aggressively stepped up sanctions against Russia over its ongoing invasion of Ukraine, which reverberated across global financial markets.

- CNH: Spot USD/CNH gradually unwound its opening uptick, ignoring a weaker than expected PBOC fix. China's central bank set the USD/CNY reference rate at CNY6.2222, 22 pips above sell-side estimate. The yuan was unfazed by the risk of sales by the Russian central bank after Western sanctions restricted the CBR's access to its foreign reserves.

- KRW: Spot USD/KRW traded with a bullish bias, printing a fresh cycle high in the process. The won was pressured by fallout from the Russo-Ukrainian war and a North Korean rocket launch, described by Pyongyang as a test for a reconnaissance satellite.

- MYR: The ringgit garnered some strength in early trade, before giving away those gains, trapped between the opposing forces of risk aversion and firmer oil prices.

- PHP: Spot USD/PHP edged higher, even as the government confirmed easing Covid Alert Level in Metro Manila, but key resistance from PHP51.500 remained intact.

- THB: Defensive flows sapped strength from the baht, making it the worst performer in the region. A miss in Thailand's factory output growth rubbed salt into its wounds.

- Markets in Taiwan and Indonesia were closed in observance of respective public holidays.

EQUITIES: Asia Mostly Lower As Russia-Ukraine Tensions Rattles Up, Commodity Names Gain

The positive lead from Wall St. was negated by flows arising from the well-documented escalation in geopolitical tensions surrounding the Russia-Ukraine situation over the weekend. Commodity-linked stocks across Asia saw notable gains on Monday amidst a rise in commodity prices, with the Bloomberg Commodity Index (BCOM) sitting 2.8% better off at typing.

- The Hang Seng leads losses amongst regional peers, printing 1.4% worse off at typing, taking the index to levels not witnessed since Mar ’20. China-based technology companies again underperformed, with steep declines seen in the real estate and financials sub-indices as well.

- The CSI300 sits 0.4% weaker, with gains in sectors seen to potentially benefit from a conflict in Ukraine and international sanctions on Russia (i.e. materials, energy and payments) countered by declines in risk-sensitive consumer discretionary and consumer staples stocks.

- Looking ahead, China’s political elite will meet for the annual “Two Sessions” in Beijing on Mar 4. Participants will likely be on the lookout for the announcement of “pro-growth” policies, mainly to address the government’s previously identified issues of “contraction of demand, supply shocks, and weaker expectations” within the Chinese economy.

- The Australian ASX200 bucked the broader trend of losses in the region to add 0.7%, led by gains in materials and energy stocks.

- U.S. e-mini equity index futures deal 1.7% to 2.6% softer at typing.

GOLD: Higher On Geopolitical Risk

Gold deals ~$20/oz firmer to print $1,909.3/oz at writing, backing away from the session’s best levels ($1,930.9/oz) after gapping higher on developments in the Russia-Ukraine situation over the weekend.

- To recap, the U.S., UK, EU, Japan, and Canada have expanded sanctions against Russia, including the exclusion of some Russian banks from SWIFT, in addition to imposing sanctions on the Russian central bank. Russian President Putin has since responded by placing the country’s nuclear forces on “high alert.” The pickup in geopolitical tension has facilitated risk-off flows on Monday’s Asian session.

- Ukrainian officials will meet Russian negotiators on the Belarus-Ukraine border for talks, although an immediate resolution is not expected. Ukrainian President Zelensky has expressed scepticism re: the talks, while Russian news agency TASS has reported that Russian officials will only speak about the possibility of fulfilling Moscow’s demands for “demilitarization and denazification”.

- From a technical perspective, the outlook remains bullish for gold despite recent price volatility. Resistance is located at ~$1,939.2 (top of the bull channel drawn from the Aug 9 ’21 low), while support is some distance away at $1,878.4 (Feb 24 low and key short-term support).

OIL: Underpinned In Asia

WTI and Brent have pulled back sharply from session highs after gapping up from Friday’s close, but the benchmarks still sit $5.30 and $4.80 better off at typing, respectively. Weekend developments surrounding the Russia-Ukraine situation have pushed crude higher during Asia-Pac hours, with participants focusing on the lifting of Russia’s nuclear deterrent forces to high alert on Sunday, as well as intensifying international sanctions on Russian banks (which includes a partial withdrawal of Russian access to the SWIFT system). Note that the wires have reported that several banks have pulled/restricting their financing of Russian commodities trading as a result of the partial suspension from SWIFT.

- Ongoing Iranian nuclear negotiations continue to see little by way of concrete developments, with Iran’s chief nuclear negotiator due to return to talks this week. While Iranian FM Amirabdollahian on Saturday stated that talks could “immediately conclude” should western powers show “real will”, U.S. officials have highlighted that “very serious issues” remain on the table.

- Looking to technical levels, resistance for WTI and Brent is situated at their Feb 24 highs of $100.54 and $105.79 respectively, while support is seen at $94.95 (Feb 22 high) for WTI, and $97.56 (Feb 24 low) for Brent.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/02/2022 | 0030/1130 |  | AU | Business Indicators | |

| 28/02/2022 | 0030/1130 | ** | | AU | Retail Trade |

| 28/02/2022 | 0700/0800 | *** |  | SE | GDP |

| 28/02/2022 | 0700/0800 | ** | | SE | Retail Sales |

| 28/02/2022 | 0700/0800 | ** | | SE | Trade Data |

| 28/02/2022 | 0730/0830 | ** |  | CH | retail sales |

| 28/02/2022 | 0800/0900 | *** |  | ES | HICP (p) |

| 28/02/2022 | 0800/0900 | *** | | CH | GDP |

| 28/02/2022 | 0800/0900 | * | | CH | KOF Economic Barometer |

| 28/02/2022 | 1130/1230 |  | EU | ECB Panetta speech at EUI monetary policy debate | |

| 28/02/2022 | 1330/0830 | ** |  | US | advance trade, advance business inventories |

| 28/02/2022 | 1330/0830 | * |  | CA | Current account |

| 28/02/2022 | 1445/0945 | ** | | US | MNI Chicago PMI |

| 28/02/2022 | 1530/1030 | ** | | US | Dallas Fed manufacturing survey |

| 28/02/2022 | 1530/1030 | | US | Atlanta Fed's Raphael Bostic | |

| 28/02/2022 | 1550/1650 | | EU | ECB Lagarde speech on Women in Econ & Finance | |

| 28/02/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 28/02/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 01/03/2022 | 2200/0900 | ** | | AU | IHS Markit Manufacturing PMI (f) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.