Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

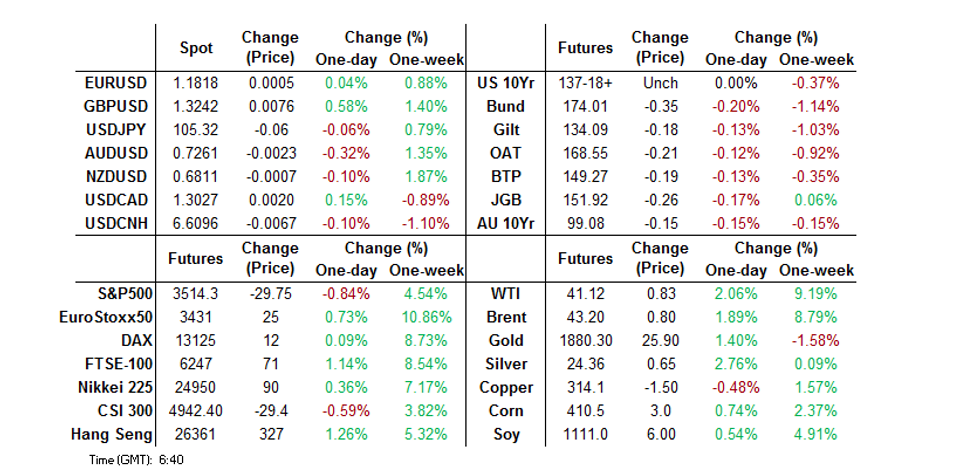

- Japanese markets were at the fore as Japanese government officials reiterated language re: FX market fluctuations, while the BoJ conducted 2 rounds of fixed rate operations to defend the upper boundary of its permitted 10-Year JGB yield trading band.

- JPY crosses were better offered in Asia, while the JGB curve steepened, aided by a poor round of 40-Year JGB supply.

- The economic docket is rather light on Tuesday, with focus set to fall on the ongoing Russia-Ukraine summit in Turkey, in addition to addresses from Fed’s Williams & Harker, ECB’s de Cos & Riksbank’s Floden. The ongoing Russia-Ukraine summit in Turkey will also garner interest.

BOND SUMMARY: BoJ Active, Tsys Soften

U. S. Tsys cheapened a touch in overnight trade, although it wasn’t one-way traffic, with spill over from the recovery off Monday’s session lows eventually negated by payside interest in swaps & some spill over from the JGB space (post-supply). That leaves the major cash Tsy benchmarks 2-5bp cheaper into London dealing, as the curve bear flattens. TYM2 is -0-05 at 121-17+, just off worst levels of the session. A block roll of FV 114.25 puts down into the 113.25 strike (10K in size) and a 5K block sale of the 114.25 puts in isolation (profit taking) headlined on the flow side in Asia. Tuesday’s NY docket includes consumer confidence & JOLTS job openings data, Fedspeak from NY Fed President Williams & Philly Fed President Harker (’23 voter) & 7-Year Tsy supply. The ongoing Russia-Ukraine summit in Turkey will also garner interest.

- JGBs pulled back from their overnight session lows, initially aided by the presence of the BoJ’s fixed rate operations to enforce the upper end of its permitted 10-Year JGB yield trading band (Scheduled through the end of March). Still, the curve ran steeper as concession was built in ahead of today’s 40-Year auction. The auction itself was particularly soft, with the high yield coming in 5.5bp above wider expectations, proxied by the BBG dealer poll. We also saw the cover ratio crater to the lowest level observed at a 40-Year auction since ’11. We would suggest that the ongoing market vol. and the lack of relative control exerted by the BoJ in this area of the curve deterred prospective bidders, while others were not willing to aggressively bid for access to the line owing to the same factors. The curve has steepened further post-auction, given the soft demand, with 40s now ~10bp cheaper on the day, while futures have softened to last trade -17 (well within the confines of the range observed since yesterday’s Tokyo close). 10-Year JGB yields continue to operate just above 0.250%, with the combination of a soft 40-Year auction and no pullback in 10-Year JGB yields seemingly dragging the BoJ back in to conduct a second round of fixed rate operations to enforce the upper end of its permitted 10-Year JGB yield trading band.

- There wasn’t much in the way of idiosyncrasies to go off when it came to the ACGB space. This evening’s budget has been subjected to the usual round of press leaks and pre-announcements, with more market focus set to fall on AOFM issuance matters surrounding the headline event (which will likely be released on Wednesday). YM -7.0 & XM +1.0 at typing. Longer dated cash ACGBs sit ~2.0bp richer on the day.

FOREX: Still JPY Watching

It was another session of JPY watching overnight, with senior Japanese government officials underscoring a need for orderly FX market moves, while continuing to point to vigilance and a sense of urgency when it comes to monitoring the FX space. We also saw Finance Minister Suzuki flag the need to avoid “negative JPY weakness,” which was enough to allow XXX/JPY crosses to run higher into the Tokyo fix (no firm pushback on JPY weakness was apparent in that particular verse), further boosted by fixing-related demand, before a firmer round of JPY strength kicked in (aided by the previously flagged rhetoric). We also saw the BoJ step in to defend the upper limit of its permitted 10-Year JGB yield trading band on two occasions, with limited, if any, tangible spill over apparent in the FX space. JPY managed to work itself to the top of the G10 FX leader board. USD/JPY is 50 or so pips lower on the day at typing, printing ~Y123.30, after showing as low as Y123.11 (Monday’s high was Y125.09). As our technical analyst flagged on Monday, at current levels, USD/JPY is extremely overbought and the most recent portion of the uptrend is very steep. A correction is overdue. Still, he also noted that technical signals suggest that the pair is likely to continue to appreciate in Q2 and a clear break of Y125.00 and Y125.86 would strengthen the bullish condition. To the downside, initial support is located at Monday’s low (Y121.97),

- Elsewhere, the USD fluctuated, with a lack of wider themes and headline flow apparent. Bursts of Tsy weakness provided some sporadic support for the greenback, but didn’t provide a consistent source of support (there were no notable extensions through Monday’s highs in yield terms), leaving the majority of the major USD crosses (excluding USD/JPY) little changed into European hours.

- A deepening of Shanghai’s COVID restrictions failed to meaningfully impact the space.

- The economic docket is rather light on Tuesday, with focus set to fall on the ongoing Russia-Ukraine summit in Turkey, in addition to addresses from Fed’s Williams & Harker, ECB’s de Cos & Riksbank’s Floden.

FOREX OPTIONS: Expiries for Mar29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0900(E722mln), $1.0950-60(E1.2bln), $1.0975(E1bln), $1.1000(E2.5bln), $1.1086-00(E1.2bln)

- GBP/USD: $1.3400(Gbp1.3bln)

EQUITIES: Mostly Higher As Crude Benchmarks Hold Monday’s Losses

Major Asia-Pac equity indices are mostly higher at typing, tracking a positive lead from Wall St. High-beta names across the region have caught a bid as major crude and commodity benchmarks have struggled to make headway in Asian hours, easing stagflation-related worry in some quarters.

- The ASX200 outperformed, building on an early lead to deal 0.8% firmer at writing. Technology and healthcare equities lead gains in the index, with the S&P/ASX All Technology Index sitting 2.6% better off at writing. The energy and materials sub-indices bucked the broader trend of gains amongst sub-index peers, on track to be the only sectors to close in the red for the day.

- The Hang Seng sits 0.4% higher at typing, with China-based tech leading gains for another day. The Hang Seng Tech Index trades 0.8% higher, with modest gains observed in internet giants Tencent, Meituan, and Trip.com. Real estate-related names within the Hang Seng remain under pressure as Hong Kong continues to pursue COVID-zero policies in the face of fresh daily case counts numbering in the thousands, seeing the Hang Seng Properties Index deal 0.4% softer at writing.

- The CSI300 underperformed against major regional equity index peers, dealing 0.4% softer come the lunch bell. Looking elsewhere domestically, Chinese real estate stocks broadly sold off as the list of developers declaring their inability to release financial results on time continues to grow, with sharp losses seen in names such as Sunac Holdings (-19.4%) and Shimao (-6.9%).

- U.S. e-mini equity index futures are virtually unchanged at typing, lacking momentum in either direction.

GOLD: Slightly Higher In Asia

Gold deals ~$3 firmer at writing to print ~$1,926/oz, operating around the lower end of Monday’s range. The precious metal has regained some poise in Asia as U.S. real yields and the Dollar have backed away from their earlier intra-day highs.

- To recap, bullion closed ~$35/oz lower on Monday, with the move lower facilitated by an uptick in U.S. real yields and the USD, in a session that saw nominal U.S. 10-Year Tsy yields hit levels not witnessed since May 2019.

- Turning to the war in Ukraine, both sides will begin two days of face-to-face ceasefire talks in Turkey later on Tuesday. FT source reports have pointed to a possible softening in Russian positions, dropping “denazification” and “demilitarization” demands while allowing Ukraine to seek admittance to the EU (but not NATO). Still, questions re: Ukrainian sovereignty surrounding Crimea and the separatist regions of Luhansk and Donetsk remain unresolved, with Ukrainian negotiators already stating that this is “the most critical point” from their perspective.

- On the technical front, the short-term outlook for gold is still bearish. Resistance is situated at $1,966.1/oz (Mar 24 high), while support is located at ~$1,901.9/oz (50-day EMA).

OIL: Lower As Shanghai Lockdown, Russia-Ukraine Talks In Focus

WTI is -$0.90 and Brent is -$1.20 at typing, operating a touch above Monday’s one-week lows as demand worry re: the two-stage lockdown of the Chinese city of Shanghai remains evident.

- To elaborate, Shanghai entered a phased lockdown on Monday despite earlier assurances to the contrary from city officials, with lingering worry evident re: other Chinese cities adopting similar pandemic control measures. BBG estimates have pointed to >60mn people in China either currently being under lockdown, or “facing one imminently”.

- Events surrounding the Russia-Ukraine conflict have applied further pressure, with hopes re: a diplomatic resolution seemingly rising ahead of scheduled ceasefire talks in Turkey later on Tuesday, raising expectations for a rapprochement between Russian crude exporters and international buyers.

- Elsewhere, RTRS source reports suggest that OPEC+ will stick to a 432K bpd target output increase at their policy meeting on Thursday, a slight increase (previous increases were set at 400k bpd) based on “internal recalculations” as opposed to consideration for ongoing tightness in global crude supplies. A note that the group has continued to miss its cumulative output targets, with IEA data showing a 1.1mn bpd shortfall in Feb.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/03/2022 | 0600/0800 | ** |  | SE | Retail Sales |

| 29/03/2022 | 0600/0800 | * |  | DE | GFK Consumer Climate |

| 29/03/2022 | 0645/0845 | ** |  | FR | Consumer Sentiment |

| 29/03/2022 | 0700/0900 |  | ES | Spain Retail Sales | |

| 29/03/2022 | 0830/0930 | ** |  | UK | BOE M4 |

| 29/03/2022 | 0830/0930 | ** | | UK | BOE Lending to Individuals |

| 29/03/2022 | 1230/0830 | * |  | CA | Payroll employment |

| 29/03/2022 | 1255/0855 | ** |  | US | Redbook Retail Sales Index |

| 29/03/2022 | 1300/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 29/03/2022 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 29/03/2022 | 1300/0900 | | US | New York Fed's John Williams | |

| 29/03/2022 | 1400/1000 | *** | | US | Conference Board Consumer Confidence |

| 29/03/2022 | 1400/1000 | ** | | US | JOLTS jobs opening level |

| 29/03/2022 | 1400/1000 | ** | | US | JOLTS quits Rate |

| 29/03/2022 | 1445/1045 | | US | Philadelphia Fed's Patrick Harker | |

| 29/03/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.