Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Chinese equities soar late doors on the back of reports of progress in talks aiming to keep U.S. equity markets open to Chinese issuers and China's politburo pledge to support the economy, even as health authorities vow to stick to Covid-Zero policy.

- Core FI come under pressure while risk-on flows take hold in G10 FX space ahead of next week's central bank meetings in the U.S. and Australia.

- Japanese financial markets are closed in observance of a public holiday.

BOND SUMMARY: Core FI Under Pressure, Japan Markets Closed

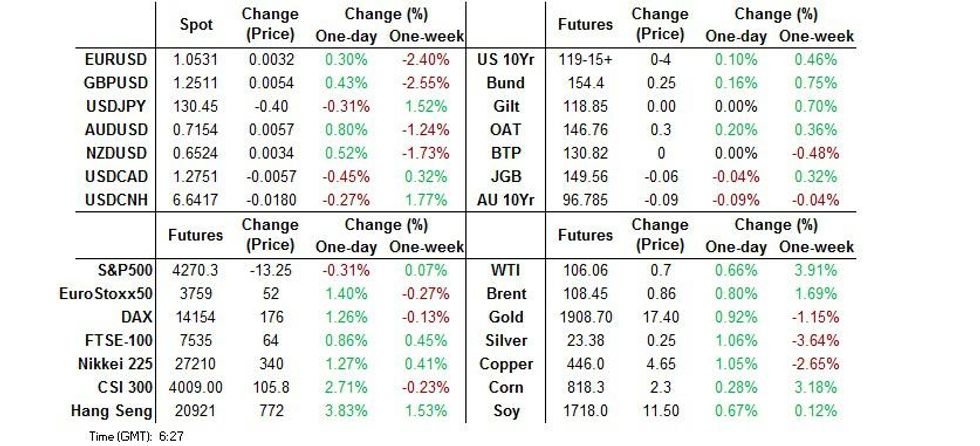

T-Notes and Aussie bond futures came under pressure amid little appetite for haven assets, with Japanese financial markets closed in observance of a public holiday. Reports of progress in talks aiming to keep U.S. equity markets open to Chinese issuers helped buoy market sentiment.

- Aussie bond futures came under pressure amid recovery in risk sentiment and expectations that the RBA will raise the cash rate come the end of its monetary policy meeting next week. Above-forecast inflation data released Wednesday put pressure on policymakers to take action, with the OIS strip fully pricing a 15bp hike. YM last deals -7.0 & XM -10.0, with bills sitting 2-9 ticks lower through the reds. Cash ACGBs extended their opening gains, with yields on 10-Year & 3-Year ACGBs printing best levels since 2014. When this is being typed, cash ACGB yields trade 6.7bp-9.7bp higher across the curve. The auction for A$1.0bn of ACGB 0.50% 21 Sep '26 & light AOFM issuance slate for next week provoked little if any market response.

- T-Notes quickly gave away opening gains and continued to lose altitude, as U.S. e-mini futures were trimming losses. TYM2 changes hands +0-02+ at 119-14, hovering just above session lows, with Eurodollars running +1.0 tick to -0.5 tick through the reds. Cash Tsys were closed until London hours due to a market closure in Tokyo. Focus in the U.S. turns to PCE data, MNI Chicago PMI & U. of Mich. Sentiment, with FOMC members already in their blackout period ahead of next week's monetary policy meeting.

AUSSIE BONDS: The AOFM sells A$1.0bn of the 0.50% 21 Sep ‘26 Bond, issue #TB164:

The Australian Office of Financial Management (AOFM) sells A$1.0bn of the 0.50% 21 September 2026 Bond, issue #TB164:

- Average Yield: 2.9040% (prev. 1.5720%)

- High Yield: 2.9100% (prev. 1.5750%)

- Bid/Cover: 4.6350x (prev. 4.0900x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield 9.2% (prev. 48.4%)

- Bidders 40 (prev. 40), successful 10 (prev. 14), allocated in full 5 (prev. 8)

FOREX: AUD Outperforms, USD Falters Ahead Of Next Week's Central Bank Meetings

The U.S. dollar index (DXY) traded on a heavier footing, moving away from a multi-year high printed on Thursday. The greenback was the worst performer among major currencies, with participants preparing for next week's FOMC meeting.

- Greenback weakness may have been exacerbated by reduced demand for safe havens, with U.S. e-mini futures chewing into their opening losses. This train of thought is supported by observed CHF weakness.

- The yen got some reprieve in the wake of Thursday's post-BoJ rout as Japan observed a public holiday. Liquidity over the next few days will be limited amid "Golden Week" market closures.

- The yuan was unfazed by the second consecutive firmer-than-expected PBOC fix. While spot USD/CNH weakened in initial reaction, it staged a strong rebound, facilitated by China's pledge to maintain its Covid-Zero policy. It took a nosedive thereafter, in response to the Politburo's pledge to boost support for the economy.

- The Aussie dollar outperformed ahead of next week's RBA MonPol meet. Data released on Wednesday provided evidence of runaway inflation, raising pressure on policymakers to take action despite ongoing election campaign.

- On the data front, preliminary EZ GDP & CPI data will take focus in European hours. Moving into the NY session, focus will turn to U.S. PCE, MNI Chicago PMI & U. of Mich. Sentiment as well as Canadian GDP.

- The central bank speaker slate includes ECB's de Cos and SNB's Jordan, with Russia's central bank set to announce its rate decision.

FOREX OPTIONS: Expiries for Apr29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0565-75(E2.0bln), $1.0600(E838mln), $1.0650(E288mln), $1.0700(E2.9bln), $1.0785-90(E587mln)

- USD/JPY: Y124.00($1.4bln), Y126.75($500mln)

- EUR/GBP: Gbp0.8475(E751mln)

- USD/CAD: C$1.2850($690mln)

- USD/CNY: Cny6.5400($500mln), Cny6.5500($570mln), Cny6.6500($560mln)

ASIA FX: Yuan Halts Sell-Off As Politburo Vows To Support Economy

The yuan was dumped despite a firmer than expected PBOC fix and broader greenback weakness, provided some reprieve to most Asia EM currencies. China's determination to continue with draconian Covid-19 countermeasures weighed on the redback ahead of the long weekend in China, before Politburo communique helped soothe the nerves.

- CNH: The PBOC continued to lean against redback weakening by maintaining appreciation bias in the daily yuan fixing, but to no avail. The People's Bank set the mid-point of USD/CNY trading band 37 pips shy of sell-side estimate after a 36-pip miss on Thursday. Spot USD/CNH shed >100 pips in the initial reaction but was bought on the dip and recoiled towards new cycle highs. The pair extended gains as China's health officials pledged to stick to their Covid-Zero policy, which pushed dozens of Chinese cities into lockdowns. It took a nosedive thereafter, in response to the Politburo's pledge to boost support for the economy and amid reports that the U.S. and China are in talks to keep U.S. stock markets open for Chinese issuers (albeit have not reached agreement quite yet).

- KRW: Spot USD/KRW eased off, while staying within Thursday's range. South Korean Finance Ministry resumed verbal warnings on recent won depreciation, with Vice FinMin Lee noting that the authorities stand ready to take market stabilisation steps in case of abrupt one-sided moves. There was little reaction to South Korea's industrial output data, with annual growth in manufacturing production missing expectations, despite unexpected monthly increase.

- MYR: Spot USD/MYR faltered, moderating its weekly gain. BNM Gov Shamsiah Yunus told Bernama news agency that the central bank is ready to use tools at its disposal to prevent "sharp or wide swings in the value of the ringgit".

- THB: Spot USD/THB slipped as recent bullish momentum petered out. The Finance Ministry noted that baht weakness boosts Thai export competitiveness, but also raises oil import costs, with the government determined to help mitigate the impact of higher energy prices. Participants awaited the release of Thailand's BoP data later today.

- PHP: Peso resumed losses despite little in the way of notable local headlines. The local Covid-19 task force decided to maintain the lowest alert level in Metro Manila for the next two days, which covers the upcoming presidential election.

- IDR: Indonesian markets were shut in observance of a public holiday.

EQUITIES: Mostly Higher As Chinese Equities Catch A Bid On Politburo Pledge

Asia-Pac equity indices are mostly higher at typing, bucking negative reception from an after-market earnings beat from mega-caps Amazon and Apple. Chinese stocks are in the midst of a broad surge on an announcement from the Politburo pledging support to meet the country’s 5.5% growth target for ‘22, with high-beta stocks outperforming.

- The Chinese CSI300 is 1.5% firmer at typing, rising above neutral levels after aforementioned reports re: the Politburo’s vows to support economic growth. Notably, underperformance in a gauge of real estate equities was broadly reversed, with the government specifically voicing support for the industry.

- The Hang Seng Tech Index was sharply bid towards the tail-end of the morning session and currently sits >10% firmer at typing. Large-caps such as Tencent, Alibaba, and JD.com contributed outsize gains to the index, building on gains made before the break.

- Focusing on the Politburo meeting, policymakers doubled down on their commitment to China’s 5.5% growth target for ‘22 through stronger “macro adjustments”, while pledging support to boost domestic consumption as well, likely again feeding into speculation for policy easing in the coming weeks.

- On the topic of Chinese consumption, several cities/regions have issued at least several hundred million yuan in coupons, vouchers, and digital “red envelopes” to residents, in an attempt to spur spending over the upcoming May Day holidays.

- U.S. e-mini equity index sit flat to 0.9% weaker at typing, with the NASDAQ leading losses. All contracts however operate clear of Thursday’s troughs, and have continued to move higher from cycle lows made on Tuesday.

GOLD: Hovering Around $1,900/oz As May FOMC Draws Closer

Gold sits ~$6/oz higher, printing ~$1,900/oz at typing. The precious metal is back from session highs at (~$1,905.9/oz), but operates clear of Thursday’s best levels.

- The precious metal builds on a ~$8/oz higher close on Thursday, after rising off session lows at $1,872.2/oz on support from a downtick in U.S. real yields despite a fresh cycle high in the USD (DXY).

- Gold is on track to close ~$40/oz lower for the month, possibly representing its worst month in over half a year, with headwinds evident above the $2,000/oz price level. The DXY has continued to make fresh successive cycle highs throughout April while U.S. real yields have pushed higher as well, with 10-Year real yields hovering a touch below neutral levels (after briefly breaking into positive territory for the first time in over two years on Apr 20).

- Looking ahead, U.S. PCE data is expected to draw some focus, with MNI Chicago PMI and U. of Michigan Consumer Sentiment headlining data releases as well.

- From a technical perspective, gold has formed initial support at Thursday’s low of $1,872.2/oz, while resistance remains some distance away at around ~$1,941.3/oz (20-Day EMA).

OIL: WTI Reclaims $100 On Possible EU Sanctions; China Vows Quicker Action On COVID

WTI and Brent are flat to a little higher at typing, operating a shade below their respective two-week and one-week highs made on Thursday.

- To recap, major oil benchmarks caught a bid on Thursday after BBG source reports suggested that Germany plans to back a phased ban in Russian crude. Sources also pointed to a sixth EU sanctions package on Russian goods likely being put up for approval by next week, although the “precise mechanics” of an embargo on Russian oil is reportedly still in the works.

- Looking to China, fresh COVID case counts in Shanghai for Thursday surged to ~15.6K cases, reversing five consecutive days of declines after reporting ~10.7K cases for Wednesday. Authorities however pointed out on Friday that the city has continued to ease restrictions, with only around ~5mn of the city’s >25mn population currently under full lockdown. Zooming out, case counts in Beijing have also crept upwards, although overall cases in China have encouragingly remained below 20K.

- Turning to pandemic control measures, Chinese regulators on Friday re-affirmed the country’s COVID-zero strategy, but stressed that they may not reach for massed city-wide lockdowns in the future. Elsewhere, Jilin province (pop. ~24mn)in the country’s northeast reported a 7.9% Y/Y decline in GDP on Thursday, coming after the province had been put under lockdown since Mar 11.

- Up next, participants may be on the lookout for COVID-related progress in the e-commerce hub of Hangzhou (pop. ~10mn), after the city started a mass testing drive earlier in the week.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/04/2022 | 0530/0730 | ** |  | FR | Consumer Spending |

| 29/04/2022 | 0530/0730 | *** | | FR | GDP (p) |

| 29/04/2022 | 0600/0700 | * |  | UK | Nationwide House Price Index |

| 29/04/2022 | 0645/0845 | *** | | FR | HICP (p) |

| 29/04/2022 | 0645/0845 | ** | | FR | PPI |

| 29/04/2022 | 0700/0900 | *** |  | ES | GDP (p) |

| 29/04/2022 | 0800/1000 | *** |  | DE | GDP (p) |

| 29/04/2022 | 0800/1000 | *** |  | IT | GDP (p) |

| 29/04/2022 | 0800/1000 | ** |  | EU | M3 |

| 29/04/2022 | 0900/1100 | *** | | IT | HICP (p) |

| 29/04/2022 | 0900/1100 | *** | | EU | HICP (p) |

| 29/04/2022 | 0900/1100 | *** | | EU | GDP preliminary flash est. |

| 29/04/2022 | 1230/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 29/04/2022 | 1230/0830 | ** |  | US | Personal Income and Consumption |

| 29/04/2022 | 1230/0830 | ** | | US | Employment Cost Index |

| 29/04/2022 | 1345/0945 | ** | | US | MNI Chicago PMI |

| 29/04/2022 | 1400/1000 | *** | | US | Final Michigan Sentiment Index |

| 29/04/2022 | 1500/1100 | | CA | Finance Dept monthly Fiscal Monitor (expected) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.