Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- NASDAQ 100 futures lead e-minis higher, supporting broader sentiment. China's spreading COVID-19 outbreak keeps a lid on risk appetite.

- Antipodean FX outperform after Australian federal election and ahead of this week's RBNZ monetary policy meeting.

- On the data front, German Ifo Survey will take focus from here. Comments from ECB's de Cos, Holzmann, Nagel & Villeroy, Fed's Bostic & BoE's Bailey are on tap.

BOND SUMMARY: Core FI Lose Altitude Amid Uptick In E-Minis, Despite China COVID Worry

Core FI came under pressure in Asia as an uptick in U.S. e-minis supported market sentiment. That said, uncertain outlook for China's COVID-19 outbreak kept a lid on risk, preventing a deeper bond sell-off.

- T-Notes extended their pullback from Friday's peak (120-08+) before stabilising. TYM2 changes hands -0-06 at 119-30 as we type, while Eurodollars run 1.0-4.0 ticks lower through the reds. Cash Tsy yields sit 2.4-3.5bp higher, curve is tad flatter. Fed's Bostic will discuss the economic outlook later today.

- JGB futures quickly gave away their opening gains. JBM2 trades at 149.80, up 2 ticks versus last settlement. Cash JGB curve has slightly flattened, with the super-long end leading gains. Local headline flow was fairly light, centred around U.S. Pres Biden's ongoing visit to Tokyo.

- Aussie bonds went offered as weekend federal election brought a decisive victory for Labor, with Anthony Albanese swiftly sworn in as new Prime Minister. While votes are still being counted, the risk of a hung parliament has narrowed. YM last -0.5 & XM +1.0, both near session lows. Bills trade unch. to +2 ticks through the reds. Cash ACGB curve twist flattened, with yields last seen +0.8bp to -2.3bp. RBA's Kent said the Reserve Bank is now in QT phase, adding that models estimate the neutral level of cash rate at around 2-3%.

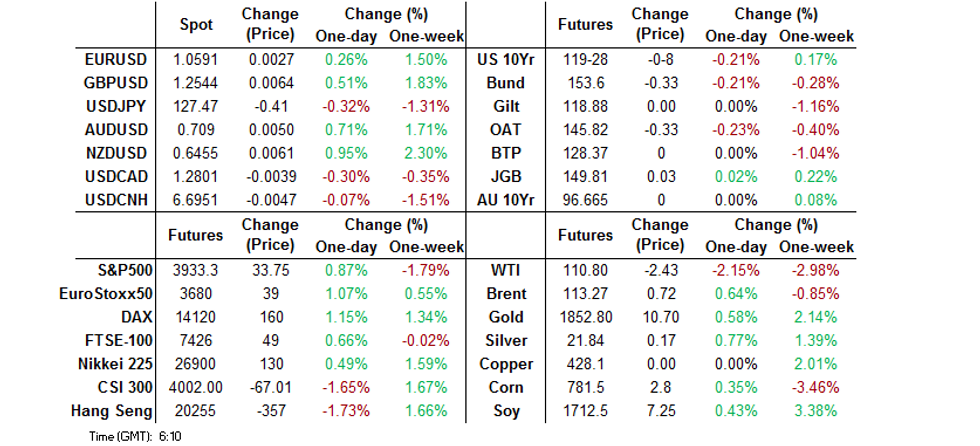

FOREX: USD Weaker; NZD Outperforms

USD sentiment remains on the back foot, sitting weaker against all the majors, while NZD and AUD are seeing outperformance.

- NZD/USD rose more than 1% today, getting close to 0.6470 before settling back at 0.6450. Higher US equity futures has improved risk appetite, with mixed readings in Asian markets not impacting sentiment at this stage.

- The RBNZ is main event risk this week in NZ, with the market expecting a 50bps hike, which supported by the RBNZ Shadow Board view. NZ 2yr swap rates are around 5bps higher on the day. A 50bps hike is close to fully priced for this week's meeting.

- The AUD has been dragged higher by NZD performance, although has unperformed modestly. AUD/USD is back at 0.7090, +0.70% higher on the day, while the AUD/NZD cross is back sub 1.1000. With the election now behind us and solid chance of Labor holding a small outright majority, tail risk around political uncertainty has been removed for the AUD.

- Elsewhere, the USD remains on the backfoot. US yields are higher on the day, but the differentials with the majors fell sharply last week. EUR/USD is back close to the 1.0600 handle, while USD/JPY is down through 1.2750. GBP/USD back towards 1.2550.

- On the data front, German Ifo Survey will take focus after Asia hours. Comments from ECB's de Cos, Holzmann, Nagel & Villeroy, Fed's Bostic & BoE's Bailey are on tap.

ASIA FX: Lagging USD Sell-Off

Asian FX is generally lagging G10 FX strength against the USD. China and Hong Kong equities have given back some of last week's rebound. Uncertainty around the China Covid situation is not helping at the margin. Shanghai is moving ahead with re-opening plans, but cases continue to rise in Beijing.

- CNH: USD/CNH continues to find selling interest above 6.7000 and we also had a slightly stronger than expected CNY fix today. Still, the currency hasn't been able to build on last week's rebound. Weaker equity market sentiment and some covid related headwinds has tempered momentum.

- KRW: 1 month USD/KRW is back sub 1270, although today's export data for the first 20 days of May continued to show slowing export momentum. FX stability was a focus point at the US and South Korean President's summit over the weekend.

- IDR: USD/IDR has edged higher through the session, back above 14660. Tomorrow's BI decision is expected to see rates left on hold. Elsewhere, FinMin Indrawati will speak on the 2022 state budget, while the government will review the remaining COVID-19 restrictions today.

- SGD: Has outperformed today, likely reflecting G10 FX strength against the USD. USD/SGD back to 1.3750. CPI data out shortly.

- PHP: USD/PHP is higher from best levels last week. We sit back close to 52.30. Higher oil is like not helping (Brent back above $113/bbl). BSP Gov Diokno said that the exit from easy monetary policy will be "gradual, well-communicated and outcome-based," with the central bank ready to take pre-emptive action if there are signs of inflation expectations becoming dis-anchored.

- INR: Bond yields are higher, as government cut taxes on fuels and boosted fertilizer subsidies in order to bring down inflation. Market expecting higher borrowing to meet funding shortfall. USD/INR 1 month back sub 78.00, which remains a short term pivot point.

EQUITIES: Firmer E-Minis Support Sentiment But China's COVID-19 Situation Weighs

U.S. e-minis found poise after S&P 500 avoided a bear market close on Friday, despite extending its losing streak (on a weekly basis) to the worst rout in two decades. While the uptick in U.S. equity-index futures supported risk sentiment, murky outlook for China's COVID-19 outbreak complicated the overall picture, as Beijing reported a record number of new infections during the current outbreak.

- Major regional indices (ex-China) trade flat or in the green, trimming initial gains as the session progressed.

- China's equity benchmarks provided a notable exception and retreated from the off amid weakness in the local tech space.

- E-minis are 0.7-1.2% better off at typing, with the NASDAQ 100 leading.

GOLD: Building On Last Week's Gains

Gold is up a further 0.40% today, building on last week's gains of 1.92%, which was the strongest weekly performance for the metal since the start of March.

- Gold is trading back through $1850, its highest levels since May 12th.

- Concerns around the global growth backdrop, particularly last week with China growth downgrades and US business survey misses, has no doubt aided the safe haven appeal of the metal.

- The fact that growth concerns are creeping into US sentiment, which has been a headwind for USD performance, has also likely aided the turnaround. The DXY was down 1.35% last week, its first drop in 7 weeks.

- USD weakness has continued today (DXY off a further -0.44%).

- US real yields are unlikely to have been a key driver of gold sentiment, but stability in yields has also likely helped at the margin.

OIL: Crude Tad Firmer, WTI Shows Above $111/bbl

WTI & Brent have edged higher as the new week got under way with the risk switch flicked to on.

- WTI briefly showed above the $111 mark and last trades at $110.70/bbl, up ~$0.40 from its previous settlement level. Brent last seen at $113.20/bbl, up ~$0.65 versus last settlement.

- Weekend headline flow centred around Russia's participation in the OPEC+ framework. Saudi Arabia's energy minister told the FT that Riyadh wanted "to work out an agreement with OPEC+ ... which includes Russia," frustrating U.S.-led efforts to isolate Moscow over its invasion of Ukraine and undermine its critically important oil industry used to fund the war machine.

- Latest COVID-19 headlines out of China failed to shed much light on the outlook. Shanghai reported no community infections, but Beijing's daily cases rose to a new high since the current outbreak started.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/05/2022 | 0800/1000 | *** |  | DE | IFO Business Climate Index |

| 23/05/2022 | - |  | EU | ECB Lagarde & Panetta at Eurogroup Meeting | |

| 23/05/2022 | 1300/1500 | ** |  | BE | BNB Business Sentiment |

| 23/05/2022 | 1530/1130 | * |  | US | US Treasury Auction Result for 13 Week Bill |

| 23/05/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 23/05/2022 | 1600/1200 | | US | Atlanta Fed's Raphael Bostic | |

| 23/05/2022 | 1615/1715 |  | UK | BOE Governor Bailey Panels Discussion |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.