Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Two-way trade in Chinese equities saw a softer open on growth worries (in lieu of Chinese Premier Li's Wednesday warning), before the latest positive COVID-related news flow and modest Chinese support measures allowed the space to more than reverse early losses.

- USD/CNH firmed even as Chinese equities recovered, with the CNY suffering on the wider Chinese growth worry and pull lower in Chinese government bond yields.

- U.S. GDP (second reading), pending home sales and weekly jobless claims as well as Canadian retail sales take focus from here. Meanwhile, central bank comments are due from Fed's Brainard & Daly as well as ECB's Centeno & de Cos.

US TSYS: Off Worst Levels Of Asia Trade, Little Changed Into European Hours

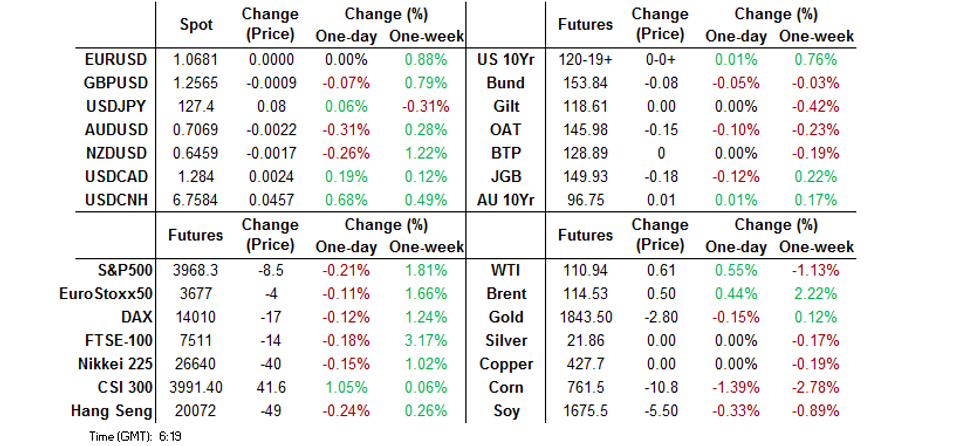

TYM2 last deals +0-00+ at 120-19+, 0-01+ shy of the peak of its 0-09 Asia range, while cash Tsys run at virtually unchanged levels across the curve.

- Tsys bounced from cheapest levels of Asia-Pac dealing, after initially being helped lower by a light bid in e-minis and the likes of the Nikkei 225 (as some flagged the potential for the Fed to pause its expeditious tightening cycle around year-end after a reference in the May meeting minutes). A heavy start for Chinese equities allowed the space to find a bit of a base, with a subsequent recovery from Chinese equities failing to provide any meaningful headwinds for Tsys.

- E-minis are still softer on the day, reversing early Asia gains on worries re: Chinese growth, while some pointed to tech giant Apple’s move to pay higher wages as another headwind for the space and an explanatory factor behind the NASDAQ 100 leading the way lower.

- There hasn’t really been much in the way of meaningful macro headline flow to digest, outside of China matters. This included China revealing its latest, limited fiscal and credit support measures, the partial re-opening of schools in Shanghai from early June and an uptick in throughput at the port of Shanghai.

- Thursday’s NY session will include weekly jobless claims & pending home sales data, the latest Kansas City Fed manufacturing activity survey, revised Q1 GDP readings and 7-Year Tsy supply. Elsewhere, Fedspeak will come from San Francisco Fed President Daly (’24 voter) and Vice Chair Brainard (on digital currencies).

JGBS: Futures Soften Late In The Day, Curve Steeper, 20s Lead Weakness

JGB futures have come under pressure ahead of the bell, with nothing in the way of an overt catalyst apparent, as the contract hits fresh session lows in recent dealing, last -18 on the day. The move comes as 20s cheapen in cash JGB trade, while 30s and 40s outperformed 20s in the wake of a relatively solid round of 40-Year JGB supply. The major cash JGB benchmarks run 0.5-3.0bp cheaper across the curve.

- This comes after a firmer Nikkei 225 resulted in the bear steepening of the JGB curve during early Tokyo dealing, while the paring of the Nikkei’s early gains failed to provide any meaningful support for the space.

- In terms of auction specifics, 40-Year JGB supply saw the cover ratio tick away from the multi-year low observed at the previous 40-Year auction (although it still held below its 6-auction average of 2.53x), while the high yield is lower than wider expectations evident ahead of the auction (which stood at 1.085%). The steep domestic yield curve (in both domestic and international terms) and short-term stability in government bond markets, coupled with the fact that 40-Year yields are near cycle highs, seemingly enticed bidders, as we suggested may be the case in our auction preview.

- Elsewhere, last week’s international security flow data revealed that foreign investors were net buyers of Japanese bonds for a second consecutive week, registering the largest round of net weekly purchases seen since March. FX hedging cost-related yield pickup and the BoJ’s continued insistence that it will stick with its current policy settings likely facilitated the bid.

- Tokyo CPI data headlines the domestic docket on Friday.

AUSSIE BONDS: Looking Offshore For Moves

Aussie bonds have traded on the previously outlined swings in risk appetite, operating off worst levels of the session at typing, after dipping lower alongside U.S. Tsys in early Sydney trade.

- That leaves YM -0.5 & XM +1.0, while wider cash ACGB trade sees a pivot around the 7-Year zone as the curve twist flattens, with 30s richening by ~2.5bp.

- The 3-/10-Year EFP box has twist flattened.

- Bills run -4 to +1 through the reds, twist flattening.

- Local data had no tangible impact on the space, with private capex providing soft GDP partial data (at least on face value) for a second consecutive day (-0.3% Q/Q vs. BBG median of +1.5%), although there was a positive revision for Q421 (up to +2.3% Q/Q from +1.1%). We also saw a much firmer than expected markup in firms’ 22-23 capex plans, while the GDP-centric equipment, plant and machinery capex category was firmer than the headline, rising by 1.2% Q/Q.

- Friday will see A$800mn of ACGB Jun-31 supply, the release of the AFM weekly issuance slate and monthly domestic retail sales data.

JAPAN: Bond Buying Dominates Weekly International Security Flow Data

Bonds once again stole the show in the latest round of Japanese weekly international security flow data.

- Note that Japanese investors lodged their second consecutive week of net purchases of foreign bonds, likely aided by the widening recessionary fears observed across much of the globe, which is drawing questions re: G10 central bank terminal rates. This was the largest round of net weekly purchases lodged since mid-January and also represents the first back-to-back round of weekly net purchases of foreign bonds observed since January.

- Foreign investors were net buyers of Japanese bonds for a second consecutive week, registering the largest round of net weekly purchases seen since March. FX hedging cost-related yield pickup and the BoJ’s continued insistence that it will stick with its current policy settings likely facilitated that particular bid.

- Japanese investors reverted to net buying of foreign equities, registering net purchases for the fifth week in six, while foreign investors reverted to incremental net buying of Japanese equities, registering net purchases for the seventh week in eight.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

|---|---|---|---|

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | 627.0 | 373.4 | -905.5 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | 326.6 | -57.4 | 1400.5 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | 1281.6 | 374.5 | 1132.7 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | 4.1 | -345.4 | 237.0 |

FOREX: G10 Volatility Subdued, Yuan Goes Offered

Risk appetite waned as U.S. e-minis pared earlier gains, but there was no obvious rush to safety. European FX outperform at the margin as we head for the London session, with G10 currency pairs holding tight ranges.

- Offshore yuan retreated despite Shanghai's reported progress on clearing ports and re-opening schools. The overhang of Premier Li's suggestion that the local economy is in some aspects faring worse than in 2020 loomed large.

- The BoK raised its key interest rate by 25bp, in line with expectations. Newly installed Governor Rhee vowed to place more focus on inflation. The won showed a muted reaction.

- U.S. GDP (second reading), pending home sales and weekly jobless claims as well as Canadian retail sales take focus from here. Comments are due from Fed's Brainard as well as ECB's Centeno & de Cos.

ASIA FX: USD/CNH Higher On Growth Fears

The main story today has been the resurgent USD/CNH trend. The pair has climbed +0.60% from NY closing levels, as growth fears weigh. Most other USD/Asia pairs have been dragged higher as a result.

- CNH: USD/CNH is pushing back through 6.7500, as the Premier's warning on the growth backdrop has hurt sentiment today. Local equities are holding up reasonably well, but we have seen lower onshore yields, while the fixing bias was close to neutral. The 10yr bond yield is threatening to breakdown to fresh multi-month lows (sub 2.74%, current is 2.75%).

- KRW: 1 month USD/KRW has been dragged higher by USD/CNH moves, now back close to 1269 (now 0.20% higher on the day). Earlier we had a hawkish 25bps hike by the BoK, which sent onshore yields up but this did little to aid the won.

- SGD: USD/SGD is up only a touch higher from NY closing levels, so some outperformance versus the rest of the region. IP figures came in mixed, with the MoM weaker than expected but YoY still solid at +6.2%.

- MYR: USD/MYR is higher but spot remains sub 4.4000 for now. Malaysia's consumer prices rose 2.3% Y/Y in April, matching consensus forecast. But food inflation reached a four-year high of +4.1% Y/Y, led by firmer dairy prices.• The Agriculture Ministry followed up noting that it held a meeting on measures to address food security issues. The Ministry will present its suggestions at the May 30 Cabinet meeting.

- PHP: USD/PHP is also higher, with spot close to 52.50, but in line with the regional trend. Bloomberg reported that Philippines President-elect Marcos will tap BSP Gov Diokno as the new Finance Secretary. Diokno also told Bloomberg Wednesday that the benchmark policy rate will likely be raised by another 25bp at the next MPC meeting.

- INR: USD/INR is drifting higher in early trade, with spot pushing up to 77.60. Moves towards 77.70 or slightly above have not been sustained in recent sessions, so be mindful of intervention risk. A positive energy price backdrop (Brent crude above $114/bbl) can still test the authorities resolve though.

EQUITIES: Chinese Equities Bounce, E-Minis Marginally Lower

A heavy start for Chinese equities (in the wake of Chinese Premier Li’s Wednesday warning re: the health of the Chinese economy) weighed on wider risk appetite in early Asia trade, with e-minis and the likes of the Nikkei 225 unwinding their opening bid.

- The unveiling of the latest round of fiscal and credit support measures in China, coupled with the partial re-opening of schools in Shanghai from early June & an uptick in throughput at the Shanghai Port (to ~95% of capacity) then facilitated a rebound for Chinese equities, with the CSI 300 now ~0.6% firmer on the day, although wider equity indices were a little more reticent to go bid. The Nikkei 225 is little changed on the day.

- E-Minis sit 0.2-0.5% below settlement after pulling lower alongside the early move in Chinese equities. Some suggested the underperformance in the NASDAQ contract could be attributed to tech giant Apple outlining a round of wage hikes given the current inflationary burden felt by households.

- Note that some pointed to the minutes covering the latest U.S. Federal reserve meeting as a source of support for e-minis in late NY/early Asia trade, with suggestions that the Fed may pause for breath around the end of the year after the current, expeditious round of tightening ends (based on a reference in the text of the minutes).

GOLD: Loses Further Momentum

Gold has spent much of the Asia session on the back foot, dipping to $1846, close to 0.40% below NY closing levels at the time of writing. The overnight low was just below $1845.

- Today's price action has been against a mixed cross asset backdrop. Regional Asian equities are firmer/resilient, while US equity futures have drifted lower through the afternoon session.

- US yields have been fairly steady, but that mirrors the overnight session, with the 10yr holding fairly close to 2.75%. US real yields edged down overnight to 0.19%, we were at 0.26% at the start of the week. This didn't sentiment much overnight in gold though.

- The USD is mixed, with the DXY a touch higher, while A$ and NZD have drifted down. USD/CNH is up close to 0.50% on the day, as China growth concerns have weighed. By extension this should weigh on the global growth outlook but this hasn't helped haven demand for gold today.

OIL: Marginally Higher In Asia

Crude futures were subjected to two-way trade within confined ranges during Asia-Pac hours, with an early downtick for Chinese equities on growth fears (after Premier Li’s Wednesday warning re: the Chinese economy) applying some modest pressure. That was before the announcement of a partial school re-opening in the Chinese city of Shanghai, fiscal support to boost consumption in the Chinese city of Shenzhen and news of another uptick in throughput at the Shanghai Port (to 95% of capacity) combined to facilitate a recovery from worst levels. WTI & Brent sit ~$0.50 above their respective settlement levels at typing as a result.

- Tight U.S. refined product markets ahead of the U.S. driving season and the ongoing saga re: the next round of EU sanctions on Russia continue to provide the wider areas of interest for the space.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/05/2022 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 26/05/2022 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 26/05/2022 | 1100/0700 | * |  | TR | Turkey Benchmark Rate |

| 26/05/2022 | 1230/0830 | ** |  | CA | Retail Trade |

| 26/05/2022 | 1230/0830 | * | | CA | Payroll employment |

| 26/05/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 26/05/2022 | 1230/0830 | *** | | US | GDP (2nd) |

| 26/05/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 26/05/2022 | 1230/0830 | ** | | CA | Retail Trade |

| 26/05/2022 | 1400/1000 |  | MX | Mexican central Bank policy meet minutes | |

| 26/05/2022 | 1400/1000 | ** | | US | NAR pending home sales |

| 26/05/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 26/05/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 26/05/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 26/05/2022 | 1600/1200 | | US | Fed Vice Chair Lael Brainard | |

| 26/05/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.