Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Chinese equities recover from early lows aided by localised support for the property sector, some upbeat sell-side musings re: Chinese equities and suggestions that China may pursue “extraordinary” measures to combat the divergence in upstream and downstream manufacturers’ profitability came to the fore.

- The bid in Chinese equities allowed the yuan to strengthen vs. the USD.

- Central bank speak from the Fed, ECB & BoE headlines the wider docket on Monday, while the U.S> will observe the Juneteenth hoiday, limiting wider liquidity.

US TSYS: Futures Unwind Early Losses

TYU2 trades 0-04 shy of the peak of its 0-18 Asia range, last dealing +0-00+ at 116-06+, on sub-average volume of ~65K. The modest volume came about on the observance of the Juneteenth holiday in the U.S., with cash Tsys closed until Tuesday’s Asia-Pac session, while Tsy futures will be subjected to curtailed trading hours on Monday.

- Weekend news flow was headlined by Fed Governor Waller’s latest round of hawkish rhetoric (pointing to support for a 75bp rate hike at the July FOMC), confirmation that U.S. President Biden aims to speak with Chinese President Xi “soon,” as well as utterances from U.S. Tsy Sec Yellen re: high inflation being “locked in” for the remainder of ’22 & the likelihood of a roll back of some of the tariffs levied on China by the Trump admin.

- These matters, coupled with an early uptick for e-mini futures, applied pressure to U.S. Tsy futures at the re-open.

- Cross-asset correlations were at the fore thereafter, with broader gyrations in e-minis and Chinese equities in the driving seat. Tsy futures recovered from intraday lows as e-minis briefly moved into negative territory and Chinese equities struggled in early dealing, before working away from best levels as a rebound in Chinese property developer stocks (aided by another round of localised policy support), some upbeat sell-side musings re: Chinese equities and suggestions that China may pursue “extraordinary” measures to combat the divergence in upstream and downstream manufacturers’ profitability came to the fore.

- Note that Monday will see St. Louis Fed President Bullard (’22 voter) comment on inflation and interest rates.

US: Juneteenth Holiday To Be Observed On Monday

The U.S. will observe the Juneteenth holiday on Monday, which will result in closures/abbreviated trading hours for U.S. markets. A summary of trading hours across the major exchanges can be found below:

JGBS: Futures Erase Some Of Overnight Gains As Curve Steepens

JGB futures gave back a chunk of their overnight session gains as global core FI markets eased a little in early Tokyo trade, although the contract remained comfortably above neutral levels on the BoJ’s continued ultra-easy policy stance and market mechanism tweaks that look to ensure that the Bank can uphold the boundary located at the upper end of its of permitted 10-Year JGB yield range. The contract then stuck to a very tight range thereafter, looking through swings in wider markets. That leaves the contract +53 as we move towards the Tokyo close.

- Cash JGB trade sees most of the major benchmarks running cheaper on the day (to the tune of 0.5-3.5bp), with 10-Year JGB yields a touch below 0.24% and the curve bear steepening. 7s provide the exception to the trend, with the BoJ’s commitment to its ultra-easy policy settings at the backend of last week (coupled with the market-based policy tweaks we fleshed out earlier) supporting futures, with cash 7s “catching up” early this week.

- Weekend commentary saw both of the political parties that form Japan’s ruling coalition support the BoJ’s monetary policy settings, although the latest Nikkei survey revealed that 46% of the public would prefer a move away from the current ultra-loose monetary settings, while 36% of those surveyed favour the Bank’s current approach.

- Elsewhere, PM Kishida’s cabinet has seen a downtick in support in the latest round of opinion polls.

- Looking ahead, Tuesday will see the release of the outdated minutes from the BoJ’s April meeting, in addition to the latest scheduled round of BoJ Rinban operations (covering 1- to 3-, 5- to 10- & 25+-Year JGBS).

JGBS: Tussle Of BoJ & Bond Vigilantes Sees Vol. Surge To New Post-GFC Peak

The BoJ’s status as the last dove standing in the major global central bank sphere, punctuated by its continued insistence that it will stick to its current ultra-loose monetary policy settings, has resulted in market participants testing the BoJ’s will.

- To date, the Bank has taken well-documented action in defending the upper end of its permitted -/+0.25% 10-Year JGB yield trading band, including daily fixed rate operations, unscheduled Rinban operations and a willingness to tweak parameters of its market-focused policy settings when weakness in JGB futures has become evident.

- This combination of speculation & BoJ action has resulted in the S&P/JPX JGB VIX surging to highest levels observed since the global financial crisis of ’08.

Fig. 1: S&P/JPX JGB VIX Index

Source: MNI - Market News/S&P/JPX/Bloomberg

Source: MNI - Market News/S&P/JPX/Bloomberg

AUSSIE BONDS: Tighter Purse Strings And Global Sentiment at The Fore

The previously outlined cross-asset moves were in the driving seat in early Sydney dealing, which leaves YM +4.5 & XM +7.5 as we move towards the close, with an early blip lower more than reversed. Tightening in EFPs suggest that receive side flows in swaps may have aided the richening.

- Elsewhere, a weekend AFR interview with Australian Treasurer Chalmers may have provided the ACGB space with more of a reason to go bid as e-minis pulled away from best levels of the day and Chinese equities struggled in early dealing. To recap, Chalmers noted that the new government will make deeper cuts than it initially envisaged when its comes to the October Budget. He also suggested that the government will then look to build public support for a “second-term agenda of tough revenue and spending measures needed to repair the nation’s finances.” Nonetheless, bonds are off best levels, aided by a recovery in both e-minis and Chinese equities.

- Elsewhere, AFR sources noted that "Chalmers has overridden Reserve Bank of Australia governor Philip Lowe’s wishes and will appoint a panel of independent experts to review the central bank, including a monetary policy expert from overseas. Dr Lowe, who the treasurer has said he has a “mountain of respect for”, has pushed for a joint RBA-Treasury review of the central bank, similar to a model employed by Canada, to ensure the RBA’s independence from politics and to protect its reputation." This didn’t have anything in the way of tangible impact on the space.

- When it comes to calendar risk, participants were already looking ahead to Tuesday, when we will get the latest address from RBA Governor Lowe, the release of the minutes from the RBA’s June monetary policy meeting and the Bank’s review of its yield targeting mechanism.

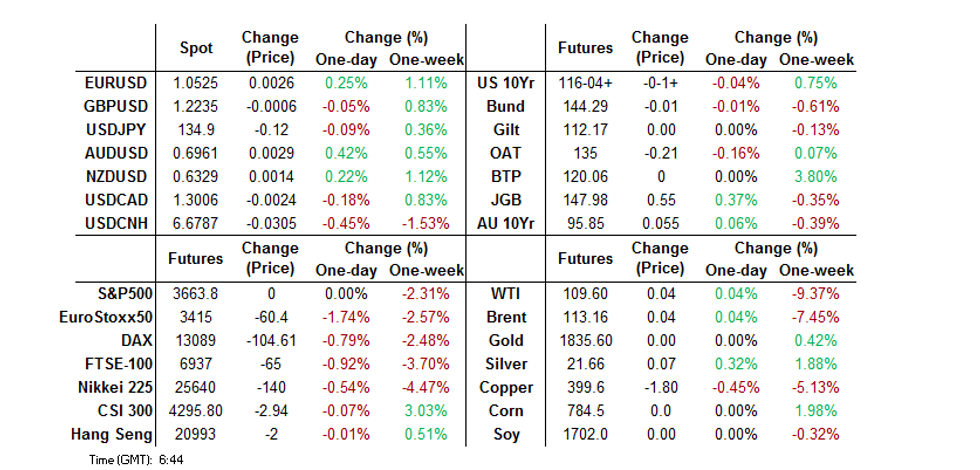

FOREX: USD Loses Ground

The USD has tracked lower, with the DXY around -0.30% below NY closing levels from last Friday to 104.40. Firmer equity futures and strong leads from China stocks regionally, appear the main catalysts for this dip.

- EUR/USD was sold early, as French leader Macron lost his outright majority and will have a tougher time pushing through his agenda. Still, we bounced from 1.0460/65 and last track just under 1.0530. This could become a renewed focus point once London/EU markets swing into action.

- USD/JPY tried to breach 135.50 in early trade but once again failed to do so. We slipped underneath 135.00, as equity futures wobbled. However, we have stayed sub this level even as equities turned higher.

- AUD/USD is up close to 0.50% to 0.6965, the best performer within the G10 FX space so far today. The currency market has shrugged off another sharp fall in iron ore prices. Higher China equities, buoyed by stimulus has helped, as has the sharp drop in USD/CNH, back to 6.6700 (-0.60% on the day).

- NZD/USD has broadly tracked AUD higher, but has underperformed by a small margin. We sit +0.30% higher, at 0.6335. The Performance of Services Index rose back to 11th month highs, printing 55.2 versus 52.2 in April.

- Other currencies are stronger against the USD, albeit to varying degrees. NOK is around 0.45% firmer, CAD 0.22%. GBP/USD is only modestly higher.

- A quick reminder that The U.S. will observe the Juneteenth holiday on Monday, which will result in closures/abbreviate trading hours for US markets.

- Note though we will still see St. Louis Fed President Bullard (’22 voter) comment on inflation and interest rates.

ASIA FX: Most USD/Asia Pairs Move Off Recent Highs

Most USD/Asia pairs have moved off their recent highs, led by the sharp drop in USD/CNH.

- CNH: USD/CNH has fallen sharply, down around 0.60% to the low 6.6700 region. The break of 6.7000 seemed to cause somewhat of an air pocket, as there were no major catalysts for the break lower. A Shanghai Securities article suggested 'extraordinary' stimulus measures are planned to combat a slowdown in investment, helped equity sentiment. Prospects of a tariff announcement from US President Biden also helped, although both of these news items were known prior to the break lower in USD/CNH.

- KRW: Spot USD/KRW climbed above 1295 briefly, fresh cyclical highs, as Korean equities tanked. The Kospi opened higher but subsequent slid more than 2.50%. USD/KRW came off its highs, as USD/CNH fell, while the South Korean Finance also warned against one-sided FX moves. Spot USD/KRW is back to 1290.

- INR: USD/INR is back below 78.00 for the first time in a number of sessions. We currently sit at 77.91. Indian bond yields have printed lower, as lower prices aid onshore sentiment. Brent crude remains around recent lows at $113/bbl.

- PHP: USD/PHP surged above 54.00 in early trade before running into resistance. We are back at 53.95 now. Comments from incoming BSP Governor Medalla around the BSP's gradualist approach to rate hikes and not having to follow the Fed in lockstep weighed on the peso. A 25bps hike is expected at this Thursday's BSP meeting.

- SGD: USD/SGD has slipped 0.35% to 1.3860, in line with broader USD weakness. The SGD NEER is sitting just off recent highs. This Thursday the focus will be on inflation data, particularly to gauge MAS tightening risks ahead of the October policy meeting.

- IDR: USD/IDR has remained around recent highs of just under 14840, in a quiet session overall. This Thursday the BI decision is due, with the market consensus expecting rates to remain at 3.50%, pressure is growing on the BI to act though, as real yields slip into negative territory and the yield differential with the US erodes. Also note, most of Indonesia's pandemic-era fiscal policy incentives ease at the end of this month.

EQUITIES: Mostly Lower In Asia; Hong Kong, China Outperform As Commodities Lag

Asia-Pac equity indices are mostly lower at typing following a mixed lead from Wall St. Commodity-linked equities region wide have borne the brunt of the selling pressure amidst broad weakness in major commodity benchmarks (BCOM: - 2.7%), with the MSCI Asia Pacific Index on track to decline for an eighth straight session.

- The CSI300 outperformed peers, trading 0.7% higher and operating a little below session highs at typing. The PBOC’s decision to hold the 1-year and 5-year LPRs steady came largely in line with expectations, with debate re: the possibility of further cuts later in ‘22 doing the rounds in Asia. Richly-valued consumer staples, tech (ChiNext: +2.4%), and healthcare stocks lead gains in the index, easily outpacing losses in energy and materials names amidst aforementioned weakness in commodity benchmarks.

- The Hang Seng Index sits 0.2% better off after reversing earlier losses on strength in real estate, seeing the Hang Seng Properties Index adding 3.5% at writing. China-based tech struggled, with the Hang Seng Tech Index sitting 0.5% weaker, weighed by a steep selloff in NetEase (-7.7%) after the company announced a delay to the Chinese launch of the closely-watched video game Diablo Immortal.

- A Reuters source report last Friday pointing to the PBOC accepting an application from the Ant Group to set up a financial holding company was rebutted by source reports to the contrary from China’s Yicai on Friday as well, effectively negating optimism spurred by the RTRS report (Alibaba’s U.S. ADRs gained as much as ~11% on the open of the NY session before paring most gains). The development thus provided virtually zero tailwind to the space on Monday, against prior expectations from some quarters.

- The ASX200 sits 0.5% worse off at writing, with losses in material stocks contributing the most drag to the index. Major miners such as Rio Tinto (-5.0%), Mineral Resources (-6.0%), and BHP Group (-4.1%) fell on the open amidst a well-documented sell-off in iron ore futures early on Monday, with iron ore on track for an eighth straight day of declines on worry re: China’s COVID-related economic outlook, and signs of weakness in the Chinese property market. The S&P/ASX All Technology Index deals 0.8% higher at writing by comparison, flipping above neutral levels on strength in index large-caps such as Block Inc and Xero Ltd.

- U.S. e-mini equity index futures are flat to 0.5% better off at typing, having pared gains from ~1.0% near the open.

GOLD: Holding On To Friday’s Lows; Fedspeak In Focus

Gold sits ~$4/oz weaker at typing to print $1,835/oz, having struggled to make headway above neutral levels in fairly limited Asia-Pac dealing. The precious metal operates a little above Friday’s worst levels, with U.S. Tsy futures and U.S. e-mini equity index futures noted to have unwound their earlier risk-positive moves despite an absence of meaningful macro headline flow.

- To recap Friday’s price action, gold snapped a two-day streak of gains, closing ~$18/oz lower amidst an uptick in U.S. real yields and the USD (DXY), ultimately capping a ~$32 overall lower close for the week.

- July FOMC dated OIS now price in an ~80% chance of a 75bp hike for that meeting, with a cumulative ~196bp of tightening priced in through the remaining four meetings for calendar ‘22. Relatively hawkish comments from the Fed’s Waller (voter) on Saturday supporting a 75bp move in July (flagging data-dependence) helped put a cap on gold, having emphasised tolerance for economic pain to bring down higher prices.

- Keeping within the U.S., debate re: stagflation continues to simmer, with the Fed’s Mester (voter) on Sunday pointing out that recession risks are rising, while Treasury Secretary Yellen said that she expects the economy to slow. A note that both officials were clear in stating that they currently do not predict an impending recession.

- Looking ahead (and keeping in mind the U.S. Juneteenth holiday on Monday), Fed Chair Powell will testify on semi-annual monetary policy before the Senate Banking Committee on Wednesday (1430 BST), with participants likely focusing on firmer clues towards a 50bp or 75bp hike for July.

- From a technical perspective, gold remains vulnerable following the ~$50/oz lower daily close seen on Jun 13. Focus is on a potential move lower towards support at $1,787.0/oz (May 16 low), a break of which would signal a resumption of the downtrend. On the other hand, key resistance holds at around $1,889.1/oz (trendline resistance from Mar 8 high).

OIL: Lower In Asia; Demand Outlook In Focus As Growth Worries Linger

WTI and Brent are ~$0.30 weaker apiece at typing, operating a little shy of their respective troughs made on Friday.

- To recap, both benchmarks lodged a lower weekly close (first in seven weeks for WTI, four for Brent) last Friday. Attention had coalesced around the possibility of slowing economic growth and weaker fuel demand, in a week that saw the Bank of England, Swiss National Bank, and the Fed raise rates, with the USD (DXY) briefly hitting a 20-year high as well.

- Looking to China, while daily COVID case counts and lockdowns around the country have generally continued easing, domestic fuel demand remains weak, with domestic refiners reportedly operating at around two-thirds capacity in the face of relatively strict export quotas as well (keeping in mind they are generally meant to serve domestic needs). Despite aforementioned improvements, worry re: further domestic COVID-related restrictions are continuing to linger however, with reports pointing to some neighbourhoods in the city of Shenzhen (~12.8mn pop) being placed under lockdown on Saturday amidst a limited number of reported cases.

- Average gasoline prices in the U.S. have registered their first weekly decline in nine weeks, dipping below the closely-watched $5/gallon mark in the process. U.S. Energy Secretary Granholm has however warned of a persistent “upward pull on demand” in light of the ongoing “summer driving season” and the tight supply outlook globally, driving debate re: the outlook for U.S. fuel demand.

- Libya’s crude production (amidst previously flagged, ongoing political woes) has risen to ~700K bpd, an improvement over the 100K - 150K bpd reported last Tuesday. Looking ahead, the country’s parliament-backed PM over the weekend stated that the country is unlikely to hold elections in ‘22, possibly troubling the crude production outlook for the rest of the year.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/06/2022 | 0100/0900 |  | CN | PBOC LPR announcement | |

| 20/06/2022 | 0600/0800 | ** |  | DE | PPI |

| 20/06/2022 | 0800/0900 |  | UK | BOE Haskel Opening TechUK Policy Leadership Conference | |

| 20/06/2022 | 0900/1100 | ** |  | EU | Construction Production |

| 20/06/2022 | 1300/1500 | | EU | ECB Lagarde Intro at European Parliament | |

| 20/06/2022 | 1300/1400 | | UK | BOE Cathy Mann Panels MNI Market News Connect Event | |

| 20/06/2022 | 1500/1700 | | EU | ECB Lagarde Intro as ESRB Chair at European Parliament | |

| 20/06/2022 | 1645/1245 |  | US | St. Louis Fed's James Bullard | |

| 20/06/2022 | 1700/1900 | | EU | ECB Panetta Interview with Federico Fubini at Nonfiction Festival | |

| 20/06/2022 | 1930/2130 | | EU | ECB Lane Speech at Society of Professional Economists |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.