Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

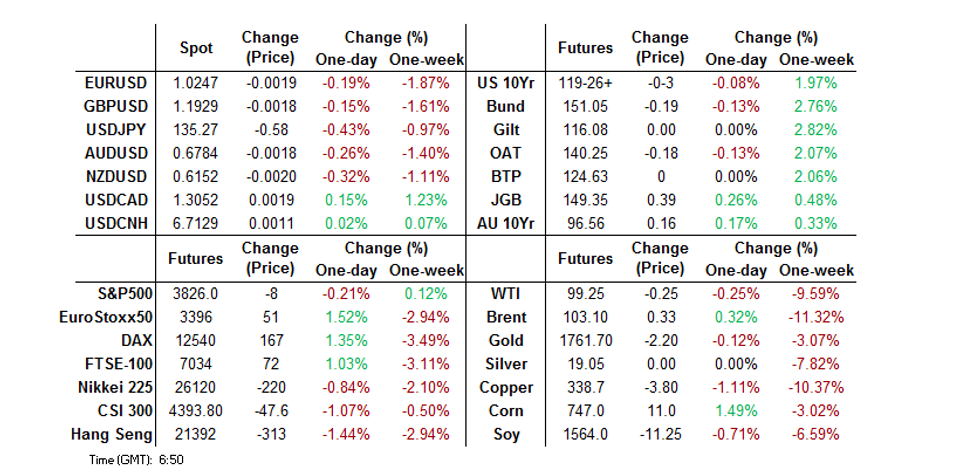

- Asia-Pac equities struggled on Tuesday's negative lead from European equities, although U.S. equities unwound Tuesday's early weakness into the bell.

- Oil was skittish as participants balanced the aforementioned recession worry with supply-related headlines

- Looking ahead, German factory orders are on tap and Eurozone retail sales will also print. In the US, the docket will be headlined by services ISM data and the release of the minutes from the most recent FOMC decision. We will also get weekly MBA mortgage apps, final services PMI data and the latest JOLTS job opening print. The release of the FOMC minutes from the June meeting will be bolstered by Fedspeak from NY Fed President Williams.

US TSYS: A Little Shy Of Tuesday’s Richest Levels

A fairly mundane round of Asia-Pac trade for Tsys saw weaker regional equity indices (on the back of recession fear & worry re: the COVID situation in China) and an early blip higher in oil after a heavy Tuesday session (with the bounce aided by Russian court rulings re: loading at one of its major ports) drawing most of the attention. The latter move moderated as we worked through overnight trade, likely aided by the former.

- TYU2 has stuck to a 0-07+ range on sub-standard volume of 75K, last dealing -0-04+ at 119-25, while cash Tsys run 2-3bp cheaper across the curve. Yields hold away from Tuesday’s lows after a late NY pullback which came alongside a recovery in U.S. equities post the European cash close (the S&P 500 finished +0.2% on Tuesday).

- There hasn’t been anything in the way of major macro news, nor meaningful market flow to flag since the Asia-Pac re-open, with the UK political situation dominating the headlines.

- Wednesday’s NY calendar is headlined by services ISM data and the release of the minutes from the most recent FOMC decision. We will also get weekly MBA mortgage apps, final services PMI data and the latest JOLTS job opening print. The release of the FOMC minutes from the June meeting will be bolstered by Fedspeak from NY Fed President Williams.

JGBS: Futures Unwind Early Blip Lower

JGB futures initially blipped lower at the Tokyo open, adjusting to Tuesday’s late pullback in U.S. Tsys, before recovering from worst levels and then breaching the recent session highs. That leaves JGB futures running +45 ahead of the bell. Note that Tuesday’s cautious tone has weighed on Asia-Pac equities, which likely provided some background support for JGBs. Cash JGBs run little changed to 3.5bp richer across the curve as a result, with 7s leading on the back of the bid in futures. Note that payside flows have shown up again in super-long JGBs, resulting in the widening of super-long swap spreads from both sides as JGBs richen.

- Local news flow was light, with continued discussions surrounding the restart of the government-subsidised local travel scheme evident, although there was nothing in the way of firm details forthcoming.

- BoJ Rinban operations covering 1- to 5- & 10- to 25-Year JGBs had no meaningful impact on the market.

- 30-Year JGB supply headlines domestic matters on Thursday.

AUSSIE BONDS: Richer, But Off Overnight Highs

A lack of notable macro headline flow and tier 1 data releases meant that Aussie bonds didn’t have much to latch onto during Sydney trade, with cash ACGBs running 4.5bp to 15.0bp richer across the curve, bull flattening, as participants adjusted to the latest round of recessionary worry coming out of Europe. YM and XM are +8.0 and +14.5, respectively, sticking to the ranges established during overnight dealing. Bills run flat to 8 ticks richer through the reds, bull flattening.

- The latest round of ACGB Apr-33 supply went smoothly, with the weighted average yield pricing 0.97bp through prevailing mids (per Yieldbroker), as the cover ratio printed at 2.38x, above the 2.00x mark (although a decline from the prev. 3.11x, with the caveat that the prior auction was in Feb, when a different market regime was in place). Wider caution re: the deployment of capital into ACGBs and a lack of outright relative value in the wider sector likely limited broader participation in the auction.

- Thursday will see monthly trade balance data headline the domestic docket.

FOREX: Outside Of USD/JPY, USD Firmer

Outside of the yen, the USD has been supported against the majors, although ranges have been tight.

- Yen demand was evident early in the session against both the USD and on crosses. USD/JPY dipped below the overnight low, before finding a base between 135.10/15. We last sat at 135.40 and may have seen a sharper pull back in USD/JPY if not for a modest recovery in US yields (2yr up 2bps to 2.84%).

- EUR/JPY dipped just below 138.70, through overnight lows and the 50-Day MA, which comes in at 139.01. The pair last traded at 138.85. EUR/USD has drifted towards 1.0250 this afternoon.

- AUD and NZD have struggled to gain much upside traction, although more so NZD. AUD/USD has oscillated around 0.6800. Weaker commodity prices have curbed any upside impetus. Iron ore is back to a $107/tonne handle. Lockdown concerns in China has weighed on the outlook, with large parts of Shanghai undergoing mass testing as case numbers track higher.

- Copper is also down, off a further -1%, while oil gains have slipped as the session has progressed. Brent back sub $104/bbl, from earlier highs of close to $106/bbl.

- CAD and NOK are back weaker against the USD, although only modestly.

- GBP/USD got above 1.1970 in early trade, but is now back to 1.1950. Local politics is likely to be watched closely when the London session kicks off.

- Looking ahead, German factor orders are on tap, along with the construction PMI. The UK construction PMI is also due. Retail sales for Euro Area also print.

- In the US, the docket will be headlined by services ISM data and the release of the minutes from the most recent FOMC decision. We will also get weekly MBA mortgage apps, final services PMI data and the latest JOLTS job opening print. The release of the FOMC minutes from the June meeting will be bolstered by Fedspeak from NY Fed President Williams.

FX OPTIONS: Expiries for Jul06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2030(E530mln)

- USD/JPY: Y135.00($615mln)

- NZD/USD: $0.6410(N$1.2bln)

- USD/CAD: C1.2610-25($2.0bln), C$1.3200-10($595mln)

ASIA FX: CNH Outperformance Persists

Most USD/Asia pairs continue to trend higher on recessionary fears and weaker regional equity market sentiment. A number of pairs have printed fresh cyclical highs. CNH outperformance continues though, with the currency shrugging off renewed onshore Covid concerns.

- CNH: USD/CNH has tracked familiar ranges, between 6.7060 and close to 6.7200. Onshore equities are off by more than 1%, as lockdown fears re-emerge on rising case numbers in Shanghai. The city will conduct mass testing, while restrictions on entertainment facilities have been tightened. Still, CNH outperforming the broader Asian FX complex.

- KRW: USD/KRW spiked above 1310 at the open, but settled back at 1305/1310 range after that. We remain below the overnight high of 1315 for the 1 month NDF. Onshore equities are down more than 1.5%, with offshore investors unloading $266.3mn in local equities, nearly offsetting all of yesterday's net inflow.

- INR: USD/INR, is down slightly, back to 79.30 after closing yesterday at 79.36. Still, the 1 month NDF has pushed back above 79.50. Onshore equities are higher, while bond yields are lower (10yr back to 7.32%, -7bps so far). The sharp drop in oil prices is aiding sentiment in this space. We are now comfortably below the mid June highs above 7.60% for the 10yr.

- IDR: USD/IDR spot has pushed through 15000, +30figs on the day to 10518. Some selling interest emerged after the BI Governor stated the central bank continues to stabilize the rupiah. BI remains comfortable with the level of inflation and already started to adjust policy through liquidity operations the Governor stated.

- THB: USD/THB has pushed above 36.00, +0.55% on yesterday's closing levels. A BoT Assistant Governor appeared less hawkish compared to recent BoT rhetoric, still it is a little over a month out from the next BoT meeting so we are likely to hear more on the outlook before then.

- MYR: USD/MYR has gotten close to previous YTD highs, before edging back down to 4.4240. Lower oil prices are weighing, while the other focus point is the upcoming BNM decision due later today. The market expects another 25bps hike, see our full preview here for more details.

EQUITIES: Lower In Asia On Recession Worry; COVID Worry Looms (Again) In China

Asia-Pac equity indices are mostly lower at typing, with a mixed lead from Wall St. providing little guidance. Recession worry was evident throughout the session, with several commodity benchmarks broadly extending Tuesday’s losses over fears of economic slowdowns crimping demand.

- The Hang Seng leads losses, sitting 1.4% worse off on losses in >80% of its constituents. Broader sentiment has suffered as Shanghai carries out mass testing in 12 of the city’s 16 districts, unwinding some optimism re: economic recovery, seeing the Hang Seng give up virtually all gains made over the past week.

- The Chinese CSI300 deals 1.3% weaker at typing, on track for its largest decline in a week on weakness in nine of ten sub-indices, with richly-valued consumer staples and healthcare stocks bearing the brunt of the selling over previously-flagged COVID fears. The materials (-2.4%)and energy (-4.8%) sub-indices were softer as well, reflecting declines in major commodity benchmarks.

- The Nikkei 225 trades 1.1% lower, with the broader TOPIX index sitting 1.4% worse off at typing. ~85% of the Nikkei’s constituents are in the red, with the latest bout of JPY strength catalysing weakness in major exporters and large-cap names.

- The ASX200 fell to a lesser extent than regional peers, dealing 0.4% weaker at writing. Outperformance in the tech sub-index (+3.0%) was countered by a sharp decline in the materials sub-gauge (-4.6%), with the likes of Rio Tinto Ltd (-6.4%) and Mineral Resources Ltd (-5.3%) leading the way lower.

- U.S. e-mini equity index futures sit on either side of neutral levels at typing, having whipped between gains and losses throughout Asia-Pac dealing.

GOLD: Firmer In Asia

Gold sits ~$6/oz firmer at typing to print ~$1,771/oz, a shade below session highs, but extending a move away from six-month lows made on Tuesday (at ~$1,764/oz).

- To recap, the precious metal shed ~$40/oz around Tuesday’s NY session open after keeping above $1,800/oz for much of the Asian session, ultimately closing ~$45/oz lower on the day. The move lower was facilitated by a broad recovery across U.S. real yields and a rally in the USD, with the DXY hitting levels not witnessed since Dec ‘02 (above 106.00) on the back of growth fears in Europe, supporting a diverging policy outlook.

- July FOMC dated OIS now price in ~70bp of tightening for that meeting while a cumulative ~168bp is now priced in through calendar ‘22. The latter has continued to edge lower, reflecting ongoing debate re: less aggressive rate hikes amidst economic growth risks, with BBG Economics forecasting odds for a recession in the U.S. in ‘23 at 38%.

- A note that Fedspeak across the past month has pointed to a Fed prepared to weather hits to economic growth to fight inflation, with Fed Chair Powell last week saying that the process is “highly likely to involve some pain”.

- From a technical perspective, conditions remain bearish for gold. Key support at $1,780.4/oz (Jan 28 low) has been broken, exposing support at $1,753.1/oz (Dec 15 ‘21 low), while a break of that level will bring further support at $1,721.7/oz (Sep 29 ‘21 low) into focus.

OIL: Back From Best Levels; Shanghai COVID Outbreak Eyed

WTI is ~+$0.10 and Brent is ~+$0.70, with WTI trading a little below $100 at typing. Both benchmarks pared earlier gains of as much as ~$2.60 to $3.00, seeming to catch a bid on news re: a court order to halt oil loadings at a Caspian Pipeline Consortium (CPC) port on the Black Sea, potentially affecting ~1.9mn bpd in Kazakh crude exports.

- To recap Tuesday’s price action, both benchmarks closed ~$10 weaker, moving sharply lower amidst growing recession fears in both the U.S. and Europe, fuelling worry re: demand destruction.

- Goldman analysts have since stated that Tuesday’s move may be overdone, worsened by limited liquidity and technicals, highlighting persistent, fundamental supply tightness in crude markets.

- Developments out of China may have applied pressure to crude in Asia, as lockdown fears have again surfaced. Shanghai on Tuesday re-imposed mass testing regimes (in line with their well-documented zero COVID policy) in 12 of the city’s 16 districts, with tests due to be completed by Thursday. Total daily case counts and cases outside of quarantine (two reported for Wednesday morning) in Shanghai have ticked higher, with the latter being a crucial metric for authorities re: pandemic monitoring.

- Elsewhere, indirect Iran-U.S. nuclear talks have seen virtually zero progress, with the State Dept.’s Price saying that no other talks are scheduled at present.

- A short-lived strike in Norway’s O&G sector ended less than a day after it commenced after intervention from the Norwegian gov’t, with the move averting an estimated >300K bpd decline in crude production.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 06/07/2022 | 0600/0800 | ** |  | DE | Manufacturing Orders |

| 06/07/2022 | 0600/0800 | ** |  | SE | Private Sector Production |

| 06/07/2022 | 0730/0930 | ** |  | EU | IHS Markit Final Eurozone Construction PMI |

| 06/07/2022 | 0800/1000 | ** |  | ES | Industrial Production |

| 06/07/2022 | 0810/0910 |  | UK | BOE Pill Speaks at Qatar Centre Conference | |

| 06/07/2022 | 0830/0930 | ** | | UK | IHS Markit/CIPS Construction PMI |

| 06/07/2022 | 0900/1100 | ** | | EU | retail sales |

| 06/07/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 06/07/2022 | 1230/1330 | | UK | BOE Cunliffe Panels Qatar Centre Conference | |

| 06/07/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 06/07/2022 | 1300/0900 | | US | New York Fed President John Williams | |

| 06/07/2022 | 1345/0945 | *** | | US | IHS Markit Services Index (final) |

| 06/07/2022 | 1400/1000 | *** | | US | ISM Non-Manufacturing Index |

| 06/07/2022 | 1400/1000 | ** | | US | JOLTS jobs opening level |

| 06/07/2022 | 1400/1000 | ** | | US | JOLTS quits Rate |

| 06/07/2022 | 1800/1400 | | US | FOMC Minutes |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.