Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- US CONGRESS APPROVES DEBT-LIMIT SUSPENSION, AVERTING DEFAULT - RTRS

- BOJ’s UEDA: NO SET TIME FRAME FOR HITTING 2% INFLATION TARGET - RTRS

- PANETTA: INFLATION TOO HIGH, BUT THERE IS NO REASON TO WORRY - LE MONDE

- AUSSIE MINIMUM WAGE LIFT SPARKS RBA RATE CONCERNS - MNI BRIEF

- EARLY OCR CUT ON RISING BANK COSTS- EX- RBNZ - MNI

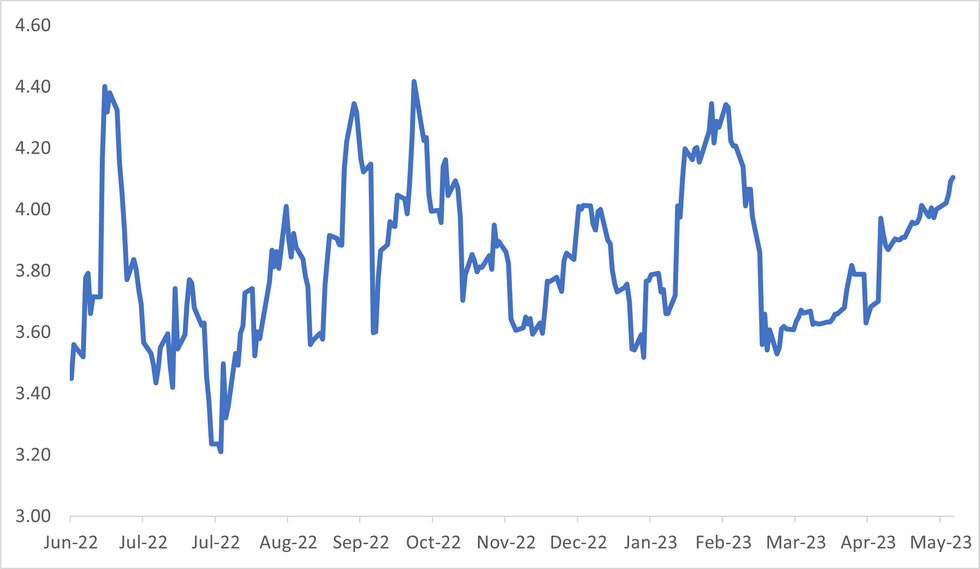

Fig. 1: RBA- Dated OIS - Terminal Rate Expectations

Source: MNI - Market News/Bloomberg

U.K.

MERGERS: EQT AB is nearing an agreement to acquire veterinary drugmaker Dechra Pharmaceuticals Plc in what would be one of the largest UK take-private deals this year, according to people familiar with the matter. The Swedish buyout firm and the UK company are likely to announce a deal Friday ahead of an already extended deadline to make a firm offer or walk away, said the people, who asked not to be identified because discussions are private. (BBG)

HOUSING: The UK housing market is sputtering again, with economists predicting the downturn has further to run as rising interest rates bite into the budgets of consumers. The warning came after reports Thursday showed house prices resumed their decline last month and mortgage approvals unexpectedly fell in April. Households repaid mortgage debt at an historic pace. (BBG)

EUROPE

ECB: ECB's Fabio Panetta: 'I don’t think this is the time to be too hasty in raising interest rates'. In an interview with 'Le Monde', Fabio Panetta, a member of the European Central Bank's Executive Board, indicates that with inflation slightly easing within the eurozone, the ECB's tightening monetary policy will likely be put on hold in the not-too-distant future. (Le Monde)

U.S.

DEBT: The U.S. Senate on Thursday passed bipartisan legislation backed by President Joe Biden that lifts the government's $31.4 trillion debt ceiling, averting what would have been a first-ever default. The Senate voted 63-36 to approve the bill that was passed on Wednesday by the House of Representatives, as lawmakers raced against the clock following months of partisan bickering between Democrats and Republicans. (RTRS)

CREDIT RATING: The suspension of US debt limit until Jan. 2025 means there will not be a binding constraint on government borrowing “for some time,” Moody’s says in a statement. Debt-limit deal struck by US lawmakers “in line with our expectation” that Congress would continue to raise or suspend the debt limit, Moody’s Senior Vice President William Foster says in statement. (BBG)

GEOPOLITICS: JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon is planning to visit Taiwan after wrapping up his high-profile trip to China, navigating a politically sensitive region at a time of heightened tensions between Beijing and Washington. (BBG)

OTHER

JAPAN: Bank of Japan Governor Kazuo Ueda said on Friday the central bank did not have a set time frame for achieving its 2% inflation target but that it would strive to hit it at the earliest date possible. (RTRS)

JAPAN: The functioning of Japan’s bond markets improved amid receding speculation about early tweak of yield-curve control by the Bank of Japan, and wagers the Fed may pause on its rate tightening. The BOJ’s diffusion index, which is based on a survey of 70 respondents on bid-ask spreads and trading volumes, rose to minus 46% points, compared with minus 64% points three months ago, which was the worst on the bank’s data going back February 2015. (BBG)

AUSTRALIA: Australia’s central bank will probably raise interest rates three more times in coming months to counter persistently elevated inflation driven by surging services prices, according to two economists. (BBG)

AUSTRALIA: (MNI) Sydney - The Fair Work Commission has raised Australia’s minimum wage by 5.75%, lifting the pay of 0.7% of the country’s workforce and potentially affecting about 20.5% of all Australian employees via the award system, a move that could impact the Reserve Bank of Australia’s upcoming June 6 interest rate decision. (MNI)

NEW ZEALAND: (MNI) Sydney - The cost of funding for New Zealand’s banks will increase as a key Reserve Bank of New Zealand support facility winds down, increasing interest and deposit rates, slowing the economy and potentially prompting an earlier-than-forecasted cut to the Official Cash Rate, John McDermott, executive director at Motu Economic and Public Policy Research, told MNI. (MNI)

SOUTH KOREA: South Korean exports are showing some signs of a recovery on the back of rising demand from China and increasing outbound shipments of semiconductors, the finance minister said Friday. (Korea Herald)

CHINA

US/CHINA: Asian leaders accustomed to straddling the US-China divide are increasingly nervous that tensions between the world’s two superpowers could spiral toward conflict, with a series of decisions on both sides making it harder for Beijing and Washington to find common ground. A defense conference in Singapore this week that could have served as a bridge between the two sides looks instead like it will further highlight the rift over issues including Taiwan, restrictions on high-end chips and China’s claims to a large swath of the South China Sea. (BBG)

YUAN: Official data from CFETS shows daily turnover of USD/CNY spot trading onshore at $59 billion on Wednesday — the highest since 2018 and also the second highest in history, according to traders. Previous record high of the daily volume was $66b back in Oct. 2018, they said. (BBG)

ECONOMY: China’s courier deliveries reached 50b parcels by May 31 this year, Securities Daily reports Friday. That’s 155 days earlier than the same milestone hit in 2019, and 27 days earlier than 2022 Data points to economic vitality, State Post Bureau told the paper, adding courier industry has played important role in driving economic growth against backdrop of China’s policies to boost domestic consumption. (CSJ)

HOUSING: Further housing support will stabilise the wider economic rebound, according to Wu Chaoming, vice president at the Financial Information Research Institute. Wu expects buyers to increase annual sales this year, but the sector’s overall recovery will remain tepid. Leaders in Beijing should implement policies to stabilise land and house prices in a timely manner, as the real-estate recovery is important to the wider rebound. On other topics, Wu said industrial production will remain soft in the coming months, with private investment sluggish and a slowdown in exports. (21st Century Herald)

MARKETS: China will expand the scope of its futures market to provide foreign investors more hedging tools and diversified investment options, according to Fang Xinghai, vice chairman at the China Securities Regulatory Commission (CSRC). In a recent speech, Fang said Chinese firms will be supported to issue depositary receipts in the European market. China remains committed to high-quality institutional opening up of the capital market and will optimise the connect programs between the mainland and Hong Kong. (Yicai)

HOUSING: Authorities should make efforts to boost demand in the real-estate sector, following last year's focus on the supply side, according to Yao Jingyuan, researcher at the Counsellor Office of the State Council. Yao said at a recent conference China’s economy faced insufficient demand with real estate being a major drag on growth prospects. Wei Chenyang, secretary-general at the Wudaokou Global Real Estate Finance Forum, said the Government should expand the use of REITs to revitalise stock valuations and increase liquidity. (21st Century Herald)

CHINA MARKETS

PBOC Net Drains CNY3 Bln Via OMOs Friday

The People's Bank of China (PBOC) conducted CNY2 billion via 7-day reverse repos on Friday, with the rates unchanged at 2.00%. The operation has led to a net drain of CNY3 billion after offsetting the maturity of CNY5 billion reverse repo today, according to Wind Information.

- The operation aims to keep banking system liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.9868% at 09:31 am local time from the close of 1.8343% on Thursday.

- The CFETS-NEX money-market sentiment index closed at 44 on Thursday, compared with the close of 47 on Wednesday.

PBOC SETS YUAN CENTRAL PARITY RATE AT 7.0939 FRI VS 7.0965 THURS

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.0939 on Friday, compared with 7.0965 set on Thursday.

OVERNIGHT DATA

NZ Q1 VOLUME OF ALL BUILDINGS Q/Q 0.6%; MEDIAN -2.0%; PRIOR -0.8%

NZ Q1 TERMS OF TRADE Q/Q -1.5%; MEDIAN; PRIOR 1.5%

SOUTH KOREA Q1 P GDP Y/Y 0.9%; MEDIAN 0.8%; PRIOR 0.8%

SOUTH KOREA Q1 P GDP Q/Q 0.3%; MEDIAN 0.3%; PRIOR 0.3%

SOUTH KOREA MAY CPI M/M 0.3%; MEDIAN 0.3%; PRIOR 0.2%

SOUTH KOREA MAY CPI Y/Y 3.3%; MEDIAN 3.4%; PRIOR 3.7%

SOUTH KOREA MAY CORE CPI Y/Y 4.3%; PRIOR 0.2%

JAPAN MAY MONETARY BASE Y/Y -1.1%; PRIOR -1.7%

AU APR HOME LOANS VALUE M/M -2.9%; MEDIAN 2.0%; PRIOR 5.3%

AU APR INVESTOR HOME LOANS M/M -0.9%; PRIOR 3.4%

AU APR OWNER-OCCUPIER HOME LOANS M/M -3.8%; PRIOR 6.3%

MARKETS

US TSYS: Weaker, Debt Ceiling Bill Passes The Senate, Awaiting Non-Farm Payrolls

TYU3 is currently trading at 114-20+, -3 from NY closing levels after the US Senate passed the US debt-ceiling bill, by 63-36 votes. The legislation now goes to US President Biden to be signed into law, which the White House has stated will happen as soon as possible. Biden will address the American people tomorrow.

- The Senate voted on 11 proposed amendments, but none were adopted. Senate Leader Schumer stated earlier on Thursday that approving any of the amendments would require the bill to go back to the House, which would almost certainly lead to default.

- Cash tsys are 0.6-1.8bp cheaper across benchmarks in Asia-Pac trade ahead of May Non-Farm Payrolls later today. BBG consensus expects an increase of 195k after +253k in April with the unemployment rate expected to rise to 3.5% from 3.4%.

- There are no major data releases in Europe today.

JGBS: Richer, Mid-Range, Light Local Calendar, Awaits US Non-Farm Payrolls

JGB futures are sitting in the middle of the Tokyo session range at 148.83, +9 versus settlement levels.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined comments by BoJ Governor Ueda in parliament re: not being able to say when the BOJ will achieve its 2% price goal.

- Consequently, local participants were likely closely monitoring headlines and keeping an eye on US Treasury yields leading up to the release of the US Non-Farm Payrolls data later today.

- In line with this, cash tsys are trading 0.6-2.0bp cheaper in Asia-Pac trade after the US Senate passed the US debt-ceiling bill, by 63-36 votes. The legislation now goes to US President Biden to be signed into law, which the White House has stated will happen as soon as possible.

- The cash JGBs are richer across the curve, apart from the 40-year zone, which is 0.5bp cheaper. The benchmark 10-year sees its yield 0.7bp lower at 0.417%, below the BoJ's YCC limit of 0.50%. The 2-3-year zone is the outperformer with yields 1.0-1.3bp lower despite this morning’s BoJ operations seeing a higher spread and a slightly higher offer cover ratio for the 1-3-year bucket.

- Swap rates are however lower across the curve with swap spreads narrower.

- The local calendar sees Jibun Bank PMIs (May F) on Monday.

AUSSIE BONDS: Weaker, At Session Cheaps, Awaits US Payrolls

ACGBs sit weaker (YM -7.0 & XM -3.0), near Sydney session cheaps as local participants focus on the possible implications of the Australian Fair Work Commission’s decision to lift the minimum wage by 5.75%.

- Cash ACGBs are 2-7bp cheaper with the 3/10 curve 5bp flatter and the AU-US 10-year yield differential +7bp at +3bp.

- Swap rates are 3-6bp higher.

- The bills strip bear flattens with pricing is -9 to -4.

- The local calendar is heavy next with the focal point likely to be RBA Policy Decision on Tuesday. BBG consensus is expecting a no-change outcome although it is not unanimous.

- While not expecting a hike until August, ANZ today announced an increase in its terminal cash rate forecast to 4.35% from 4.10% (link). They join several other sell-side economists who have turned more hawkish in terms of the RBA outlook (link).

- RBA dated OIS is 4-10bp firmer across meetings with a 56% chance of a 25bp hike in June priced. It was a 40% chance at the opening of trade today.

- On Monday, the local calendar is scheduled to release Judo Bank PMIs (May F), MI Inflation Gauge (May), Inventories (Q1), Company Profits (Q1) and ANZ Job Ads (May).

- The AOFM announced plans to sell A$700mn of the 3.75% 21 May 2034 bond on Wednesday.

NZGBS: Richer, Off Bests, Pressured By US Tsys & ACGBs

NZGBs closed flat to 1bp cheaper, well off the local session’s best levels despite NZ trade data adding to signs the economy may have been in a recession. The economy shrank 0.6% q/q in the final three months of 2022.

- Import volumes jumped 6.7% q/q, the most in two years in Q1, while export shipments increased just 1% q/q. However, construction work, another input in Q1 GDP calculations, rose 0.6% q/q (estimate -2.0%) in 1Q.

- The decline in NZGBs during the session seemed to be driven by the overall weakness in bonds during Asia-Pac trading. This weakness was particularly evident in ACGBs, which were influenced by economists adopting a more hawkish stance ahead of the RBA decision next Tuesday. Additionally, the announcement of a minimum wage increase of 5.75% by the Australian Fair Work Commission also contributed to the bond market reaction.

- NZ/US 10-year yield differential closes +6bp at +71bp, with the NZ/AU differential unchanged at +68bp.

- Swap rates closed flat with the 2s10s unchanged.

- RBNZ dated OIS closed little changed.

- The local calendar is light next week with ANZ Commodity Prices (Tue) and Mfg Activity (Wed) as the only releases. The NZ Government is also scheduled to release its 10-month Financial Statement on Wednesday.

EQUITIES: Hang Seng Tech & HS China Enterprises Index Rebound +4%

Asian stocks are tracking higher in the first part of Friday's dealings. Much of the focus remains on gains for Hong Kong stocks, the HSI up over 3.6% at the break. The tech sub index is tracking more than 5% higher. The HS China Enterprise index is +4.2%.

- China mainland shares are also firmer, albeit with a lower beta, the CSI 300 +1.3% at the break. Japan stocks are +1.3% for the Topix. Taiex +1.4%, the Kospi +1.0%, while SEA markets are more muted.

- In terms of drivers of these moves, there doesn't appear to be a single catalyst. As we noted earlier the Golden Dragon rallied 4% in US trade on Thursday, so some positive spillover is clearly evident. This was amidst broadly positive gains in US/EU bourses, with the viewpoint of a Fed pause in June helping sentiment.

- Goldman Sachs is keeping its MSCI China OW but lowering the price target, is another positive. Value buyers may also be emerging given the extent of recent sell-offs (i.e the HSI and HS China Enterprise Index both moving 20% off Jan highs).

- Possible stimulus expectations could also be driving market sentiment, it the aftermath of this week's mixed PMI data.

- We have seen some positive spillover to US equity futures, Eminis last close to +0.20% (4235/36), while Nasdaq futures are +0.25%. The US Senate passed the debt-ceiling agreement, which is expected to be signed by President Biden. This didn't bring any meaningful shift in equity sentiment though.

FOREX: USD Lower, A$ Rallies On RBA Expectations/Minimum Wage Hike

The BBDXY is tracking lower, last close to 1236.40, -0.15% lower versus NY closing levels. The dollar has seen broad based losses, with the index down through Thursday lows. AUD and NZD have outperformed, with the A$ slightly stronger at the margins. Risk appetite has been much stronger in HK/China equities, which has also weighed on USD sentiment.

- AUD/USD is back to 0.6615, +0.65% above NY closing levels. Sell-side names adding RBA rate hikes before and after the 5.75% minimum/wage hike that was announced this morning. This has been a clear support point (see this link). Pricing is slightly above 55% for a 25bps hike next week.

- AUD/NZD firmed in the first part of trade, getting to fresh highs of 1.0866, but we now back at 1.0835/40, as the firmer risk backdrop has seen NZD/USD play catch up. NZD/USD is back above the 0.6100 handle this afternoon.

- The US Senate passed the debt-ceiling legislation. The market impact was minimal. US yields have ticked higher, the 10yr back above 3.61%, (~+2bps). but this hasn't aided USD sentiment.

- USD/JPY sits slightly below NY closing levels, last 138.70/75. Yen has lagged the antipodeans though. BoJ Governor Ueda appeared before parliament, stating that the central bank didn't have a set time frame for achieving to the 2% inflation target.

- Looking ahead, all focus is on the NFP release where Bloomberg consensus looks for further moderation in payrolls growth in May to +195k versus a prior read of +253k.

OIL: Brent Builds On Thursday Gains, But Still Tracking Lower For The Week

Brent crude has drifted higher in the first part of Friday trade. We were last at $74.70/75/bbl, which is 0.60% above Thursday closing levels. This comes after Thursday's 2.23% gain, amid broadly stronger risk appetite in the equity space and a weaker USD. Still, we are tracking lower for the week, off nearly 3% at this stage. WTI is back to $70.50/bbl, following a similar trajectory.

- For Brent, recent lows come in near $71.40/bbl, while on the topside, the simple 50-day MA sits close to $78.85/bbl.

- Crude’s gains come ahead of this weekend's OPEC+ meeting which many analysts thought would lean more heavily towards extending cuts if Brent goes sub-$70/bbl this week – a move now looking less likely.

- EIA weekly data showed a 4.5mn bbl increase in crude stocks – which were supported by a net 1mn bbl increase in imports. Gasoline stocks saw a small decline while implied demand on a four-week average reached 9.2mn bpd - the highest four-week average since late 2021 and on a seasonal basis since 2019. This still points to a challening supply backdrop for oil bulls.

GOLD: Higher For Three Consecutive Days

Gold is 0.3% higher in the Asia-Pac session, after closing higher for the third day in a row at 1977.61 (+0.8%).

- The bipartisan agreement, which aims to suspend the debt limit until Jan. 1, 2025, has been approved by the House and the Senate and now goes to US President Biden to be signed into law. This eliminates a significant risk to financial markets that had provided support to gold in early May.

- ADP private employment data exceeded expectations, aligning with the strength seen in the JOLTs data on Wednesday. This initially fueled speculation that the Federal Reserve may need to take further measures to cool down the labour market and control inflation. However, subsequent comments from central bank officials and weaker-than-expected unit labour costs data eased concerns of an imminent interest rate hike, which provided support to non-yielding gold.

- Attention now turns to May Non-Farm Payrolls later today. BBG consensus expects an increase of 195k after +253k in April with the unemployment rate expected to rise to 3.5% from 3.4%.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 02/06/2023 | 0645/0845 | * |  | FR | Industrial Production |

| 02/06/2023 | 1230/0830 | *** |  | US | Employment Report |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.