Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- BOJ ON HOLD; MAKES 10 YEAR RATE MOVES MORE FLEXIBLE - MNI

- LAGARDE OFFERS DOWNBEAT ASSESSMENT AS ECB RAISES RATES - BBG

- US BAN HONG KONG CHIEF EXECUTIVE LEE FROM ECONOMIC SUMMIT - BBG

- DONALD TRUMP HIT WITH NEW OBSTRUCTION CHARGES - BBG

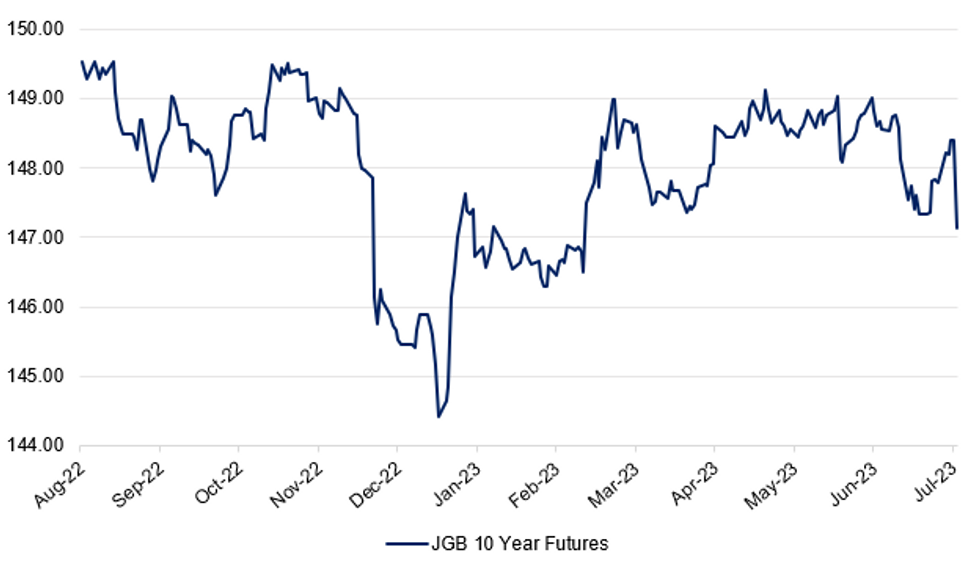

Fig. 1: JGB 10 Year Future

Source: MNI - Market News/Bloomberg

U.K.

HOME PRICES: Home sellers are increasingly offering price cuts to tempt cash-strapped Britons into deals, raising the likelihood of a further drop in house prices this year. Sellers’ willingness to compromise comes as the number of would-be buyers contacting agents about purchasing a home tumbled by almost a fifth in the past two months, according to a report from property portal Zoopla. (BBG)

EUROPE

ECB: Christine Lagarde is confronting how tighter monetary policy is driving the euro-zone economy into the ground in her bid to bring inflation under control. The European Central Bank president on Thursday offered a downbeat assessment of a “deteriorated” economic outlook as she delivered a ninth consecutive interest-rate increase and said that the Governing Council is open minded on another potential hike in September. (BBG)

ECB: The European Central Bank will stop paying banks for the money they are required to keep at the institution as a minimum reserve, a surprise move that could cut billions from lenders’ interest income. Europe’s banks most recently were required to stash about 165 billion euros at the ECB as minimum reserves, according to data through June 20 on the central bank’s website. The central bank paid 3.25% on that amount, translating into annual income of about 5.4 billion euros ($6 billion). (BBG)

ITALY: Italian Prime Minister Giorgia Meloni said US President Joe Biden fully trusts the country’s plan to establish balanced relations with China, as Italy mulls a strategy to disentangle from a controversial investment pact known as China’s Belt and Road Initiative. (BBG)

ITALY: Italy will ask the European Union to extend the financing deadline for about €15.9 billion ($17.4 billion) of projects that had originally been included in its post-pandemic recovery fund spending plan after the government struggled to spend all of it in time. (BBG)

UKRAINE: Ukraine’s long-awaited assault against Russian troops in the occupied south kicks off a new stage in the war as Kyiv seeks to persuade its allies that it can take back lost territory. With Moscow also stepping up a long-range missile campaign, both sides are intensifying their attacks as Kyiv seeks a decisive breakthrough on the ground and Russia aims to cripple Ukraine’s economy. (BBG)

U.S.

POLITICS: Donald Trump was hit with new obstruction charges in the criminal case over his handling of classified documents, including allegations that he and two employees attempted to delete surveillance video footage at his Mar-a-Lago estate last year. In the latest indictment announced on Thursday, prosecutors accused Trump of directing employees to erase footage of a storage room where the documents were kept, days after his lawyers received a subpoena for any such recordings. (BBG)

US/HONG KONG: The White House will bar Hong Kong Chief Executive John Lee from attending a major economic summit in the US this fall, the Washington Post reported, citing three unidentified US officials familiar with the matter. The US is set to host the Asia-Pacific Economic Cooperation in November. Lee and other top Hong Kong and mainland Chinese officials were sanctioned by the US for their role in the crackdown on civil liberties in the city. Generally, US people or entities are banned from engaging with individuals on the list, unless an exemption is awarded. (BBG)

REAL ESTATE: Office buildings are poised to set records for a bad reason this year: The amount of office space in the US is declining for what is likely the first time in history. A lack of new construction and a plethora of aging office space being repurposed or destroyed will lower the amount of office space, according to Jones Lang LaSalle Inc. Less than 5 million square feet (465,000 square meters) of new offices broke ground in the US so far this year, while 14.7 million square feet has been removed, often to be converted into buildings for other uses. (BBG)

OTHER

BOJ: The Bank of Japan board on Friday decided to increase the flexibility of the 10-year long-term policy interest rate, but kept yield curve control without changing both the short- and long-term policy interest rate targets, a statement released by the BOJ said on Friday. (MNI)

BOJ: The Bank of Japan jolted financial markets by loosening its grip on bond yields in Governor Kazuo Ueda’s first surprise move since taking the helm, a step that will likely spur talk of potential policy normalization to come. The yen whipsawed, falling more than 1% before reversing losses to trade about the same amount higher. Japan’s benchmark bond yield surged, extending gains above the central bank’s 0.5% cap. (BBG)

RBA: Impending reforms at the Reserve Bank of Australia to alter its mandate and interaction with financial regulators open the way to the use of macroprudential measures to address financial imbalances more directly than with the blunt tools of interest-rate policy, industry experts and ex-staffers told MNI. (MNI)

SAUDI ARABIA: Saudi Arabia has made the first big deal in a push to deploy its vast wealth into the global mining industry, agreeing to buy a stake in Vale SA’s base metals unit. Saudi sovereign wealth vehicle, Public Investment Fund, and Saudi Arabian Mining Co., known as Maaden, will purchase a 10% stake in a company created to house Vale’s base metal assets, Vale said Thursday. Separately, investment firm Engine No. 1 will buy a 3% stake. The total amount to be paid under both agreements is $3.4 billion. (BBG)

ADANI: Billionaire Gautam Adani’s conglomerate is returning to the loan market to potentially raise more than $1 billion, the latest sign it’s slowly regaining the ability to raise funds six months after a US short seller caused a meltdown in its stocks and bonds. (BBG)

TSMC: The world’s largest contract-chipmaker is investing in research for chipmaking techniques more advanced than next-generation 2nm or 3nm nodes, Chairman Mark Liu says at an event in Hsinchu. (BBG)

TURKEY: Turkish President Recep Tayyip Erdogan appointed three new deputy governors to the central bank, continuing his revamp of the country’s economic team after his reelection in May. Cevdet Akcay, Hatice Karahan and Fatih Karahan replace Emrah Sener, Taha Cakmak and Mustafa Duman at the Monetary Policy Committee, according to a decision published in the Official Gazette on early Friday. (BBG)

CHINA

INNOVATION: Policymakers will promote greater lending to science and innovation enterprises, according to Zhang Qingsong, deputy governor at the People’s Bank of China. Speaking at a State Council policy briefing, Zhang said the PBOC will encourage science and innovation firms to make use of international capital markets and ensure the high risk sector can obtain finance guarantees and insurance products which firms typically find difficult to access. Authorities will guide finance institutions to provide more credit for M&A activities and refinancing. (MNI)

HOUSING DEMAND: Local governments should further implement policies to support housing demand, such as reducing the down-payment ratio and loan interest rate for the purchase of first homes, tax relief for housing replacement, as well as relaxing loan restrictions, said the Minister of Housing and Urban-Rural Development Ni Hong in a recent meeting with property developers and builders. Ni called for homebuyers who have a mortgage history, but do not own property to be considered as first-time buyers. The ministry said the construction and real-estate industry represent two pillars of the economy and key to the economic recovery. (MNI)

REFORM: China should promote reforms that deepen opening to the outside world, according to Premier Li Qiang. On a recent tour of free trade zones in Shanghai, Li said China had benefited from partnerships with foreign companies and the government should take measures to attract foreign firms. Li acknowledged cross-border data flows remained a concern to all parties and called on relevant authorities to build a new cross-border data management system. On FTZs, the Premier instructed local officials to focus on meeting international trade rules and promoting institutional opening up. (MNI)

TECH: China has asked its largest technology companies to provide case studies of their most successful startup investments in consumer, telecom and media companies, a sign authorities are ready to grant them broader leeway in backing such deals after a crackdown brought them to a virtual halt two years ago. (BBG)

CHINA MARKETS

PBOC Net Injects CNY52 Bln Via OMOs Friday

The People's Bank of China (PBOC) conducted CNY65 billion via 7-day reverse repos on Friday with the rate unchanged at 1.90%. The operation has led to a net injection of CNY52 billion after offsetting the maturity of CNY13 billion reverse repo today, according to Wind Information.

- The operation aims to keep month-end liquidity stable, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8178% at 09:40 am local time from the close of 1.8268% on Thursday.

- The CFETS-NEX money-market sentiment index closed at 44 on Thursday, compared with the close of 46 on Wednesday.

PBOC Yuan Parity At 7.1265 Thursday Vs 7.1265 Thursday

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1338 on Friday, compared with 7.1265 set on Thursday.

OVERNIGHT DATA

South Korea Jun Industrial Production -1.0% M/M; Prior 3.0%

Japan July Tokyo CPI 3.2% Y/Y; Prior 3.2%

Japan July Tokyo CPI Ex-Fresh Food 3.0% Y/Y; Prior 3.2%

Japan July Tokyo CPI Ex-Fresh Food, Energy 4.0% Y/Y; Prior 3.8%

Australia Q2 PPI 0.5% Q/Q; Prior 1.0%

Australia June Retail Sales -0.8% M/M; Prior 0.8%

MARKETS

US TSYS: Curve Steeper, See-Saws On BOJ

TYU3 deals at 1110-30+, -0-02, a 0-17 range has been observed on volume of ~293k

- Cash tsys sit 2bps richer to 2bps cheaper, the curve has twist steepened pivoting on 5s.

- Tsys have see-sawed in recent dealing as JGBs provide the lead in Asia. Tsys initially firmed alongside JGBs in the aftermath of the BOJs rate decision, as they adjusted YCC, before falling sharply from session highs. Losses have been marginally pared in recent dealing.

- Earlier in the session participants faded yesterday's cheapening perhaps using the opportunity to close out short positions.

- Flow wise a block seller in FV, 5,655 lots, was the highlight.

- In Europe today regional German CPI provides the highlight. Further out we have US consumer income, employment cost index and University of Michigan consumer sentiment.

JGBs: Futures Sharply Lower As BoJ Effectively Widens YCC Band

JGB futures are just off session lows, -125 compared to settlement levels, after the BoJ's decision to maintain the policy balance rate at -0.1% and the 10-year JGB target at about 0% but adjust YCC to be flexibly managed.

- In effect, the BOJ said that the +/- 0.5% range around 0% in the 10-year JGB will be a “reference, not a rigid limit”. However, there will be a strict yield cap for fixed rate operations at 1.0%. That effectively makes the band the 10-year JGB can trade in much wider than anyone expected.

- Amidst a strong consensus leaning towards no policy change, echoing recent statements from BOJ Governor Ueda, the BoJ has adhered to the principle of not indicating the timing of any policy adjustments beforehand, as previously acknowledged by officials.

- The BoJ’s reasoning for this change is to “enhance the sustainability of monetary easing under the current framework by conducting yield-curve control with greater flexibility and nimbly responding to both upside and downside risks to Japan’s economic activity and prices.”

- Cash JGBs are 0.1bp to 13bp cheaper with the futures-linked 7-year zone leading. The benchmark 10-year yield is 10.5bp higher at 0.554%, above BoJ's YCC (now soft) limit of 0.50%.

- The swap curve has bear steepened with rates 0.1bp to 12.0bp higher. Swap spreads are wider apart from the 7-year.

- On Monday the local calendar sees Retail Sales, Industrial production, Consumer Confidence and Housing Starts.

AUSSIE BONDS: Sharply Weaker Despite Retail Sales Miss After BoJ Surprises

ACGBs (YM -10.0 & XM -14.5) sit sharply weaker, just above worst levels, as the local market’s attention turn to the surprise decision by the BoJ to tweak its yield curve control (YCC) policy.

- While the BoJ maintained its policy balance rate at -0.1% and the 10-year JGB target at about 0%, it adjusted YCC to be flexibly managed. In effect, the BOJ said that the +/- 0.5% range around 0% in the 10-year JGB will be a “reference, not a rigid limit”.

- Earlier in the day, ACGBs had pared morning weakness after retail sales printed significantly below expectations.

- Cash ACGBs are 9-15bp cheaper with the 3/10 curve steeper and the AU-US 10-year yield differential -2bp at +6bp.

- Swap rates are 8-11bp higher with EFPs 3bp narrower.

- The bills strip bear steepens with pricing flat to -9.

- RBA-dated OIS pricing is 2-5bp firmer for meetings beyond December.

- (AFR) An unexpected fall in spending has given the RBA more reasons to pause raising interest rates. (See link)

- On Monday, the local calendar sees the MI Inflation Gauge, Private Sector Credit and CoreLogic House Prices data.

- Nevertheless, the week’s highlight will be the RBA Policy Decision on Tuesday. Bloomberg consensus expects a 25bp hike to 4.35%.

NZGBS: Cheaper With $-Bloc Bonds After Surprise YCC Tweak From BoJ

NZGBs closed 4-9bp weaker, but off session cheaps, as $-bloc bonds react to the surprise decision by the BoJ to tweak its yield curve control (YCC) policy. The BoJ maintained the policy balance rate at -0.1% and the 10-year JGB target at about 0% but adjusted YCC to be flexibly managed. In other words, the BoJ said that the +/- 0.5% range around 0% in the 10-year JGB will be a “reference, not a rigid limit”.

- US tsys sit 2bp richer to 2bp cheaper as the curve twist steepens, pivoting on 5s. US tsys have see-sawed in recent dealing as JGBs provide the lead in Asia. Tsys initially firmed alongside JGBs in the aftermath of the BoJs rate decision. Losses have been marginally pared in recent dealing.

- Swap rates are 7-12bp higher with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed flat to 7bp firmer across meetings, with Jul’24 leading. Terminal OCR expectations sit at 5.66%.

- Next week the local calendar sees ANZ Business Confidence (Jul) on Monday, CoreLogic House Prices (Jul) and Building Permits (Jun) on Tuesday and Q2 Employment and Wages data on Wednesday.

- Later today, the US calendar sees the release of the Q2 Employment Cost Index along with the June PCE deflator.

GOLD: Pressured By Stronger US Data As USD & US Tsy Yields Move Higher

Gold is +0.3% in the Asia-Pac session, after closing -1.35% at $1946 on Thursday as the US dollar surged on a combination of strong data and a dovish ECB.

- US data releases included much stronger than expected GDP, lower than projected jobless claims, a pop in durable goods orders, a bounce in pending home sales, and a narrowing in the goods trade deficit.

- The ECB delivered the well-anticipated 25bps hike that took the deposit rate to 3.75%, a record high for the Euro area. However, forward guidance by the ECB was seen by the market as more dovish than expected. EGBs finished 1-5bp richer with the curve steeper.

- Treasury yields also climbed strongly with an added tailwind from BoJ YCC speculation ahead of the upcoming decision.

- Bullion cleared support at the 50-day EMA of $1951.2 with a low of $1942.65, after which lies further support at $1924.5 (Jul 11 low).

OIL: Crude Set To Finish Week Higher Again, WTI Struggles To Break $80

Oil prices are down around 0.5% today after the optimism-driven +1% rise on Thursday, but they have been trading in a narrow range. WTI is around $79.71/bbl after reaching a high of $79.88, as it is still struggles to break $80. It is currently up 3.4% on the week. Brent is around $83.75 following a high of $83.92. The USD index is flat.

- Better US Q2 GDP, possibility Fed may be close to done, economic measures in China and signs of reduced output have supported crude this week and this month. Lower crude inventories in Cushing, down 7.5mn barrels over last 4 weeks, are also helping. As a result some forecasters, such as Standard Chartered and UBS, are revising up prices, according to Bloomberg.

- Exxon and Chevron report today which will include their assessment of the outlook.

- Russia has said that it will meet its OPEC+ output reduction commitments fully in August. Shipping data has shown lower output this month. Saudi Arabia has also said that it will extend its voluntary cuts to next month.

- Later the US Q2 employment cost index, June spending/income including core PCE deflator, and final Michigan consumer survey for July print. There are also preliminary German Q2 GDP and July European Commission survey data.

FOREX: Yen Firmer In Volatile Trade Post-BOJ

The Yen is now sitting firmer in post-BOJ trade after see-sawing as participants digested the decision. The BOJ tweaked YCC to be flexibly managed, in effect, the BOJ says that the +/- 0.5% range around 0% in the 10-year JGB will be a “reference, not a rigid limit”. However, there will be a strict yield cap for fixed rate operations at 1.0%. That effectively makes the band the 10-year JGB can trade in much wider than anyone expected.

- USD/JPY see-sawed on the decision initially falling printing a low at ¥138.63 before firming to a high of ¥141.94. The pair now sits ~1.8% below its post meeting peak, however has ticked away from session lows and sits at ¥138.35/45.

- AUD is pressured, the post BOJ flows have spilled over into risk off flows seeing the AUD extend early losses. June Retail Sales fell 0.8% vs a 0.0% expected print. The pair has broken support at $0.6651, the low from July 11 and last prints at $0.6645/50.

- Kiwi is also pressured, NZD/USD is down ~0.5% as risk off flows weigh. The next support level is $0.6051 the low from 29 June.

- Cross asset wise; 10-Year US Tsy Yields are ~3bps higher and e-minis are down ~0.1% having been up as much as 0.3% early in the session.

- French CPI and Regional CPI from Germany provide the highlight in todays European session.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/07/2023 | 0530/0730 | *** |  | FR | GDP (p) |

| 28/07/2023 | 0530/0730 | ** | | FR | Consumer Spending |

| 28/07/2023 | 0530/0730 | *** |  | DE | North Rhine Westphalia CPI |

| 28/07/2023 | 0600/0800 | ** |  | SE | Unemployment |

| 28/07/2023 | 0600/0800 | ** | | SE | Retail Sales |

| 28/07/2023 | 0645/0845 | *** | | FR | HICP (p) |

| 28/07/2023 | 0645/0845 | ** | | FR | PPI |

| 28/07/2023 | 0700/0900 | *** |  | ES | GDP (p) |

| 28/07/2023 | 0700/0900 | *** | | ES | HICP (p) |

| 28/07/2023 | 0800/1000 | ** |  | IT | PPI |

| 28/07/2023 | 0800/1000 | *** | | DE | Bavaria CPI |

| 28/07/2023 | 0900/1100 | ** |  | EU | EZ Economic Sentiment Indicator |

| 28/07/2023 | 0900/1100 | *** | | DE | Saxony CPI |

| 28/07/2023 | 1200/1400 | *** | | DE | HICP (p) |

| 28/07/2023 | 1230/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 28/07/2023 | 1230/0830 | ** |  | US | Personal Income and Consumption |

| 28/07/2023 | 1230/0830 | ** | | US | Employment Cost Index |

| 28/07/2023 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 28/07/2023 | 1500/1100 | | CA | Finance Dept monthly Fiscal Monitor (expected) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.