Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- US TO IMPOSE MANDATORY COVID-19 TESTS FOR TRAVELERS FROM CHINA (RTRS)

- CHINA’S TOP ECONOMIC PLANNER URGES ECONOMY TURNAROUND (XINHUA)

- YUAN COULD RISE TO 6.6 AGAINST US DOLLAR IN 2023 (HERALD)

- S.KOREA MAY REQUIRE COVID TESTS FOR TRAVELERS FROM CHINA (CHOSUN)

- AUSTRALIAN MINISTER RAISES HOPES FOR TRADE THAW WITH CHINA (BBG)

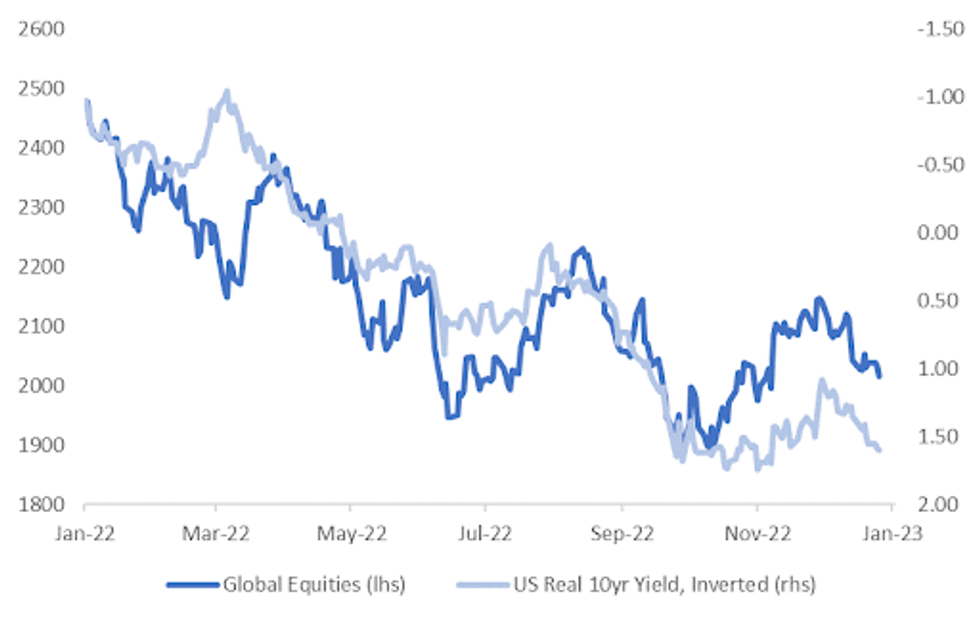

Fig. 1: Global Equities And US Real 10yr Yield (Inverted)

Source: MNI - Market News/Bloomberg

UK

POLITICS: Rishi Sunak trails Boris Johnson and Suella Braverman in votes for Tory members’ minister of the year in the latest survey to suggest that he has yet to win over his party’s grassroots. (The Times)

ECONOMY: British consumers plan to cut back on restaurant meals and non-essential shopping next year after a surge in the cost of living ate into disposable income. The consulting firm KPMG said almost two-thirds of the 3,000 people it surveyed felt the need to reduce spending and save more because inflation hit the highest in four decades. It found people paying more for basics like food, mortgages and energy bills.(BBG)

EUROPE

CORONAVIRUS: Italy will begin testing all arrivals from China for Covid, and wants European Union countries to do the same, after a virus scare at Milan airport. (BBG)

CORONAVIRUS: Milan health authorities said that almost half of the passengers on two flights from China tested positive for Covid. Milan’s region health chief said at a press conference Wednesday that airport authorities tested passengers who arrived on two flights, one from Beijing and one from Shanghai. China has seen outbreaks since the government there abandoned its strict zero-Covid policies. (BBG)

GEOPOLITICS: The United States, NATO and European Union urged maximum restraint in the north of Kosovo, as authorities closed a third border crossing on Wednesday and tensions escalated with local Serbs over its 2008 independence. (RTRS)

U.S.

ECONOMY: Goldman Sachs Group Inc. is working on a fresh round of staff cuts that will be unveiled in a matter of weeks, Chief Executive Officer David Solomon said in his traditional year-end message to staff. (BBG)

CORONAVIRUS: The United States will impose mandatory COVID-19 tests on travelers from China, U.S. health officials said on Wednesday, joining India, Italy, Japan and Taiwan in taking new measures after Beijing's decision to lift stringent zero-COVID policies (RTRS)

OTHER

JAPAN: Japanese Prime Minister Fumio Kishida plans to visit Group of Seven nations including the US, the UK and France in Jan. for bilateral meetings with his counterparts, public broadcaster NHK reports, citing an unidentified government official. Hopes to build up rapport ahead of G-7 summit in Hiroshima in May. Looks to discuss issues including the situation in Ukraine, nuclear disarmament and climate change (NHK)

BOJ: Former Bank of Japan Deputy Governor Hirohide Yamaguchi, a vocal critic of Governor Haruhiko Kuroda's stimulus programme, is emerging as a strong candidate to become next head of the central bank, the Sankei newspaper reported on Thursday. (RTRS)

SOUTH KOREA: South Korean government is likely to require visitors from China to take rapid antigen test for Covid-19 and also ask for PCR test results taken before 48 hours prior to arrival, Chosun Ilbo newspaper says, without citing anyone. South Korea to discuss such measures Thursday and make final announcement on Friday (CHOSUN).

AUSTRALIA: Australia would be willing to reconsider its case against China at the World Trade Organization if Beijing’s sanctions against its exports were lifted, as Trade Minister Don Farrell flagged a potential thaw in the trade tensions between the two countries. (BBG)

HONG KONG: The daily quota for travelers from Hong Kong to China is tentatively set at 30,000 for the initial stage of reopening, Sing Tao reports, citing unidentified people. All border control points will be opened. (Sing Tao)

CHINA

CORONAVIRUS: Chinese hospitals and funeral homes were under intense pressure on Wednesday as a surging COVID-19 wave drained resources, while the scale of the outbreak and doubts over official data prompted some countries to enact new travel rules on Chinese visitors. (RTRS)

ECONOMY: China’s removal of the last of its Covid curbs will likely bring more disruption to the economy through the first quarter as infections surge, while increasing the possibility of a faster and stronger rebound in growth next year, economists said. (BBG)

ECONOMY: Experts are divided on the extent to which China’s household pandemic era savings can fuel a rebound in consumption in 2023, according to Yicai.com. A recent survey by the People’s Bank Of China (PBOC) showed 61% of urban residents intend to "save more", up 3.7 percentage points over the previous quarter, with 22.8% intending to “consume more”. Some experts believe the large increase in household deposits during the pandemic will be able to support a consumption rebound in 2023, but others say a large part of the savings is ringfenced for future real estate purchases once confidence has returned to the property sector, or are the result of investors liquidating bond positions as yields have declined, according to Yicai.com. (MNI)

FX: The yuan is expected to rise by about 5% to reach about 6.6 against the U.S. dollar next year as the Federal Reserve may end its rate hikes around mid-2023 as U.S. inflation cools, and as China’s GDP rebounds on reopening, 21st Century Business Herald reported citing Wang Qing, chief analyst at Golden Credit Rating. It is possible the yuan may fluctuate around 7 in the first half of 2023 as U.S. interest rates may still rise and support the U.S. Dollar Index, the newspaper said citing Wu Zhaoyin, director of AVIC Trust. It is not recommended to bet on the one-way appreciation of yuan, as the currency may also be impacted by Sino-U.S. relations, the global geopolitical situation and domestic real estate market, the newspaper cited Wang as saying. (MNI)

EQUITIES: Foreign financial institutions have become more bullish about China's stock market performance in 2023 as the signs of the country's economic stabilization become increasingly noticeable amid stimulus measures and the accelerated optimization of epidemic control measures.(CHINA DAILY)

CHINA MARKETS

PBOC NET INJECTS CNY201 BILLION VIA OMOs THURSDAY

The People's Bank of China (PBOC) on Thursday injected CNY205 billion via 7-day reverse repos with the rates unchanged at 2.00%. The operation has led to a net injection of CNY201 billion after offsetting the maturity of CNY4 billion reverse repos today, according to Wind Information.

- The operation aims to keep year-end liquidity stable, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) fell to 2.0000% at 9:24 am local time from the close of 2.1517% on Wednesday.

- The CFETS-NEX money-market sentiment index closed at 45 on Wednesday vs 47 on Tuesday.

PBOC SETS YUAN CENTRAL PARITY AT 6.9681 THURS VS 6.9546 WEDS

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 6.9793 on Thursday, compared with 6.9681 set on Wednesday.

OVERNIGHT DATA

SOUTH KOREA NOV INDUSTRIAL PRODUCTION +0.4% M/M; MEDIAN -0.8%; OCT -3.5%

SOUTH KOREA NOV INDUSTRIAL PRODUCTION -3.7% Y/Y; MEDIAN -4.9%; OCT -1.2%

SOUTH KOREA CYCLICAL LEADING INDEX -0.2 M/M; OCT -0.1

SOUTH KOREA NOV RETAIL SALES +8.4% Y/Y; OCT 7.3%

SOUTH KOREA NOV DEPARTMENT STORE SALES +3.7% Y/Y; OCT 8.0%

SOUTH KOREA NOV DISCOUNT STORE SALES +9.2% Y/Y; OCT -0.5%

MARKETS

US TSYS: Richening Holds Through Asian Session

TYH3 deals at 112-12, +0-06, a touch off the top of its 0-06+ range on light volume of ~5k

- The early richening has extended a touch through the session with cash tsys running 0.5-3bps richer with the belly leading the strength.

- With limited macro newsflow and thin volume through Asia-Pac today, local participants faded the cheapening seen through the Europe and NY sessions yesterday.

- There is a thin data calendar in Europe today, further out US Initial Jobless Claims is the main point of interest ahead of a 7Y auction.

OIL: Crude Prices Lower As Market Growth Concerns Rise

MNI (Australia) - Oil has been trading in a tight range again today on thin year-end liquidity. WTI is down slightly again by 0.3% to about $78.70/bbl after falling 0.8% on Wednesday, as fears of a new global Covid wave grow. Brent is down 0.3% to $83.00. DXY is flat on the NY close.

- The Australian is reporting that the US, Italy, India, Japan and Taiwan have introduced procedures for incoming travellers from China after the end of its quarantine rules. The possible global spread of Covid has created some uncertainty in markets over the boost to growth from China’s reopening (bbg).

- Oil has traded in a wide range this year with WTI reaching a peak of $105.94/bbl at the beginning of June and a trough at the start of 2022 of $70.03, before the Russian invasion of the Ukraine. Brent had a high of $110.46 and a low at $73.68.

- API crude inventories fell 1.3mn in the latest data after a 3.07mn drawdown in the previous week. Distillate and gasoline stocks were higher.

- Another quiet day with only US jobless claims and EIA inventory data scheduled later.

GOLD: Bullion Up Slightly, Holding Above $1805/oz

Gold prices are up 0.2% during today’s session after falling 0.5% on Wednesday as trend conditions remain bullish. It is currently trading around $1807.50/oz after reaching a high of $1809.38 and a low of $1804.34. DXY is down 0.1%.

- Gold moves inversely with the USD. Many analysts are expecting bullion to rally later in 2023 as the USD eases with the slowdown and eventual pause of Fed tightening. Higher yields are likely to weigh on bullion but a lower USD should make it cheaper for non-US buyers.

- Gold hit a low of $1622.36 at the end of September this year and a high of $2050.76 at the start of March.

- Another quiet day with only US jobless claims scheduled later.

EQUITIES: Major Indices Tracking Lower As China Optimism Is Tempered

(MNI Australia) Regional equities have mostly followed the negative EU/US lead from Wednesday's session and are tracking lower today. Tech sensitive plays have again seen the largest falls. US futures are slightly higher, with the Nasdaq around +0.25/0.30% higher at this stage, while other major indices are closer to flat.

- Much of the focus remains on countries imposing restrictions on tourist/visitor arrivals from China, amid the current onshore outbreak and as China removes constraints on inbound/outbound travel.

- The HSI is down by 1.1%, the underlying tech index down 2.60%, more than unwinding yesterday's gain. More game approvals from China regulators failed to buoy sentiment, although it suggests potentially less regulatory burden on the sector as we move into 2023.

- Mainland shares are down, with the CSI 300 off by 0.41%.

- The Kospi is down a further 1.44%, led by the electronics sector. Offshore investors have sold a further -$232.8mn of local shares. The Taiex is down by 0.55%, the Nikkei 225 off by 1.15%.

- Only Malaysia, Thailand and Indonesian stock indices are in positive territory so far today.

FOREX: USD Slips, As Yields Soften, JPY & NZD Outperform

The USD has tracked lower through today's session, with the BBDXY back sub 1255, around 0.25% off NY closing levels. JPY and NZD have been the standouts, while lower US cash Tsy yields, led by the belly of the curve have been a broader USD headwind.

- USD/JPY hit lows of 133.50, but is now back near 133.65, still +0.60% for the session in yen terms. Post yesterday's Asia close we saw the dip sub 133.50 supported, so this may be a short-term support point. Next year the focus will be on the BoJ policy outlook, with Reuters reporting that ex BoJ Deputy Yamaguchi (who opposed Kuroda's stimulus program) is a potential contender to replace Kuroda.

- NZD/USD is up 0.50%, last near 0.6345. Yesterday's highs came in just above 0.6355. The NZD hasn't been affected by the negative tone to regional equities, while AUD/NZD downside has likely helped at the margin. The cross is back to 1.0640, after reaching 1.0766 yesterday.

- AUD/USD is up around 0.2%, tracking 0.6750 currently.

- Event risk is relatively limited for the offshore session, with the ECB publishing its monthly Economic Bulletin. In the US, jobless claims are on tap.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/12/2022 | 0800/0900 |  | ES | Retail Sales | |

| 29/12/2022 | 0900/1000 | ** |  | EU | M3 |

| 29/12/2022 | 1330/0830 | ** |  | US | Jobless Claims |

| 29/12/2022 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 29/12/2022 | 1600/1100 | ** | | US | DOE weekly crude oil stocks |

| 29/12/2022 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 29/12/2022 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 29/12/2022 | 1800/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.