Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- FED OFFICIALS SEE SLOWDOWN IN HIKE PACE 'SOON' - MINUTES (MNI)

- CENTENO WANTS ECB TO SEND CLEAR MESSAGE OF GENTLER RATE HIKES (RTRS)

- BOE’S TOP ECONOMIST SAYS MORE RATE RISES NEEDED TO TACKLE INFLATION (BBG)

- RBNZ POLICY IS ‘CONTRACTIONARY’ AFTER RECORD RATE HIKE, ORR SAYS (BBG)

- SPECULATION SWIRLS RE: IMMINENT PBOC RRR CUT

- CHINA ORDERS COVID LOCKDOWN IN ZHENGZHOU AFTER IPHONE FACTORY PROTESTS (BBG)

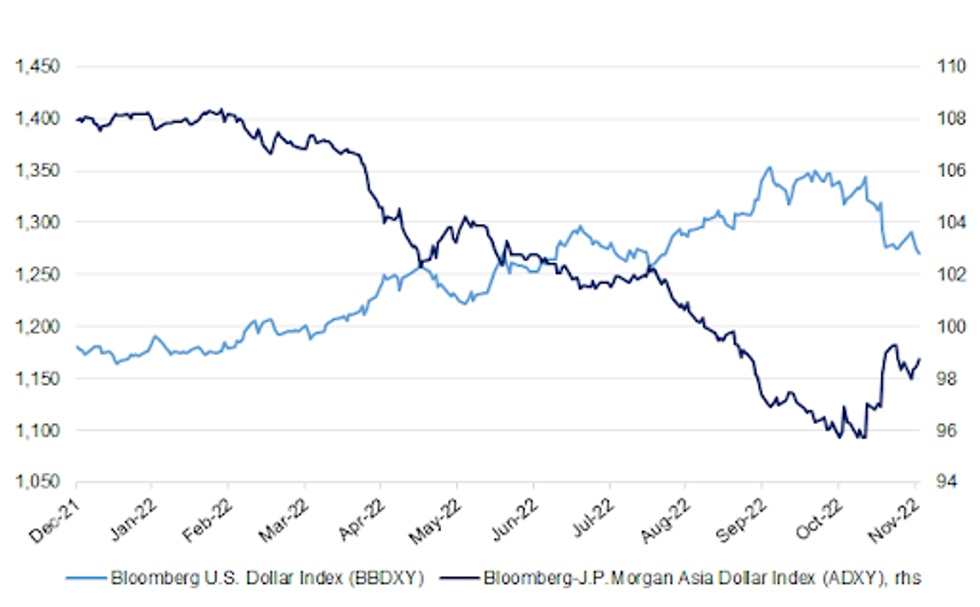

Fig. 1: Bloomberg U.S. Dollar Index (BBDXY) Vs. Bloomberg-J.P.Morgan Asia Dollar Index (ADXY)

Source: MNI - Market News/Bloomberg

UK

BOE: The Bank of England needs to raise interest rates further to tackle inflationary pressures that are becoming increasingly domestic, Chief Economist Huw Pill said. (BBG)

BOE: The Bank of England set out operational details on Wednesday of its plans to start selling some of the 19 billion pounds ($23 billion) of long-dated and index-linked gilts which it bought last month to stabilise financial markets. (RTRS)

POLITICS: Rishi Sunak this week warned his cabinet that Britain faced “a challenging period” this winter, but as the country’s problems pile up, the new prime minister is also facing a serious test of his own political authority. With opinion polls still giving Labour a 20-point lead, a fatalistic mood has fallen on many Tory MPs, some of whom privately claim the next election is already lost; others are looking to a new career outside Westminster. (FT)

POLITICS: Rishi Sunak could be forced to compromise with rebel MPs over the scrapping of housing targets to avoid relying on Labour votes to pass the levelling up bill. (Guardian)

BREXIT: The EU will demand that derivatives traders use accounts at clearing houses in the bloc for some of their transactions, as part of plans to take a share of the €115tn market processed through the City of London. (FT)

BREXIT/POLITICS: Rishi Sunak has been told to drop plans to remove EU-derived law from the statue book by several business, legal, worker and environmental groups. (The Times)

EUROPE

ECB: The European Central Bank should slow the pace of interest rate hikes from December and send a clear message that record 75-basis-point increases are not the norm as inflation is likely to peak this quarter, policymaker Mario Centeno told Reuters. (RTRS)

U.S.

FED: Fed officials at their November meeting supported slowing the pace of interest rate hikes "soon" to give them time to observe the effects of higher rates on the economy and inflation, according to the minutes of the meeting released Wednesday, signaling a 50 basis point increase was likely next month. (MNI)

FED: Federal Reserve staff economists briefed policymakers this month that the chances of a US recession in the next year had risen to almost 50% on risks of slower consumer spending, global economic risks and further interest-rate hikes. (BBG)

OTHER

EU/CHINA: European Council president Charles Michel will travel to Beijing for a meeting with Xi Jinping next month, in a move likely to highlight European divisions on how to engage with China. (FT)

CHINA/TAIWAN: Taiwan is targeting resumption of mini-three links before the Lunar New Year holiday in 2023, deputy minister of Mainland Affairs Council Chiu Chui-cheng tells lawmakers in Taipei. (BBG)

JAPAN: Japanese Prime Minister Fumio Kishida sought to brush off a magazine report that questioned election expenses from last year by saying that while some receipts his office submitted didn’t include complete information, the money had been spent appropriately. (BBG)

RBNZ: New Zealand central bank governor Adrian Orr said monetary policy is now contractionary after yesterday’s record interest-rate hike. (BBG)

NEW ZEALAND: New Zealand's house prices are forecast to fall more than previously thought this year and next with a peak-to-trough slump of 18% as aggressive interest rate hikes weaken an already-slowing housing market, a Reuters poll found. (RTRS)

BOK: South Korea's central bank raised its policy rate by a quarter percentage point Thursday to tame persistently high inflation but slowed the pace of monetary tightening amid worries over high borrowing costs and their impact on economic growth. (Yonhap)

SOUTH KOREA: Unionised truckers in South Korea kicked off their second major strike in less than six months on Thursday, threatening to disrupt manufacturing and fuel supplies for industries from autos to petrochemicals in the world's 10th-largest economy. (FT)

HONG KONG: Billionaire investor Bill Ackman said he's betting the Hong Kong dollar will fall and that its peg to the U.S. dollar can break, the latest big money manager to take a public short bet as U.S. rate hikes turn the blowtorch on Hong Kong's currency system. (RTRS)

NORTH KOREA: North Korean leader Kim Jong Un's powerful sister, Kim Yo Jong, on Thursday denounced Seoul's push to impose additional sanctions on Pyongyang following its repeated missile launches, saying such measure will add to the North's "hostility and anger," state media KCNA reported. (RTRS)

BOC: Bank of Canada Governor Tiff Macklem reiterated Wednesday the end of the rate hiking cycle is nearing but it will take time to slow inflation to target, without giving a specific clue on the size of the next interest rate move on Dec. 7. (MNI)

BRAZIL: The head of Brazil's electoral court Alexandre de Moraes on Wednesday rejected a complaint from President Jair Bolsonaro's allies to challenge the presidential election, which the incumbent lost by a small margin, according to a court document. (RTRS)

BRAZIL: Brazil's central bank chief Roberto Campos Neto on Wednesday reiterated concerns about the spending program planned by the government of President-elect Luiz Inacio Lula da Silva, saying it had not been explained well. (RTRS)

ENERGY: The 27 European Union countries disagreed on Wednesday over a proposal by the bloc's executive to cap future gas prices at 275 euros per megawatt-hour (MWh), a plan that has swiftly drawn criticism from both backers and opponents. (RTRS)

ENERGY: Germany looks like accepting European Commission tweaks to a proposed gas price cap to ease concerns that it might cause LNG exporters to divert cargoes to Asia in search of higher prices, with an agreement on the mechanism likely by the end of the year, EU sources told MNI. (MNI)

ENERGY: Energy traders would have to stump up an additional $33bn in margin payments if a plan by Brussels to cap the price of a key European gas benchmark goes ahead, a leading exchanges operator has warned. (FT)

OIL: Talks between European Union nations on where to set a proposed Group of Seven price cap on Russian oil bogged down Wednesday evening, as governments split over how to design the plan, according to people familiar with the matter. (BBG)

OIL: The Group of Seven (G7) nations' proposed price cap of $65-$70 a barrel on Russian oil would have little immediate impact on Moscow's revenues, as it is broadly in line with what Asian buyers are already paying, five industry sources with direct knowledge of the purchases said on Wednesday. (RTRS)

OIL: Oil pumping through the Ukrainian section of the Druzhba pipeline has resumed at the scheduled volume after being partially suspended, Russia's state-owned pipeline operator Transneft said on Wednesday, according to Russia's TASS news agency. (RTRS)

CHINA

CORONAVIRUS: China’s daily Covid infections climbed to a record high, exceeding the previous peak in April, as it battles an outbreak that has grown since the country adopted a more targeted approach to containing the virus. (BBG)

PBOC: The People’s Bank of China is expected to cut the reserve requirement ratio on Friday, after the State Council executive meeting on Wednesday mentioned using RRR cuts in a timely and appropriate manner to maintain reasonable and ample liquidity, 21st Century Business Herald reported. (MNI)

PROPERTY: Major Chinese developer Country Garden (2007.HK) has signed a contract with the Postal Savings Bank of China (1658.HK) for a credit line of up to 50 billion yuan ($7.0 billion), Securities Times reported on Thursday. (RTRS)

CHINA MARKETS

PBOC NET DRAINS CNY124 BILLION VIA OMOS THURSDAY

The People's Bank of China (PBOC) on Thursday injected CNY8 billion via 7-day reverse repos with the rates unchanged at 2.00%. The operation has led to a net drain of CNY124 billion after offsetting the maturity of CNY132 billion reverse repos today, according to Wind Information.

- The operation aims to keep liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.8999% at 9:27 am local time from the close of 1.5982% on Wednesday.

- The CFETS-NEX money-market sentiment index closed at 50 on Wednesday vs 47 on Tuesday.

PBOC SETS YUAN CENTRAL PARITY AT 7.1201 THURS VS 7.1281 WEDS

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1201 on Thursday, compared with 7.1281 set on Wednesday.

OVERNIGHT DATA

JAPAN NOV, P JIBUN BANK MANUFACTURING PMI 49.4; OCT 50.7

JAPAN NOV, P JIBUN BANK SERVICES PMI 50.0; OCT 53.2

JAPAN NOV, P JIBUN BANK COMPOSITE PMI 48.9; OCT 51.8

Activity at Japanese private sector firms declined for the first time in three months, according to November flash PMI data. Central to the latest downturn was a poor performance at Japanese manufacturing firms. (S&P Global)

JAPAN SEP, F LEADING INDEX 97.5; AUG 101.3

JAPAN SEP, F COINCIDENT INDEX 101.4; AUG 101.8

JAPAN OCT, F MACHINE TOOL ORDERS -5.5 Y/Y; SEP +4.3%

SOUTH KOREA OCT PPI +7.3% Y/Y; SEP +7.9%

MARKETS

SNAPSHOT: Fed Minutes Reverberate Around Asia

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 up 303.92 points at 28421.2

- ASX 200 up 10.035 points at 7241.8

- Shanghai Comp. down 5.964 points at 3090.943

- JGB 10-Yr future up 8 ticks at 149.42, yield down 0bp at 0.249%

- Aussie 10-Yr future up 4.0 ticks at 96.450, yield down 4.3bp at 3.546%

- U.S. 10-Yr future up 0-05 at 113-03+, cash Tsys are closed

- WTI crude down $0.20 at $77.74, Gold up $4.77 at $1,754.46

- USD/JPY down 83 pips at Y138.77

- FED OFFICIALS SEE SLOWDOWN IN HIKE PACE 'SOON' - MINUTES (MNI)

- CENTENO WANTS ECB TO SEND CLEAR MESSAGE OF GENTLER RATE HIKES (RTRS)

- BOE’S TOP ECONOMIST SAYS MORE RATE RISES NEEDED TO TACKLE INFLATION (BBG)

- RBNZ POLICY IS ‘CONTRACTIONARY’ AFTER RECORD RATE HIKE, ORR SAYS (BBG)

- SPECULATION SWIRLS RE: IMMINENT PBOC RRR CUT

- CHINA ORDERS COVID LOCKDOWN IN ZHENGZHOU AFTER IPHONE FACTORY PROTESTS (BBG)

US TSYS: Futures Twist Steepen A Touch In Holiday-Thinned Trade

The Tsy futures curve twist steepened a touch overnight, with the Asia-Pac reaction to the slightly dovish feel to the minutes covering the latest FOMC decision, and to a lesser degree soft U.S. PMI & jobless claims data, allowing that dynamic to unfold.

- Contracts out to UXY remain underpinned, while WN & US futures are softer on the day. TYZ2 deals +0-04+ at 113-03, operating in a narrow 0-05+ range on sub-standard volume of ~45K

- A reminder that futures will be subjected to curtailed trading hours and thinner liquidity on Thursday owing to the observance of the Thanksgiving holiday, while cash Tsys are closed until Friday’s Asia-Pac session.

- In terms of meaningful macro news flow, Asia-Pac hours saw another uptick in Chinese COVID cases, with the daily new case count exceeding the previous peak lodged earlier this year. More localised lockdowns were declared in the country.

- ECB speak headlines Thursday’s global docket.

JGBS: A Touch Firmer After Holiday

A modest bid crept into the JGB space as Tokyo participants played catch up after their mid-week holiday, leaving the major benchmarks 0.5-1.5bp richer across the curve, while JGB futures nudged higher, operating in a contained range to finish +5. The supportive global factors that we have outlined elsewhere aided the early bid.

Local headline flow saw PM Kishida push back against the recent speculation surrounding the potential for a fairly imminent cabinet reshuffle.

- A softer round of PMI surveys was also observed, with the survey collators writing “activity at Japanese private sector firms declined for the first time in three months, according to November flash PMI data. Central to the latest downturn was a poor performance at Japanese manufacturing firms.”

- Looking ahead, Friday’s local docket is headlined by Tokyo CPI and services PPI data

AUSSIE BONDS: Firmer & Flatter On Global Inputs

The impulse from a firmer core global FI complex, linked to soft U.S. data, a dovish feel to the minutes covering the latest FOMC decision, the prospect of further monetary easing in China and firm demand at the latest round of longer dated NZGB auctions fed into demand for ACGBs, allowing the space to firm on Thursday.

- That left YM +3.0 & XM +4.5 at the bell, with wider cash ACGB trade seeing 2-6bp of richening as the curve bull flattened.

- Bills were flat to 3bp richer through the reds come the close, erasing early losses to bull flatten at the margin.

- We didn’t get much in the way of headline flow to facilitate idiosyncratic moves, with the local data docket and speaker schedule somewhat empty.

- Looking ahead, Friday will bring the release of the weekly AOFM issuance slate and A$700mn of ACGB Apr-25 supply.

NZGBS: Auction Dynamics Promote Flattening

The broader bid in core global FI markets observed during Asia-Pac hours generally facilitated an extension of the early bid in NZGBs.

- This, coupled with a solid round of demand at the latest NZGB May-32 & Apr-37 auctions, as each line saw 1 successful bidder, who paid up for access to the lines (note the NZGB Apr-25 leg of the auctions was only covered 1.00x and saw an ~11bp wide spread of accepted yields, probably on the back of some RBNZ-related caution, which weighed on the shorter end of the curve), promoted curve flattening, with the major NZGB benchmarks finishing flat to 9bp richer.

- Swap spreads were tighter in the front end to little changed further out, with the 2-/10-Year swap differential pulling further into inverted territory.

- RBNZ dated OIS price just over 70bp of tightening for the RBNZ’s next meeting (which will be held in Feb ’23), with a terminal OCR of just over 5.45% eyed (compared to the 5.50% peak seen in the Bank’s latest OCR track projection).

- Post-meeting parliamentary testimony from RBNZ Governor Orr & chief economist Conway mimicked the post-meeting statement’s focus on inflation, with Orr highlighting that the OCR is now in contractionary territory.

- Looking ahead Q3 retail sales volume data and the monthly ANZ consumer confidence survey headline the domestic docket on Friday.

EQUITIES: Mostly Higher On FOMC Mins, Although Chinese Indices Give Back Early Gains

The slightly dovish feel to the minutes covering the latest FOMC meeting, coupled with a softer USD, as well as realised and swirling expectations for further Chinese policy support, allowed the majority of the major Asia-Pac equity indices to tick higher on Thursday.

- The Nikkei 225 outperformed its regional peers after the mid-week Japanese holiday, adding just over 1.00% as we head into the close, although a firmer JPY likely capped the strength in Japanese equities.

- The CSI 300 gave back its modest, early gains with a fresh round of localised COVID restrictions in China weighing. Still, the property sector outperformed on signs of the latest step up in policy support for the sector.

- E-minis nudged ~0.2% higher against this backdrop.

OIL: Prices Range Trading After Overnight Correction

Oil prices have been in a tight range today around the NY close of $77.94/bbl for WTI and $85.41 for Brent. Prices fell sharply overnight on continued Chinese demand concerns and discussions that the EU will implement a softer Russian oil price cap. WTI is now well below its 50-day MA.

- WTI has been trading between $77.30 and $78.00 today and Brent between $85 and $85.31.

- It looks like the EU will introduce an oil price cap on Russian shipments of $65-$70 rather than the originally proposed $40-$60. This would reduce the risks of severe retaliation from Russia. A higher cap is also likely to keep crude prices lower overall, given Russia’s influence it would allow more of its output onto the global market. Goldman Sachs doesn’t think that the cap at this level will be effective in hurting Russia and only the current oil embargo will impact its supply.

- The EIA reported a 3.69mn barrel drawdown in crude inventories in the US after -5.4mn last week. However, there was a much needed build in distillate and gasoline stocks of 1.72mn and 3.06mn respectively.

- The US is closed for Thanksgiving. But there is the German IFO in Europe and the ECB meeting accounts plus a number of ECB speakers.

GOLD: Gold Prices Higher As USD Softens On December Fed Pivot

The gold price responded positively to the weaker USD in response to the signal from the FOMC minutes that there is likely to be a smaller rate hike in December. Bullion closed the NY session at just under $1750/oz but spot has moved 0.35% from there today to trade around $1755, as DXY as fallen another 0.35%.

- Gold has struggled this year as the Fed implemented aggressive monetary tightening. Signs that it may be slowing are good for bullion. But prices are still some way off the bull trigger of $1786.50, the November 15 high.

- The US is closed for Thanksgiving and so trading is likely to be light tonight. But there is the German IFO in Europe and the ECB meeting accounts plus a number of ECB speakers.

FOREX: Dollar Under Pressure In Wake Of FOMC Minutes & U.S. Data

Thanksgiving holiday-thinned Asia-Pac trade was dominated by regional reaction to Wednesday’s soft U.S. economic data (PMIs and jobless claims) and the FOMC meeting minutes, which pressured the USD.

- We saw another uptick in COVID cases in China, with new daily case numbers in the country now through their previous ’22 peak.

- The JPY leads the G10 FX pack, with Tokyo returning from a mid-week holiday.

- Elsewhere, RBNZ Governor Orr & chief economist Conway reiterated the Bank’s focus on getting inflation under control in an early parliamentary address.

- We also saw the BoK deliver the widely expected 25bp rate hike, although the Bank signalled the likelihood that the tightening cycle will draw to an end in the early part of ’23, while indicating the board’s range of preferences re: the terminal rate (from no more tightening to 50bp of additional hikes).

- USD/CNH operates within the confines of Wednesday’s range, with no bias observed in today’s USD/CNY mid-point fixing, as markets looked through the latest round of COVID lockdowns in China and leant on both realised and expected support for the Chinese economy, which supported the yuan at the margin.

- Asia FX played catch up to the USD weakness witnessed since yesterday’s local market closes, with the respective moves extending throughout the day.

- German IFO data, the accounts covering the latest ECB meeting and a range of ECB speakers headline on Thursday. A reminder that the U.S. observes a public holiday today.

FOREX OPTIONS: Expiries for Nov24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0035(E598mln), $1.0100-10(E1.3bln), $1.0345-50(E571mln), $1.0380-00(E1.1bln)

- USD/JPY: Y138.00($816mln), Y140.30($765mln), Y141.15($600mln), Y150.00($1.4bln)

- AUD/USD: $0.6585-00(A$798mln)

- USD/CNY: Cny7.1500($1.1bln)

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/11/2022 | 0745/0845 | ** |  | FR | Manufacturing Sentiment |

| 24/11/2022 | 0830/0930 | ** |  | SE | Riksbank Interest Rate |

| 24/11/2022 | 0900/1000 | *** |  | DE | IFO Business Climate Index |

| 24/11/2022 | 0945/0945 |  | UK | BOE Ramsden Speech at BOE Watchers’ Conference | |

| 24/11/2022 | 1030/1030 | | UK | BOE Pill Panelist at BOE Watchers’ Conference | |

| 24/11/2022 | 1100/0600 | * |  | TR | Turkey Benchmark Rate |

| 24/11/2022 | 1115/1215 |  | EU | ECB de Guindos Speech at Analysis Forum in Milan | |

| 24/11/2022 | - |  | SK | South Korea BoK Rate Decision | |

| 24/11/2022 | - |  | ZA | SARB Rate Decision | |

| 24/11/2022 | 1300/1400 | | EU | ECB Schnabel Speech at BOE Watchers' Conference | |

| 24/11/2022 | 1330/0830 | * |  | CA | Payroll employment |

| 24/11/2022 | 1345/1345 | | UK | BOE Mann Panelist at BOE Watchers’ Conference | |

| 24/11/2022 | 1400/1500 | ** |  | BE | BNB Business Sentiment |

| 25/11/2022 | 2330/0830 |  | JP | Tokyo Nov CPI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.