EXECUTIVE SUMMARY

- BOWMAN SUPPORTS STEADY FED STANCE, WARNS OF UPSIDE RISKS - MNI

- US REGULATORS EYE SOFTER CAPITAL HIKE RULES FOR BANKS - WSJ

- IRAN PRESIDENT RAISI, FOREIGN MINISTER DEAD IN HELICOPTER CRASH - BBG

- JUNE CUT TO JGB BUYS POSSIBLE FOR BOJ - SAKURAI - MNI INTERVIEW

- CHINA’S MAY LOAN PRIME RATE UNCHANGED - MNI BRIEF

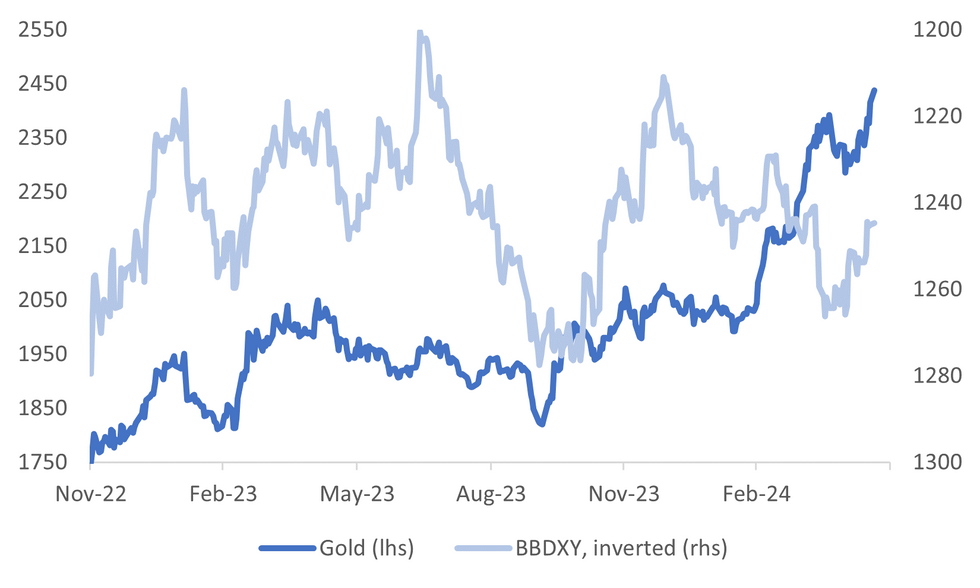

Fig. 1: Gold To Fresh Record Highs

Source: MNI - Market News/Bloomberg

UK

HOUSE PRICES (BBG): Rightmove report UK May house prices +0.8% m/m, +0.6% y/y to £375,131.

EUROPE

UKRAINE (ECONOMIST): Volodymyr Zelensky has had a testing first term as president of Ukraine. But Mr Zelensky may soon face his biggest political challenge yet. His term ends on Monday and he will struggle to refresh his mandate with no obvious possibility of elections. Recent polling shows that trust in the presidency has fallen from a net positive of 71% in 2023 to 26%.

UKRAINE (BBC): Ukrainian President Volodymyr Zelensky says Russia could increase its attacks in Ukraine's north east following its recent gains near the city of Kharkiv.

UKRAINE (POLITICO): Ukrainian President Volodymyr Zelenskyy rejected a call by French President Emmanuel Macron for a truce in the Ukraine-Russia war during the Summer Olympic Games in Paris.

UKRAINE (BBC): Russia is currently not seeking to capture Ukraine's second-largest city of Kharkiv, President Vladimir Putin has claimed. But he stressed that Russian forces were advancing in the north-eastern Kharkiv region to create a "security zone" for Russia's border region.

POLAND (POLITICO): Poland plans to invest €2.3 billion to bolster security along its eastern border with Russia and Belarus, Prime Minister Donald Tusk announced on Saturday.

SLOVAKIA (BBC): The man suspected of attempting to assassinate Prime Minister Robert Fico may not have been working alone, Slovakia's interior minister says. Mr Fico’s life is no longer in danger following hours of surgery, but the 59-year-old still requires intensive care, his deputy said earlier.

U.S.

FED (MNI): Federal Reserve Governor Michelle Bowman Friday reiterated her preference for keeping interest rates steady to allow restrictive policy to bring inflation down, adding she remains open to raising borrowing costs should data indicate progress on inflation has stalled.

BANKS (WSJ): US federal regulators are mulling a new plan which would lower a nearly 20% proposed compulsory capital increase for the country’s biggest lenders, the Wall Street Journal reported on Sunday.

OTHER

IRAN (BBG): Iranian President Ebrahim Raisi has been killed in a helicopter crash in a mountainous area of the country. Rescuers on Monday found the helicopter that had been carrying the president and other officials including Foreign Minister Hossein Amirabdollahian, who also died, the semi-official Mehr news agency reported. It crashed on Sunday near Tavil village in northwest Iran.

JAPAN (MNI INTERVIEW): The Bank of Japan could reduce its purchases of government bonds from about JPY6 trillion per month to around JPY5 trillion by as early as June but it is likely to keep its policy interest rate unchanged at a range of zero percent to 0.1% until at least July given the contraction in first quarter GDP and the lack of immediate justification for a hike from price data, a former BOJ board member told MNI.

JAPAN/CHINA (NIPPON TELEVISION): Liu Jianchao, who heads the Communist Party of China’s diplomatic arm, is set to visit Japan as soon as May 27, to meet with government leaders, Nippon Television reported, citing people familiar with the two nations’ diplomatic relations it didn’t identify.

SAUDIA ARABIA/JAPAN (BBG): Saudi Arabia’s Crown Prince Mohammed bin Salman postponed a planned four-day trip to Japan due to concerns over the king’s health, Japan’s top government spokesman Yoshimasa Hayashi said.

ISRAEL (BBG): It certainly appeared crucial. Benny Gantz, ramrod straight and facing the cameras with gravity, told Prime Minister Benjamin Netanyahu to shift course on the Gaza war or he’d quit the three-man war cabinet. Israel, he said, needs “a government that will win the people’s trust.”

HONG KONG (MING PAO): Hong Kong will delay its plans to open up trading during the most severe weather in order to offer adequate time to let industry players prepare, local media outlet Ming Pao reports, citing unidentified people.

COMMODITIES (BBG): Copper surged to a fresh record, extending a months-long rally that’s been driven by financial investors who have piled into the market in anticipation of supply shortages.

NEW ZEALAND (BBG): Shadow Board members recommended the Reserve Bank keep the Official Cash Rate at 5.5% this week, the New Zealand Institute of Economic Research says Monday in Wellington.

CHINA

HOUSING (SECURITIES TIMES): - Chinese developers’ sales centers saw a surge of visits by homebuyers over the weekend, after the authorities announced property support measures on Friday, the Securities Times reports.

HOUSING (YICAI): China’s plan for local governments to purchase properties and convert them into affordable housing faces the test of profitability as rental returns in most cities stand at around 2%, Yicai reports, citing China Real Estate Information Corp.

MORTGAGE RATES (FINANCIAL NEWS): China’s mortgage interest rates are expected to fall “significantly” after recent removal of rate floor, releasing housing demand and alleviating funding pressure on real estate developers, according to a front-page report in PBOC-backed newspaper Financial News, citing analysts.

LPR (MNI BRIEF): China's Loan Prime Rate remained unchanged on Monday according to a People's Bank of China statement, in line with market expectation as the drop in market rates and efforts to curb idle funds in the financial system restrained rate cut chances.

CHINA MARKETS

PBOC net drains CNY2 bln via Omo Mon; rates unchanged

The People's Bank of China (PBOC) conducted CNY2 billion via 7-day reverse repo on Monday, with the rates unchanged at 1.80%. The operation has led to a net drain of CNY2 billion after offsetting the CNY4 billion maturity today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8000% at 09:27 am local time from the close of 1.8078% on Friday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 48 on Friday, compared with the close of 49 on Thursday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1042 on Monday, compared with 7.1045 set on Friday. The fixing was estimated at 7.2158 by Bloomberg survey today.

MARKET DATA

UK MAY RIGHTMOVE HOUSE PRICES RISE 0.8% M/M; PRIOR +1.1%

UK MAY RIGHTMOVE HOUSE PRICES RISE 0.6% Y/Y; PRIOR +1.7%

JAPAN MAR TERTIARY INDUSTRY INDEX M/M -2.4%; MEDIAN -0.1%; PRIOR 2.2%

MARKETS

US TSYS: Treasury Futures Little Changed, Busy Day Ahead For Fed Speakers

- Treasury futures are little changed today with the 10Y contract now (+ 00+) at 109-06+, the contract made highs of 109-09 and lows of 109-05, while the 2Y contract is (+ 00.375) at 101-22.75

- The treasury curve is little changed today with yields were flat to 1bps lower, the 2Y yield -0.7bps at 4.818%, 10Y -0.8bps to 4.412%.

- Tsys Flows today: A 20k likely buyer of TYM4 110 calls, 0.03 at 10:24:49 AEST, and a block seller of 1,800 FVM4 105-29.25

- Across local rate markets: ACGBs yields are 2-3bps higher, curve slightly steeper, NZGBS 1-2bps higher, curve steeper, while JGBs 1-4bps higher with the 10y yield rising to 0.975% for the first time since 2013

- Rate cut projections remain largely in-line with this morning's levels (*): June 2024 at -10% w/ cumulative rate cut -2.5bp at 5.313%, July'24 at -22% w/ cumulative at -8bp at 5.258%, Sep'24 cumulative -21.1bp, Nov'24 cumulative -29.2bp, Dec'24 -44.4bp

- Today, there is little on teh data calendar with markets focusing on Fed speakers including Raphael Bostic, Christopher Waller, Philip Jefferson, Loretta Mester and Michael Barr.

JGBS: Solid Demand At Linker Auction, 10yr Yield At Highest Levels Since 2013

JGB futures got to lows of 143.78 post the lunchtime break, but we have since stabilized somewhat. JBM4 was last around 143.81, -.26, generally maintaining a downside bias in the first part of trade today.

- Downside focus will be on recent lows near 143.70. There has been little spill over from US Tsys today, with 10yr futures largely tracking sideways.

- The 10yr linker auction drew a strong bid to cover ratio of 4.27 (the highest since 2007). The broader backdrop is also focused on the BoJ outlook, with the latest MNI interview with an ex BoJ official noting we could see a cut to BoJ bond purchases at the June meeting (see this link).

- Cash JGB yields remain on the front foot, with the 10yr up to 0.975%, fresh highs going back to 2013. We continue to see firmer yield gains at the back end of the curve, the 20-40yr tenors seeing yield gains of around 3bps. The 10yr swap rate is back near 1.025.

- Tomorrow the data calendar is relatively light.

AUSSIE BONDS: ACGBs Cheaper, Curve Steepens, RBA Minutes Tomorrow

ACGBs (YM -2.0 & XM -2.0) are cheaper today, it was a slow and uneventful day with no local headlines or data out. Looking ahead tomorrow we have Westpac Consumer Confidence for May due out and the RBA minutes of May policy meeting.

- Cross-asset moves: Equities are higher today, ASX200 is up 0.64%, while US equity futures are current about 0.15% higher. In FX the BBDXY is little changed today with the AUD is up about 0.20%, while Iron Ore was up 0.89% at $118.25/ton

- US treasury futures are slightly higher in Asia trading, the 10Y contract is (+ 01) at 109-07, after earlier making highs of 109-09, while volumes are on the low side, yields are about 1bp lower across the curve. In tsys flows there was earlier a block seller of FV, and a likely buyer of 20k TY Jun 24 110 calls.

- The ACGB curve has bear-steepened today with the 2y10y +0.340 at 30.110, yields are 1-3bps higher, while the AU-US 10-year yield differential is 3bps higher today at -18bps

- Swap rates are are 1-2bps lower today

- The bills strip is flat to 1bps lower.

- RBA-dated OIS implied rate is little changed this morning with 18bps of easing into the year-end to a terminal rate of 4.17%

- Looking ahead, Westpac Consumer Conf & RBA Minutes

NZGBS: Cheaper, RBNZ Survey Shows Household Inflation Expectation Falls

NZGBs are flat to 1.5bps cheaper today, the curve has bear steepened. It has been a slow day, RBNZ published Q2 household expectations survey earlier with the two-year inflation expectation now at 3% down from 3.2% in Q1, otherwise the market will be waiting for the RBNZ rate decision on Wednesday were they are widely expected to keep rates on hold.

- US treasury futures are slightly higher in Asia trading, the 10Y contract is (+ 01) at 109-07, after earlier making highs of 109-09, while volumes are on the low side, yields are about 1bp lower across the curve. In tsys flows there was earlier a block seller of FV, and a likely buyer of 20k TY Jun 24 110 calls.

- The NZGB curve is steeper, but trading near session best at the moment, the 2Y +0.5bps at 4.674%, 10Y is +1.0bps at 4.596%.

- Earlier, The RBNZ's 2Q household expectations survey shows a decrease in the median expected inflation rate for the next two years to 3% from 3.2% in 1Q, and for the next year to 4% from 5%. The median expected inflation in five years remains at 3%. The mean expected inflation in two years is unchanged at 3.6%. Additionally, 52% of respondents expect higher house prices, with the median expected house price inflation in one year at 0%.

- Swap rates are flat to 1bps lower

- RBNZ dated OIS is slightly today today down 2bps heading into year-end with cumulative 47bps of easing now.

- Looking Ahead: RBNZ on Wednesday

FOREX: A$ Outperforms On Higher Metals, Steady Trends Elsewhere

The BBDXY USD index sits a touch under end levels from last week, last around 1244.80/85. Overall trends have been fairly muted in the FX space in Monday trade to date.

- AUD/USD has outperformed marginally, up around 0.20%. Commodity prices remain favorable from a metals standpoint, with copper hitting a fresh record high. Regional equity sentiment is mostly positive as well.

- US equity futures are marginally higher as well, while US yields are down a touch, losses are close to 1bps at this stage.

- AUD/JPY is tracking higher, last near 104.45. We aren't too far away from late April highs of 104.94.

- USD/JPY has risen a touch but hasn't broken back above 156.00 (the pair last 155.75/80).

- NZD/USD is down a touch to 0.6125/30. A Q2 RBNZ survey of inflation expectations showed households saw a slightly lower median expected inflation rate for the next two years at 3% from 3.2% in 1Q. The RBNZ meeting on Wednesday is expected to be unchanged.

- Later the Fed’s Bostic, Barr, Waller, Jefferson and Mester speak. There are no data of note.

ASIA STOCKS: HK & China Equities Head Higher, Property Off Morning Lows

Hong Kong & Chinese equities have opened higher today, the main focus today has been on the property space after the Chinese government announced new measures to support the sectors on Friday, however many analysts have mixed views on how much the recent announcements will do to help the struggling sector, while China EV makers are taking longer than ever before to pay their suppliers. Earlier, China left the 1 & 5yr LPRs unchanged.

- Hong Kong equities are mostly higher today, property indices initially opening lower with the HS Property Index opening down 1.40% however has recovered to now trade up 0.95%, while he Mainland Property Index now trades unchanged for the day. The HSTech Index is up 0.60%, while the HSI is up 0.50%. In China onshore markets, the CSI300 is trading up 0.20% while the the small-cap CSI1000 Index, up 0.30% and the ChiNext is up 0.21%.

- On Friday, The Chinese government announced a comprehensive support package to revive its struggling property market, including relaxed mortgage rules and encouraging local governments to purchase unsold homes. This move aims to mitigate the sector's impact on economic growth. The measures include lower down-payment requirements, central bank funding, and various incentives to stabilize the market. However, there are concerns about whether these measures will be sufficient to address the deep-rooted issues within the property sector and stimulate long-term demand.

- China's electric car market is facing significant stress, with companies like Nio and Xpeng taking much longer to pay suppliers due to sluggish economic growth, reduced demand, and intense price wars. This delay is impacting auto-parts suppliers, increasing their receivables and reducing cash reserves, potentially leading to a "messy consolidation" as weaker suppliers face bankruptcy, per bbg.

- Looking ahead, quiet week for China on the data front, Hong Kong has Unemployment Rate later today

ASIA PAC STOCKS: Equities Head Higher, Miners Top Performers On Strong Metal Prices

Asian markets are higher today, boosted by China property market and US equities climbing to fresh highs on Friday thanks to strong earnings, the MSCI Asia Pacific is on track for its seventh straight day of gains and is currently up about 0.70%, with mining stocks rallying on strong commodity prices. It has been a relatively quiet session, very little in the way of economic data.

- Japan equities are higher today, materials stocks are higher as copper and oil continue to rise. Semiconductor names are slightly lower after the Philadelphia SE Semiconductor Index fell on Friday ahead of Nvidia earnings due out later this week. The Nikkei 225 is up 0.89% and is closing back in on the 40,000 mark, while the Topix is up 0.77%.

- South Korean equities are higher today as the Kospi edges closer to the year-to-date highs up 0.63%, Samsung and SK Hynix hare the top performers, small caps are underperforming today with the Kosdaq down 1.24%

- Taiwan equities are lower today, with the Taiex down about 0.45% with TSMC is the biggest drag on the index after the Philadelphia SE Semiconductor Index traded lower on Friday. We have Export orders due out a bit later today and Industrial Production on Thursday.

- Australian equities are higher today led by mining and energy stocks, the moves are largely tracking US equities from Friday as well as China taking steps to support their local property market. The ASX200 is up 0.68%

- Elsewhere in SEA, New Zealand equities are up 0.14%, Indonesian equities are up 0.18%, Philippines equities are up 0.94%, Malaysian equities are up 0.76%, Indian equities are up 0.16%.

OIL: Crude Little Changed Today Despite Geopolitical Events

Oil prices are slightly higher during APAC trading today as the risk tone remains favourable. Brent is up 0.2% to $84.12/bbl after a high of $84.30. WTI is 0.1% higher at $79.65/bbl after reaching $79.83. Supply risks remain the focus with instability in Russia/Ukraine and the Middle East. The USD index is slightly lower.

- The crash site of Iran’s President Raisi’s helicopter has been found and he and the foreign minister were killed. There is concern that his death could leave a power vacuum and destabilise the world’s third largest oil producer, but Ayatollah Ali Khamenei said that there “won’t be any disruption to the country’s affairs”.

- Over the weekend an oil tanker was hit by Houthis off the coast of Yemen and Ukraine struck Russia’s Slavyansk refinery again causing operations to cease. It refines 80kbd. But there has been little reaction in APAC trading.

- Money managers’ net long crude positions fell for a second straight week, according to Bloomberg.

- Later the Fed’s Bostic, Barr, Waller, Jefferson and Mester speak. There are no data of note.

GOLD: Fresh Record Highs

Bullion touched a fresh record high in the first part of Asia Pac trade. We got to $2440.59, but sit slightly lower now, last near $2438. We are still up 0.90% on Friday levels and this follows a +2.3% gain for gold last week.

- Broader USD sentiment has been relatively steady so far today, with the BBDXY index little changed near 1245. Still, some risk aversion may be creeping into markets given the on-going Israel-Hamas conflict and the reports of the death of the Iranian President and Foreign Minister in a helicopter crash.

- There are no reports of external involvement in the crash, with US Senator Chuck Schumer stating US intelligence agencies indicated there was no evidence of foul play. We broader tensions in the region still elevated though, the news may have lent some support to gold today.

- Broader commodity sentiment is positive in the metals space today, with copper continuing to track higher.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 19/05/2024 | 1930/1530 |  | US | Fed Chair Jerome Powell | |

| 20/05/2024 | 0600/0800 | ** |  | DE | PPI |

| 20/05/2024 | 0900/1000 |  | UK | BOE's Broadbent Monetary Mechanism Workshop | |

| 20/05/2024 | - | | UK | DMO to hold quarterly consultation investors / GEMM consultation | |

| 20/05/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 20/05/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 21/05/2024 | 0130/1130 |  | AU | RBA Minutes | |

| 21/05/2024 | 0800/1000 | ** |  | EU | Current Account |

| 21/05/2024 | 0900/1100 | ** | | EU | Construction Production |

| 21/05/2024 | 0900/1100 | * | | EU | Trade Balance |

| 21/05/2024 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 21/05/2024 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 21/05/2024 | 1230/0830 | *** |  | CA | CPI |

| 21/05/2024 | 1230/0830 | ** | | US | Philadelphia Fed Nonmanufacturing Index |

| 21/05/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 21/05/2024 | 1300/0900 | | US | Fed Governor Christopher Waller | |

| 21/05/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 21/05/2024 | 1700/1800 | | UK | BOE's Bailey Lecture at LSE | |

| 21/05/2024 | 2300/1900 | | US | Atlanta Fed's Raphael Bostic | |

| 21/05/2024 | 2300/1900 | | US | Cleveland Fed President Loretta Mester |