Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- CHINA-US FACE CHALLENGES DESPITE THAW - EXPERT - MNI

- YELLEN CHINA VISIT SEEKS TO CREATE MORE TALKS AMID TENSIONS - BBG

- CHINESE RUSH TO BUY HK INSURANCE, DOLLARS AS CONFIDENCE CRACKS, YUAN WEAKENS - RTRS

- OVER A THIRD OF UK HOMES DROPPED IN VALUE IN THE LAST SIX MONTHS - BBG

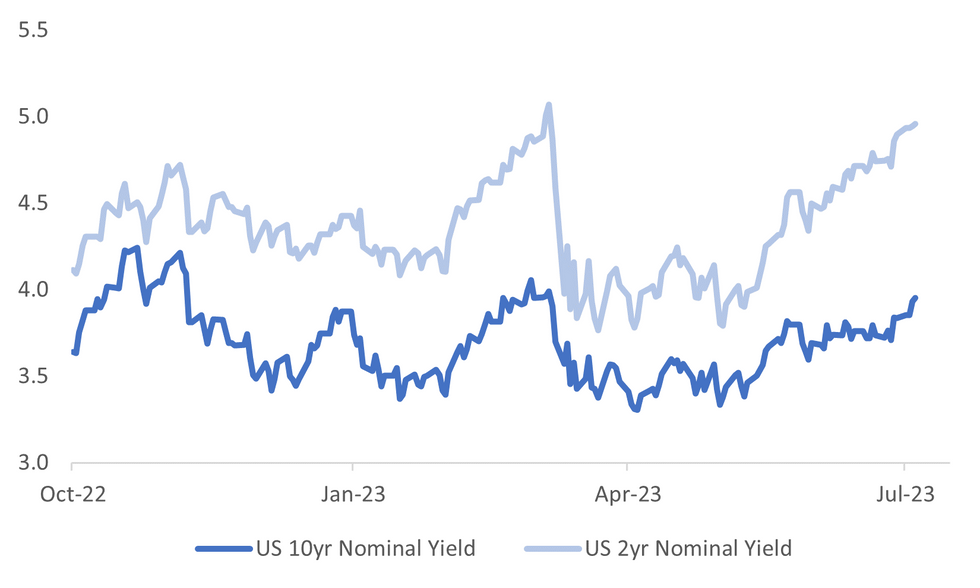

Fig. 1: US 2yr & 10yr Nominal Government Bond Yields

Source: MNI - Market News/Bloomberg

U.K.

PROPERTY: More than 11 million UK homes have declined in value since the end of last year, as pricey mortgages wreak havoc on the nation’s real estate market. Some 38% of homes lost at least 1% in value between November and May, according to estimates from property portal Zoopla. These properties lost an average of £7,700 ($9,788). It’s up from 18% of homes losing value in the 12 months to May, suggesting the impact of rising rates is starting to weigh on prices. (BBG)

REGULATION: The UK’s financial services regulator has said asset managers are putting investors at risk by not adequately monitoring the liquidity of their funds. Many mutual fund houses did not properly use their liquidity management tools and failed to understand the risks of less liquid assets held in their portfolios, the Financial Conduct Authority said following a multi-firm review. (BBG)

BOE: Two former Bank of England officials said the central bank was too slow to spot the signs of inflation's post-pandemic surge, adding to pressure on the BoE which is battling the fastest price growth of the world's big rich economies. Former Deputy Governor Charlie Bean and Sushil Wadhwani, who also sat on the Monetary Policy Committee, pointed to the BoE's decision to stick with its huge bond-buying even when there were signs of an economic rebound from the COVID-19 lockdowns. (RTRS)

EUROPE

ECB: The race to succeed Andrea Enria as the head of the European Central Bank’s oversight arm has narrowed to two female candidates, according to people familiar with the matter. Bundesbank Vice President Claudia Buch and Bank of Spain Deputy Governor Margarita Delgado are the only names on a shortlist that the ECB Governing Council is sending to European Parliament lawmakers on Wednesday, the people said. They declined to be identified because talks on the matter are confidential. (BBG)U.S.

US/CHINA: US Treasury Secretary Janet Yellen visits China this week with the goal of finding areas of common economic ground and opening communication channels amid an increasingly turbulent relationship between the world’s two biggest economies. It will be the first major test of a policy she outlined in April that’s geared toward defending and securing US national security without trying to hold China back economically. (BBG)

US/CHINA: The United States "firmly" opposes export controls announced by China on gallium and germanium, metals needed to produce semiconductors and other electronics, a U.S. Commerce Department spokesperson said on Wednesday, adding that Washington will consult its partners and allies to address the issue. (RTRS)

OTHER

AUSTRALIA: Australia's central bank will likely deliver a 25 basis point interest rate increase on Aug. 1 following a pause on Tuesday according to economists in a snap who were split on when and where the cost of borrowing would peak. (RTRS)

AUSTRALIA: After a lifetime dedicated to helping steer Australia through economic uncertainty, the governor of the Reserve Bank of Australia, Philip Lowe, will be by now reading the room and preparing for his exit. With Treasurer Jim Chalmers set to announce a new central bank head within days, Lowe isn't expected to see his current seven-year term extended beyond September. (Dow Jones)

SOUTH KOREA: Samsung Electronics June-quarter profit is expected to plunge 96% on-year to the lowest for any quarter in more than 14 years, as a chip glut continues to drive large losses in the tech giant's cash cow business despite a supply cut. (RTRS)

CHINA

US/CHINA: MNI (Beijing) - The inclusion of the U.S. within the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) could temper its intensifying regional rivalry with China, however, the relationship faces challenges, despite a recent flurry of high-profile visits, a leading Chinese international relations advisor told MNI. While U.S. Treasury Secretary Janet Yellen’s visit to Beijing this week represents something of a thaw following Secretary of State Antony Blinken’s meeting with President Xi Jinping and foreign minister Qin Gang in June, the upcoming U.S. presidential election could stifle reconciliation as candidates' campaign on anti-China issues, according to Professor Wang Yiwei, director at Renmin University's Institute of International Affairs. (MNI)

YUAN: Chinese investors are rushing offshore to make dollar deposits and buy Hong Kong insurance in a signal domestic confidence is languishing and that the ailing yuan faces more pressure. The outflows highlight deep-seated concern about the state of China's economy as its much-awaited pandemic recovery stalls. Consumer spending is flagging, the property market and stock markets are in the doldrums and cash is piling up in savings. (RTRS)

YUAN: The yuan could gradually stabilise or appreciate against the U.S. dollar, should market expectations on the Chinese economy improve and the USD index weakens as the US economy slows, said Ming Ming, chief economist of CITIC Securities. The central bank has plenty of policy tools to deal with large FX fluctuations, including raising the FX risk reserve ratio or the deposit reserve ratio, as well as using central bank bills in the offshore market and restarting countercyclical factors, said analysts from Donghai Securities. The yuan began to rebound this week after approaching the CNY7.3 mark against USD. (Yicai)

INFLATION: China’s National Bureau of Statistics expects June’s CPI data to remain unchanged from May’s 0.2% y/y increase, according to Yicai. The news outlet noted pork prices, a key component of CPI, have dragged down inflation this year as producers increased slaughter due to swine flu and faced lower than expected consumer demand. The NDRC began a new round of pork purchasing to increase national reserves and stabilise prices. Wu Chaoming, deputy director of the Caixin Research Institute, said CPI in June will remain below 1% y/y, reflecting insufficient domestic demand and slow recovery of household income. (Yicai)

POLICY: Structural tools may be used again and be key in the next phase of policy support, while there may be more caution toward cutting rates, according to a report in Shanghai Securities News, citing analysts. China will be prudent toward using pricing tools such as rate cuts, which might be better timed at year-end when US rate hikes come to an end considering impact on yuan: Lian Ping, chief economist, Zhixin Investment. (Securities News).

TRADE: China’s recent export control on gallium and germanium is “just the beginning,” state media China Daily reports, citing Wei Jianguo, former vice-minister of commerce. China has more tools for countermeasures if the US plans to impose tougher technology restrictions on Beijing, the report adds, citing Wei in an interview. (BBG)

MARKETS: Chinese banks have stopped buying bonds issued in the Shanghai free trade zone after regulators increased scrutiny of the $18 billion market mostly used by the nation’s local government financing vehicles, according to people familiar with the matter. (BBG)

CHINA MARKETS

PBOC Drains Net CNY191 Bln Via OMOs Thursday

The People's Bank of China (PBOC) conducted CNY2 billion via 7-day reverse repos on Thursday, with the rates at 1.90%. The operation has led to a net drain of CNY191 billion after offsetting the maturity of CNY193 billion reverse repo today, according to Wind Information.

- The operation aims to keep banking system liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.8214% at 09:24 am local time from the close of 1.7842% on Wednesday.

- The CFETS-NEX money-market sentiment index closed at 45 on Wednesday, compared with the close of 38 on Tuesday.

PBOC Yuan Parity Lower At 7.2098 Thursday VS 7.1968 Wednesday.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.2098 on Thursday, compared with 7.1968 set on Wednesday. The fixing was estimated at 7.2458 by BBG survey today.

OVERNIGHT DATA

AU MAY EXPORTS M/M 4%; PRIOR -6%

AU MAY IMPORTS M/M 2%; PRIOR 2%

AU MAY TRADE BALANCE A$11791mn; MEDIAN A$10900mn; PRIOR A$ A$10454mn

JAPAN JUNE TOKYO AVG OFFICE VACANCIES 6.48; PRIOR 6.16

MARKETS

US TSYS: Marginally Cheaper In Asia

TYU3 deals at 111-09, -0-02+, a 0-09 range has been observed on volume of ~97k.

- Cash tsys sit 1-2bps cheaper across the major benchmarks, the belly leads the cheaps.

- Tsys have been pressured through the Asia-Pac session, the move came alongside a cheapening in ACGBs and NZGBs which spilled over into the wider space.

- TY broke Wednesday's lows before marginally paring losses, the next support level comes in at 110-27+ the low from Mar 2 and key support.

- Regional Equities and US Equity Futures are lower, with the USD and Yen firming as risk off flows escalated through the session.

- In Europe today German Factory Orders provides the highlight. Further out we have ADP Employment and ISM Services. Fedspeak from Dallas Fed President Logan crosses.

JGBS: Futures At Cheaps After Relatively Poor Digestion Of 30-Year Supply

JGB futures are dealing on a negative note, -23 compared to the settlement levels, as they push to Tokyo session lows after today’s 30-year supply exhibits weaker-than-expected demand.

- 30-year supply sees relatively poor digestion as the low price fails to meet dealer expectations and the cover ratio declines to its lowest level since March. The auction tail was also significantly longer than the past auction, rising to the highest level since Apr-2020.

- Apart from the previously mentioned international investment flow data, which revealed offshore buying of Japanese bonds and increased Japanese buying of offshore bonds, there have been few notable domestic drivers to highlight.

- Cash JGBs are dealing cheaper in the Tokyo afternoon session with yield movements ranging from flat (1-year) to +1.9bp (7-10-year). The benchmark 30-year yield sits at 1.219%, 1.7bp higher than lunch break levels.

- The swaps curve bear steepens with rates 0.7-1.9bp higher. Swap spreads are wider apart from the 7-10-year zone.

- Tomorrow the local calendar sees May’s Real Cash Earnings, Labour Cash Earnings and Household Spending data along with the Leading and Coincident Indicators.

- Later today, attention turns to ADP employment data, ahead of Non-Farm Payrolls on Friday. The US calendar also sees Trade Balance, ISM Non-Mfg, S&P Global Services PMI, Weekly Initial Jobless Claims and JOLTS data.

AUSSIE BONDS: Tracking US Tsys Cheaper

ACGBs are dealing on a negative note (YM -12.0 & XM -11.5), following the weakening trend observed during the Sydney session. Without domestic catalysts, local participants appear to have been guided by US tsys, which have continued their cheapening from the NY session.

- Cash ACGBs are 11bp cheaper with the AU-US 10-year yield differential unchanged at +16bp.

- Swap rates are 11-12bp higher with EFPs slightly wider.

- Bills strip bear steepens with pricing -2 to -16.

- RBA dated OIS pricing is 8-12bp firmer for meetings beyond Nov'23 with Feb'24 leading.

- The local calendar remains light until Tuesday when we can expect the release of CBA Household Spending data for June, Westpac Consumer Sentiment for July, and NAB Business Confidence for June. Additionally, on Wednesday, market attention will be focused on Governor Lowe's speech, as investors hope to gain insights into the central bank's level of concern regarding inflation.

- Later today, attention turns to ADP employment data, ahead of Non-Farm Payrolls on Friday. ADP Employment Change: 225k est vs. 278k prior. The US calendar also sees May Trade Balance, June ISM Non-Mfg, June S&P Global Services PMI, Weekly Initial Jobless Claims and May JOLTS.

NZGBS: Cheaper, Outperforms The $-Bloc, Syndicated Tap Of Apr-33 Bond

NZGBs closed weaker but off cheaps with benchmark yields 5-6bp higher after the NZ Treasury sells an additional NZ$5.0bn of the nominal 14 April 2033 bond via syndicated tap. The bonds, which carry a coupon of 3.50%, were issued at a spread of 4bp over the 15 May 2032 nominal bond, at a yield to maturity of 4.7575%. Total book size, at final price guidance, exceeded NZ$12.2bn. Today’s tap led to the cancellation of the scheduled tender.

- The cash line richened 2.5bp in post-tap trade, more than unwinding the pre-announcement cheapening.

- While pressured by US tsys and ACGBs in local trade, NZGBs have outperformed with the NZ/US and the NZ/AU 10-year yield differentials respectively 5bp and 7bp tighter.

- Swap rates closed 5-10bp higher with the 2s10s curve steeper and implied swap spreads wider.

- RBNZ dated OIS pricing closed 6-8bp firmer for meetings beyond Nov'23.

- (AFR) While the RBNZ is widely viewed as having reached its interest rate peak, the central bank increasingly is expected to hold the cash rate at its current level well into next year, perhaps even until mid-2024. (See link)

- The local calendar is light tomorrow with the focus turning to the RBNZ policy decision on Wednesday.

FOREX: Yen Firms In Asia

The Yen is firmer in Asia, despite US Tsy Yields ticking high, as weaker regional equities and US equity futures weigh on sentiment.

- USD/JPY is now dealing at session lows a touch above the ¥144 handle, the pair is down ~0.3%. Support comes in at ¥143.29, low from 27 June.

- AUD is down ~0.2%, and last prints at $0.6640/45. Support comes in at $0.6596, low from June 29 and bear trigger. Australia's Trade Surplus in May was stronger than expected printing at $11.179bn vs $10.90bn exp.

- Kiwi is also pressured as the waning risk sentiment weighs. NZD/USD prints at $0.6160/65, the pair is ~0.2% lower. The 20-Day EMA ($0.6153) provides the next technical support level.

- Elsewhere in the G-10 space, EUR is down ~0.2%. The Scandies are under pressure, NOK is down ~0.2% and SEK is down ~0.4%, however liquidity is generally poor in Asia.

- Cross asset wise; E-minis are down ~0.4% and Hang Seng is down ~3%. BBDXY is ~0.1% firmer. 10 Year US Tsy Yields are up 2bps.

- Looking ahead in Europe today we have German Factory Orders, further out a slew of US data crosses including ADP Employment, Initial Jobless Claims and ISM Services.

EQUITIES: Most Asia Pac Markets Down, Hong Kong Shares Off By -3%

Regional equities are by and large in the red. Losses have been largest for Hong Kong stocks. The HSI off by over 3% at this stage, amid multiple headwinds. Japan stocks are also weaker. US futures are tracking lower at this stage, with losses moderately accelerating in the Asia Pac afternoon session. Eminis were last -0.35% around 4468. This is fairly close to Wednesday session lows. Broader sentiment has been weighed by higher US yields, post the FOMC minutes from Wednesday.

- The HSI is off by a little over 3% at this stage. Property woes are weighing, with recent trading halts in bonds for state back Sino-Ocean cited as one factor. The tech sub index is also down, off by close to 2.4% at this stage. The HS China Enterprise index is also down sharply, off by 3.55%, with China banks suffering.

- The authorities are also reportedly halting China banks from buying free-trade zone bonds, which is expected to impact LGFVs.

- Japan stocks are also weaker, with the Nikkei 225 down by 1.80% at this stage. Weakness is evident in tech related plays, while Daiwa notes that ETF managers may sell shares to pay for dividends.

- The Kospi is down by near 0.90% at this stage, but the Taiex is faring worse, off by 1.60%, following a sharp pull back in the SOX during Wednesday trade.

- In SEA, only Indonesian stocks are higher at this stage, but gains are modest. Elsewhere losses are generally under 1%.

OIL: Crude Off Highs As Soft Risk Appetite Weighs

Oil prices are holding onto most of yesterday’s gains with WTI down to $71.68/bbl but Brent down 0.4% to $76.38. Crude rose in early APAC trading but has fallen with weak risk appetite driving equity markets across the region lower (Hang Seng down 3.1%). Minutes showed that most FOMC members think rates will need to rise further. The USD index is 0.1% higher and off the day’s lows.

- WTI reached an intraday high of $72.06 earlier but hasn’t been able to sustain moves above $72. It is currently close to the low of $71.64. Brent’s high was $76.82 and it is now trading close to intraday lows. Friday’s June payroll data will be a key input into the Fed and thus oil outlook.

- EIA US inventories are released today. Last week they were their lowest for nearly 6 months. Bloomberg reported that US API crude stocks fell another 4.38mn barrels in the latest week after -2.41mn according to sources familiar with the data. Gasoline rose 1.6mn and distillate 600k.

- Later the Fed’s Logan speaks. Also in the US, there are jobless claims, Challenger job cuts, JOLTS job openings, ADP employment and services ISM/PMI – all of which will be important guides to Friday’s payroll data. There is also US May trade.

GOLD: Pressured By 3-Month High In US Tsy 10-Year Yield

Gold is steady in Asia-Pac trading, after slumping 0.5% in the previous session, as higher US tsy yields pressured non-interest-bearing bullion. The 10-year US tsy yield finished 8bp higher at 3.93% after reaching a fresh 3-month high of 3.95%. This move largely came prior to the release of the FOMC minutes of the June meeting, which offered few surprises.

- There was little reaction to the release of the FOMC minutes of the June meeting. "Almost all participants noted that in their economic projections that they judged that additional increases in the target federal funds rate during 2023 would be appropriate," the report said. “Some participants indicated that they favoured raising the target range for the federal funds rate 25 basis points at this meeting or that they could have supported such a proposal.”

- A July hike from the Fed is close to fully priced (circa 22bp), though markets are more circumspect on the policy outlook thereafter, with a cumulative 33bp priced out to November.

- Attention now turns to employment data (ADP later today and Non-Farm Payrolls on Friday).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 06/07/2023 | 0600/0800 | ** |  | DE | Manufacturing Orders |

| 06/07/2023 | 0730/0930 | ** |  | EU | IHS Markit Final Eurozone Construction PMI |

| 06/07/2023 | 0830/0930 | ** |  | UK | IHS Markit/CIPS Construction PMI |

| 06/07/2023 | 0830/0930 | | UK | BOE DMP Survey | |

| 06/07/2023 | 0900/1100 | ** | | EU | Retail Sales |

| 06/07/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 06/07/2023 | 1215/0815 | *** | | US | ADP Employment Report |

| 06/07/2023 | 1230/0830 | ** | | US | Jobless Claims |

| 06/07/2023 | 1230/0830 | ** |  | CA | International Merchandise Trade (Trade Balance) |

| 06/07/2023 | 1230/0830 | ** | | US | Wholesale Trade |

| 06/07/2023 | 1245/0845 | | US | Dallas Fed's Lorie Logan | |

| 06/07/2023 | 1345/0945 | *** | | US | IHS Markit Services Index (final) |

| 06/07/2023 | 1400/1000 | *** | | US | ISM Non-Manufacturing Index |

| 06/07/2023 | 1400/1000 | ** | | US | JOLTS jobs opening level |

| 06/07/2023 | 1400/1000 | ** | | US | JOLTS quits Rate |

| 06/07/2023 | 1500/1100 | ** | | US | DOE Weekly Crude Oil Stocks |

| 06/07/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 06/07/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.