Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

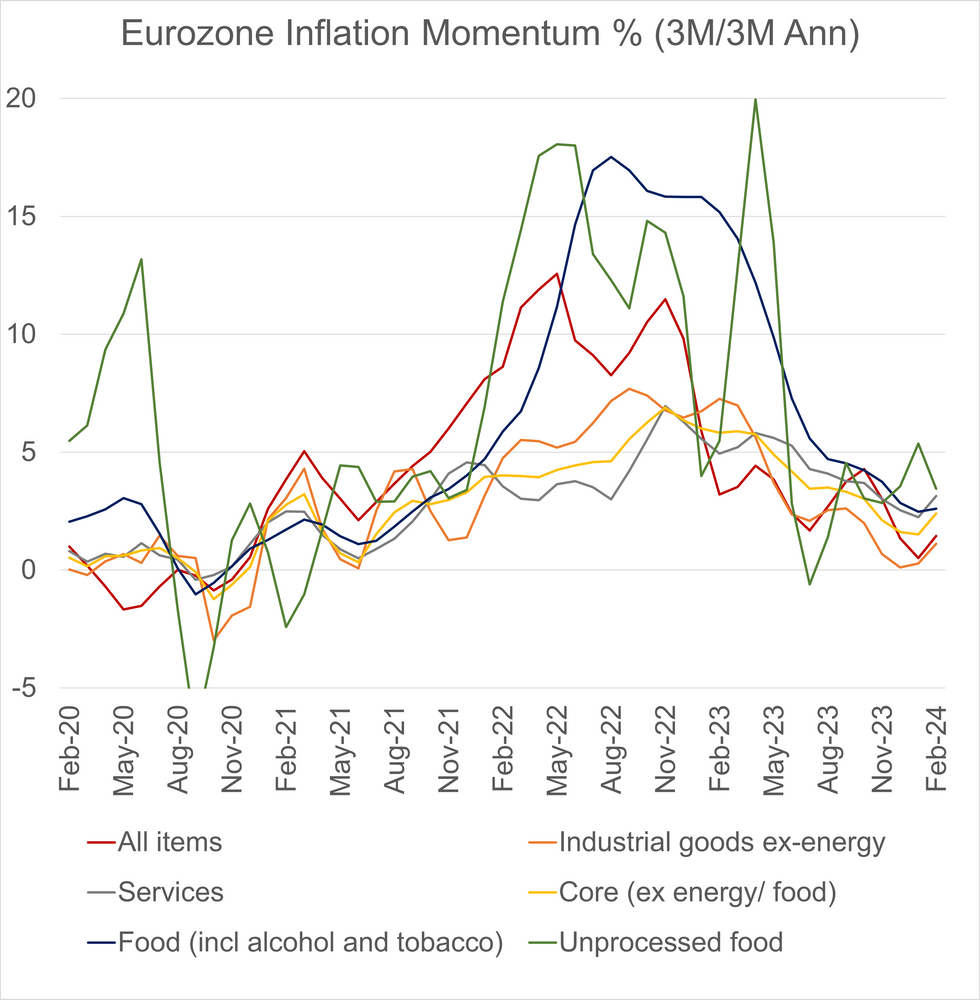

Services Stickiness Defies Expectations

- Eurozone flash inflation for February printed at an unrounded +2.58% Y/Y (vs +2.5% cons;+2.77% prior) while core (ex-energy/food) was +3.08% Y/Y (vs 2.9% cons; +3.27% prior).

- The main national releases in the lead-up to the Eurozone-wide print (France, Spain and Germany) came in firmer than expected on core measures, largely a result of stickiness in services. This led analysts to increase their estimates of the core EZ HICP rate to 3.0-3.2% Y/Y (from 2.9% previously).

- Overall, the stickiness in services inflation sets the scene for the upcoming ECB meeting (March 7), which features an updated set of macroeconomic projections.

- While the ECB's headline inflation forecast is likely to be revised lower (owing largely to lower natural gas prices), the same is not certain for core inflation, where disinflation progress has been slower than analyst projections (highlighted in the latest instance by the February flash print).

- Our review of February's preliminary Eurozone inflation data includes breakdowns and analysis of the national inflation prints and sell-side reactions.

FOR FULL PDF ANALYSIS:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok