Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE

We've just published our review of March's Eurozone flash inflation round - PDF here.

- Eurozone March flash headline and core inflation both printed below consensus on a rounded basis, but services stickiness continued to be a running theme in the road back to the ECB’s 2% target.

- Headline HICP was 2.4% Y/Y (vs 2.5/2.6% cons, 2.6% prior) and 0.8% M/M (vs 0.6% prior). Core HICP was 2.9% Y/Y (vs 3.0% cons, 3.1% prior), below 3% Y/Y for the first time since March 2022.

- The ECB’s seasonally adjusted data indicates that core and headline inflation momentum rose for the second consecutive month. However, sequential monthly inflation was lower than February across core categories.

- While some analysts have pointed to Easter-related calendar effects as a driver of the stickiness this month, others have noted that the “Easter effect” was not as large as expected coming into the release.

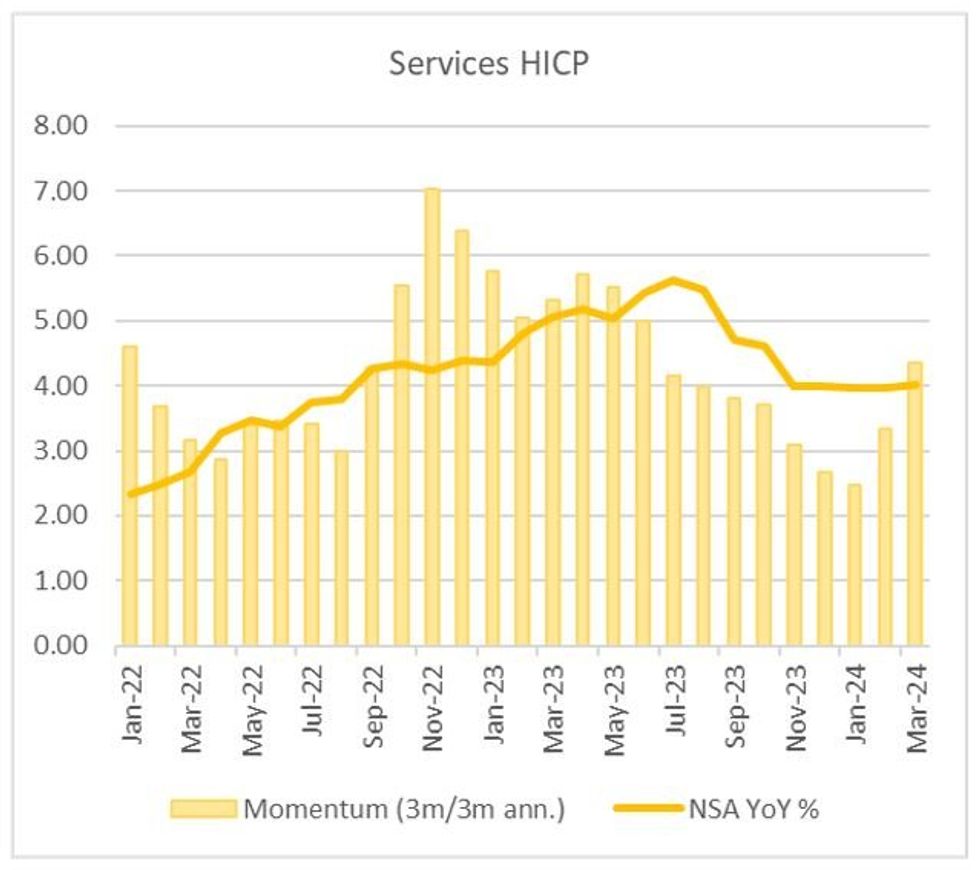

- While the annual core inflation rate has fallen in each of the last 8 months, recent progress has been only gradual, in large part due to services finding a seemingly firm floor at 4.0% Y/Y.

- In deciding whether to initiate rate cuts in June, these developments underscore the ECB’s need to analyse how labour costs are faring, due to their importance in service sector price setting behaviour.

- Our review of March's preliminary Eurozone inflation data includes breakdowns and analysis of the national inflation prints, and some sell-side reactions.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok