Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI Fed Preview - July 2024: September Signals In Spotlight

MNI Fed Preview - July 2024: September Signals In Spotlight

EXECUTIVE SUMMARY:

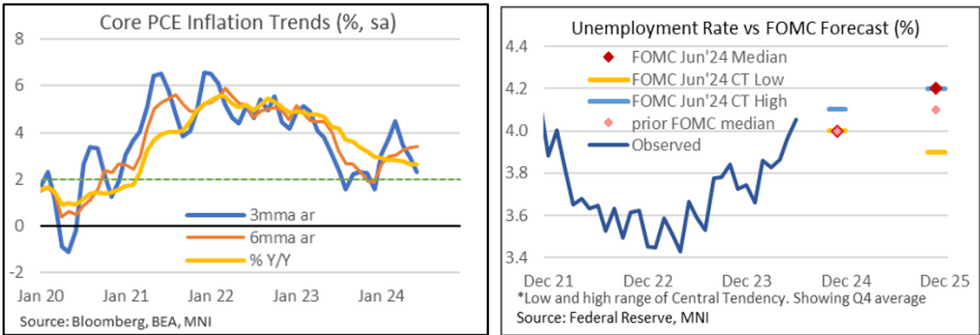

- The Fed will hold rates for an 8th consecutive meeting at its July meeting, putting immediate attention on any signals about rate cuts beginning in September.

- While inflation and the labor market cooled in the second quarter, providing a clear path to rate cuts by year-end, underlying demand has remained resilient in defiance of what FOMC officials see as “sufficiently restrictive” policy.

- With the lingering memory of various data "head fakes" in mind on both the upside and downside of the inflation and rate cycles, yet a “soft landing” still seen in reach, the FOMC is likely to express only cautious optimism.

- The policy statement is due for key adjustments to the characterization of recent inflation and employment, and perhaps to the shifting balance of risks – but it’s not clear the Committee will adjust the forward rate guidance, in contrast to previous cycles where it explicitly signaled that it could move rates at an upcoming meeting.

- That would put the focus on Chair Powell to deliver the message at the press conference that the FOMC is cautiously open to cuts at upcoming meetings.

- The absence of a clear signal about an upcoming rate cut would disappoint current market pricing for 2 to 3 rate cuts by year-end, which is more aggressive than the 1 to 2 cuts the FOMC eyed just 6 weeks ago.

Note to readers: MNI’s separate preview of sell-side analyst summaries to follow on Monday Jul 29

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok