Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

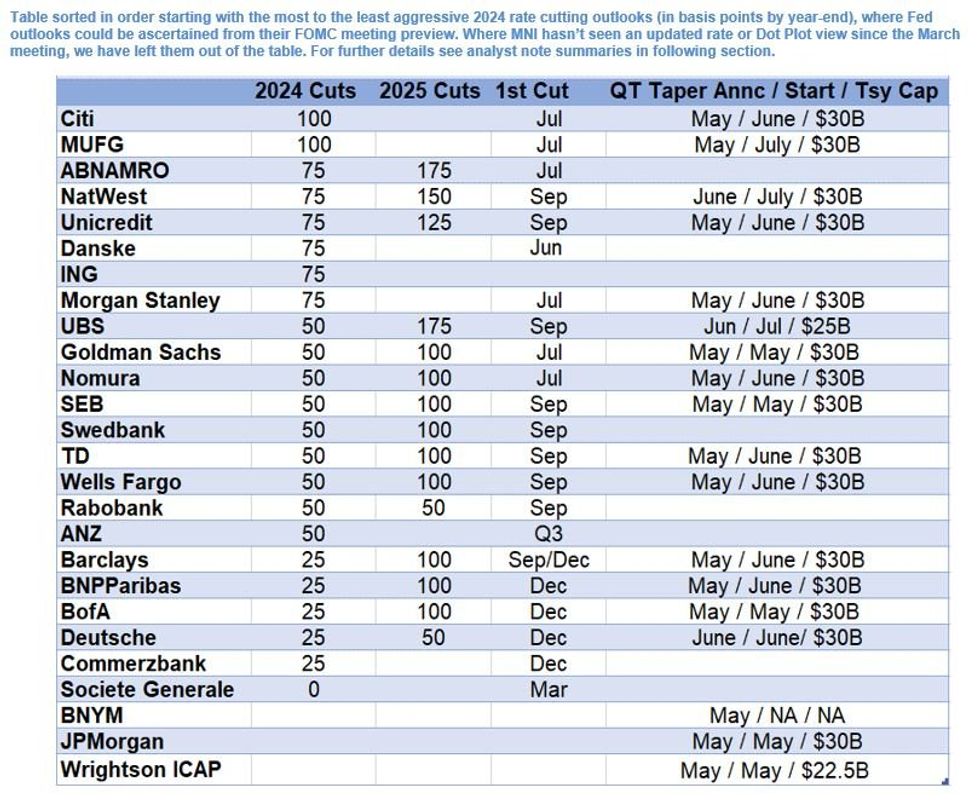

- Note to readers: This is an update to the MNI Fed preview published on Thursday April 25. Please see Page 26-31 of the PDF below for sell-side analysts' outlooks for the May 1 FOMC decision and future policy.

More Hawkish Message Expected As Cuts Get Pushed Back

Analysts generally look for a more hawkish message from the FOMC in May compared with March, in light of strong inflation and economic activity data.

- None expect the Statement forward guidance to be changed, though a few see potential for tweaks. Several eye risks of the characterization of inflation to be changed in a hawkish fashion.

- Generally, Powell is expected to tilt more cautious on the inflation outlook than in previous appearances, with potential flashpoints for markets including whether he acknowledges that 3 cuts are less likely to be the base case for the FOMC in 2024, and/or whether June is too early for the first cut.

- On tapering QT, consensus is clearly for an announcement at this meeting, with Treasury runoff capped at $30B (vs $60B currently) starting in June. Some see caps set slightly lower ($22.5-25B).

- Only one analyst (Danske) whose preview we read still sees a cut as early as June. Consensus for the first cut is clustered around Jul/Sep, though at least one (SocGen) sees the first only in 2025.

- A plurality of analysts see 50bp of cuts in 2024, with 100bp in 2025, though the range is somewhere from 75bp to 250bp cumulatively to end-2025 (incorporating analysts who provided forecasts for both years).

FULL PUBLICATION PDF HERE

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok