Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI Fed Review - June 2024: Destination Remains The Same

MNI Fed Review - June 2024: Destination Remains The Same

EXECUTIVE SUMMARY:

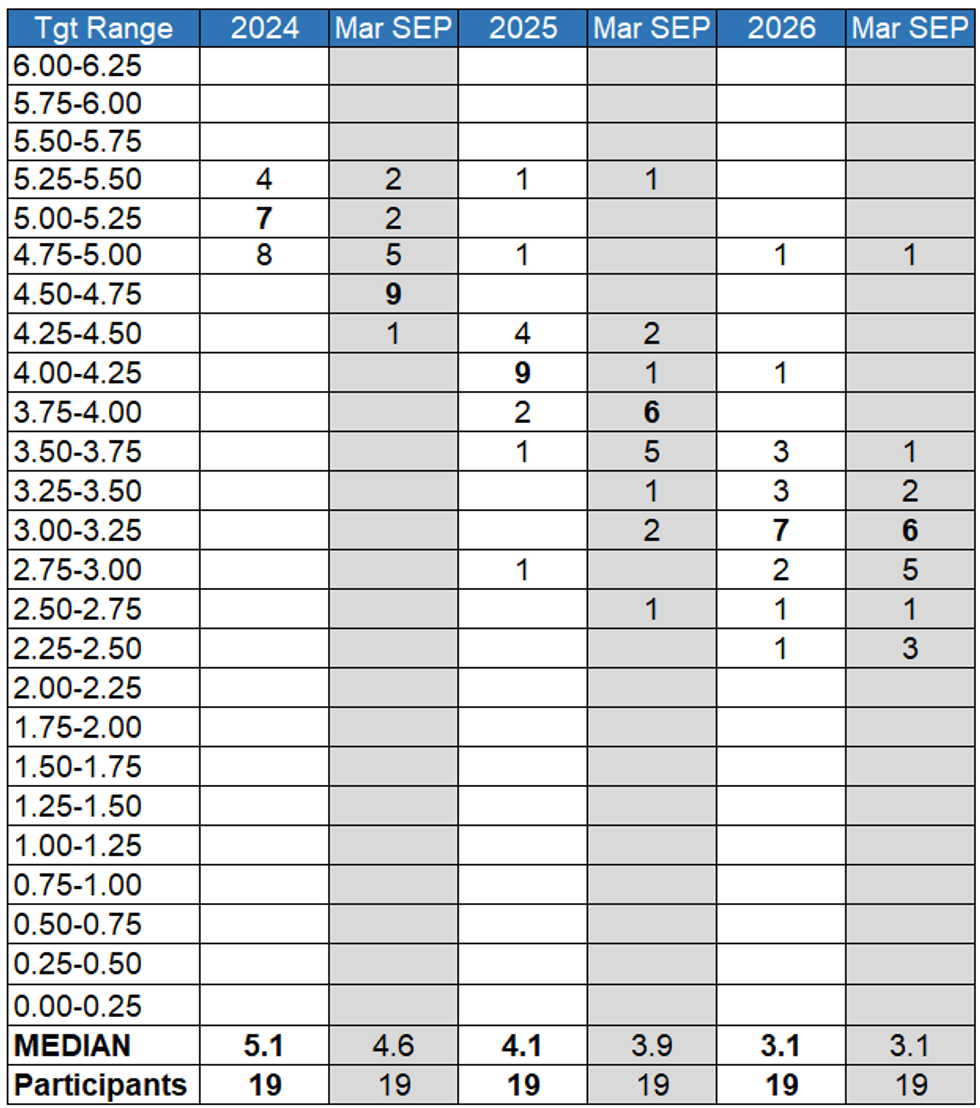

- The overall outcome of the June FOMC meeting was hawkish versus expectations, but couldn’t fully reverse the dovish impact of a very soft May CPI report released hours earlier.

- Markets reacted hawkishly to the new projection for the 2024 median Fed funds rate, which showed just one cut anticipated by year-end, versus three in March’s projection (and versus 2 widely expected).

- But the reaction was relatively muted, due in part to the fact that the 2025-26 path was relatively steady, implying 100bp of cuts in each of 2025 and 2026 (vs 75bp for each year in the prior edition) to the same destination of 3.1%. This was a point that Chair Powell reinforced in the post-meeting press conference.

- Powell gave little away on rate cut timing as expected, noting that while May’s CPI (+0.16% M/M core versus +0.28% consensus) in addition to April’s figure (+0.29% M/M) represented “progress” that was “building confidence”, “we don't see ourselves as having the confidence that … would warrant beginning to loosen policy at this time."

- In other words, the theme portrayed by the meeting communications is that rate cuts are being delayed, but they are still expected by year-end, and the ultimate destination hasn’t changed.

- This should keep September on the table for the first rate cut – but that will of course depend on inflation data in the interim looking more like April-May’s than the sharp rises in January-March.

FOR FULL ANALYSIS INCLUDING PRESS CONFERENCE TRANSCRIPT:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok