Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI Fed Review - Mar 2024: Soft Landing Story Remains The Same

MNI Fed Review - Mar 2024: Soft Landing Story Remains The Same

EXECUTIVE SUMMARY:

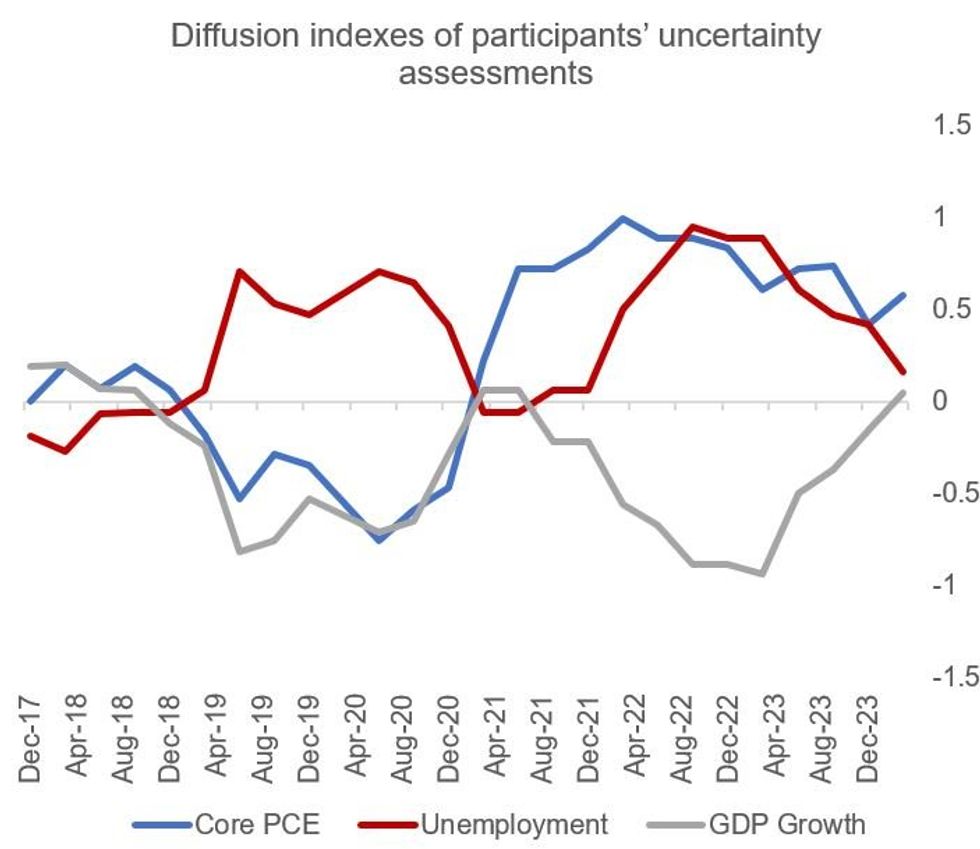

- The main takeaway from the March FOMC is that the Fed remains willing to start cutting rates at an upcoming meeting even in the face of an apparent stalling of disinflation progress to start the year.

- In describing a “bumpy road” to getting inflation back to 2% on a sustainable basis, Chair Powell said the January-February CPI/PCE data “haven't really changed the overall story, which is that of inflation moving down gradually on a sometimes bumpy road toward 2%. I don't think that story has changed."

- Judging from the new economic projections and Dot Plot, that “story” is part of a soft landing scenario, with robust growth and stable unemployment alongside disinflation – allowing rates to be cut 3 times this year (the same median outlook as at end-2023).

- Markets reacted dovishly, in part due to relief that the median 2024 dot didn’t rise, but also due to the perception that the Fed didn’t set a high bar to cuts (and Powell didn’t push back much against the idea that the first cut could come in May/June, while also noting no discomfort with current financial conditions).

- There were plenty of other areas of interest at this meeting besides the 2024 rate outlook, including a possible QT taper announcement in May, and a nudge higher in the longer-run rates Dot.

FOR FULL ANALYSIS INCLUDING 30 SELL SIDE SUMMARIES:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok