Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

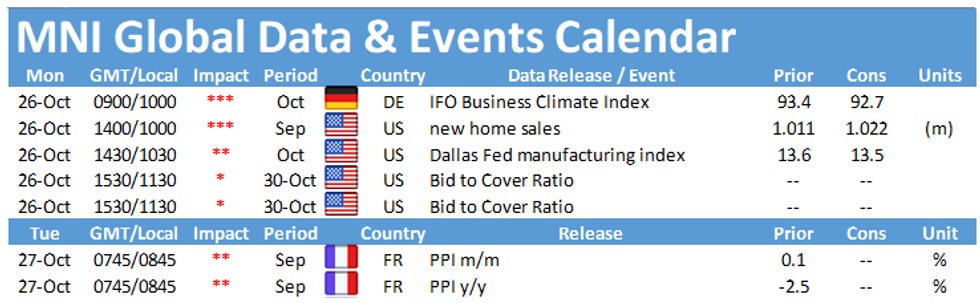

Monday sees a quiet day in terms of data releases, with the only publication scheduled in Europe being the Ifo business climate indicator at 0900BST. In the US, new home sales at 1400BST and the Dallas Fed Manufacturing Survey at 1430BST are worth mentioning.

Ifo business climate index seen falling

The Ifo business climate indicator edged higher in September, rising to 93.4, up from the 92.5 recorded in August. This marked the fifth consecutive increase to the highest level since February. In October, markets expect the headline business climate index to ease to 92.7, with expectations dropping to 96.0, while current conditions are seen slightly higher at 89.7. Both the current situations index and expectations rose in September to 89.2 and 97.7, respectively. While the manufacturing, retail trade and construction sectors saw solid gains in September, the service sector recorded a decline. This divergence is can also be seen in the recently released flash PMIs. The German flash manufacturing PMI surprised in October and rose to 58.0, while the services PMI slipped back to contraction territory.

US new home sales forecast to decelerate

The sale of new single-family houses in the US ticked up 4.8% in August on a monthly basis to a seasonally adjusted rate of 1,011,000, up from 965,000 recorded in July. New home sales were up 43.2% compared to August 2019. In September, markets are looking for another gain of 3.9% to 1,022,000 new home sales.

Dallas Fed manufacturing index expected to ease marginally

The general business activity index of the Dallas fed manufacturing outlook survey gained 6 points in September and rose to 13.6, which is the highest level since November 2018. The index is projected to cool in October with markets pencilling in a downtick to 13.5. The September report noted a stable reading for the company outlook index, however uncertainty regarding the outlook continued to rise. Similar survey evidence suggests an upside risk. The Kansas City Fed's manufacturing index ticked up in October, as did the Philadelphia Fed manufacturing index.

The events calendar remains quiet on Monday with no speeches scheduled for the day.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.