Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

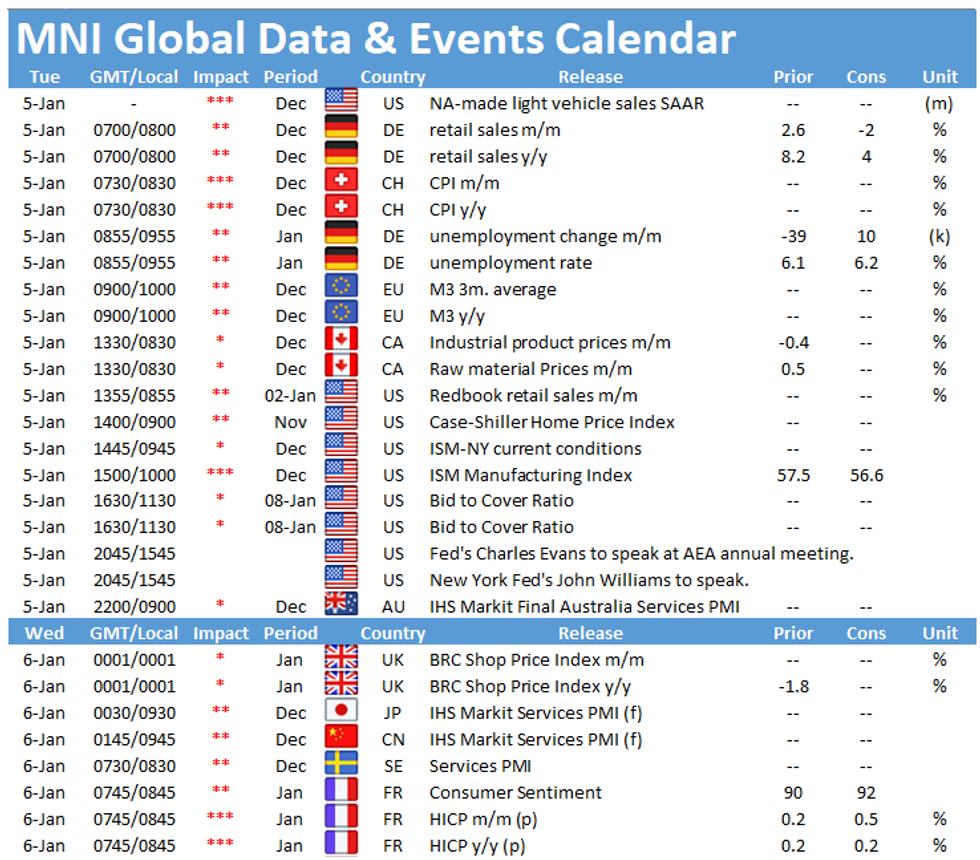

Tuesday morning kicks off with the release of German retail sales at 0700GMT, followed by German labour market data at 0855GMT. In the US the main data event is the release of the ISM Manufacturing PMI at 1500GMT.

German retail sales seen falling

German retail sales are expected to fall by 2.0% in November after October's solid 2.6% growth. November sales are likely to be pressured lower due to the partial lockdown as shops remained open but the hospitality sector had to close and social distancing rules were tightened. As infection rates remained elevated in December, shops and schools had to close from December 16 onwards, which is likely to weigh further on retail sales in December.

German unemployment rate seen marginally higher

The German unemployment rate is forecast to tick up slightly to 6.2% in December, up from 6.1% seen in November. Seasonally adjusted unemployment fell by 39,000 in November, but markets are looking for an increase in December by 10,000. The jobless rate increased only modestly during the crisis due to the short-term working scheme which was extended until the end of 2021. Last month's report noted that the demand for labour fell sharply at the beginning of the crisis, but recovered in recent months. The impact of the partial lockdown flattened the increase in labour demand as fewer new jobs were reported.

ISM manufacturing PMI seen lower

The ISM manufacturing PMI is forecast to tick down slightly to 56.6 in December which would mark the second successive decline. The indicator slipped to 57.5 in November, down from 59.3 seen in October. Employment led the decline in November, dropping by 4.8pt to 48.4 and shifting below the 50-mark. Anecdotal evidence suggests that the manufacturing sector recovered further in November, however, absenteeism, short-term shutdowns to sanitize facilities and difficulties regarding the return or hire of workers are causing problems and are likely to weigh on manufacturing growth going forward. Similar survey evidence provides a mixed picture. While the Chicago business barometer and the Kansas City Fed manufacturing PMI rose slightly in December, the Dallas Fed index and the Philadelphia Fed manufacturing index ticked down in December.

The events calendar is quiet Tuesday, with the only events worth noting being speeches by Chicago Fed's Charles Evans and New York Fed's John Williams.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.