Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

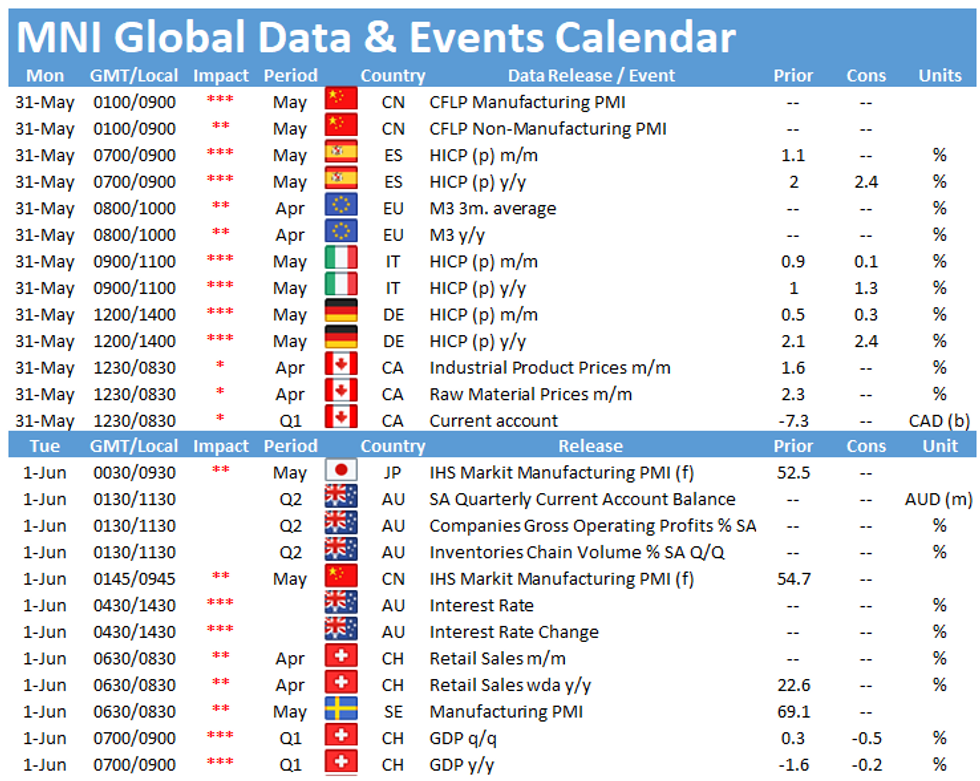

The main data events on Monday morning are the flash inflation figures for Spain at 0800BST, followed by Italy at 1000BST and Germany at 1300BST. There are no data publication scheduled in the UK or US due to bank holidays.

Flash inflation forecast to rise further in May

Annual Spanish inflation rose sharply in March and April, mainly on the back of base effects as prices are compared to the low figures seen at the beginning of the pandemic. In May, markets are expecting another uptick for the annual HICP to 2.4%, up from 2.0% recorded in April. INE noted that prices for housing and transport were the main drivers of April's increase. Housing prices rose due to a sharp increase of electricity prices, while transport inflation increased due to higher prices for fuels and lubricants for personal transport.

The Italian year-on-year HICP rose to 1.0% in April and markets expect the indicator to tick up further to 1.3% in May. Energy inflation was the main driver of April's uptick as prices rose 9.8%, up from 0.4% seen in March. At the same time, prices for unprocessed food and services related to transport declined in April. Meanwhile, core inflation eased to 0.3%.

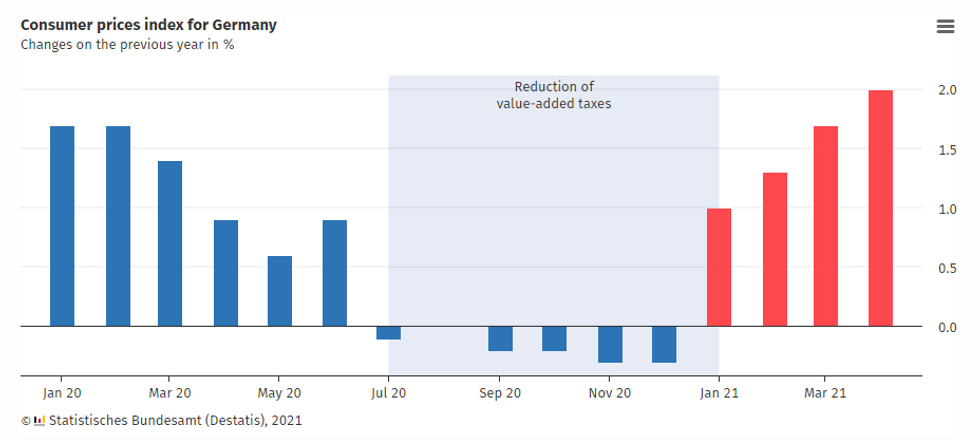

German inflation accelerated since the start of the year when the temporary VAT cut ended. The annual HICP rose to 2.1% in April, the highest level since November 2019. Energy price base effects were as well the main driver of April's increase. Markets are projecting another uptick of annual inflation to 2.4% in May with energy inflation being the main contributor.

Source: Destatis

Survey evidence suggests that firms are passing higher prices for inputs on to consumers, leading to upward pressure for CPI figures. The EZ flash composite PMI reported that average prices charged for goods and services rose at the fastest rate since 2002. The increase mainly stems from the manufacturing sector but prices for services also showed the biggest rise in two years.

There are no speeches scheduled on Monday.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.