Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

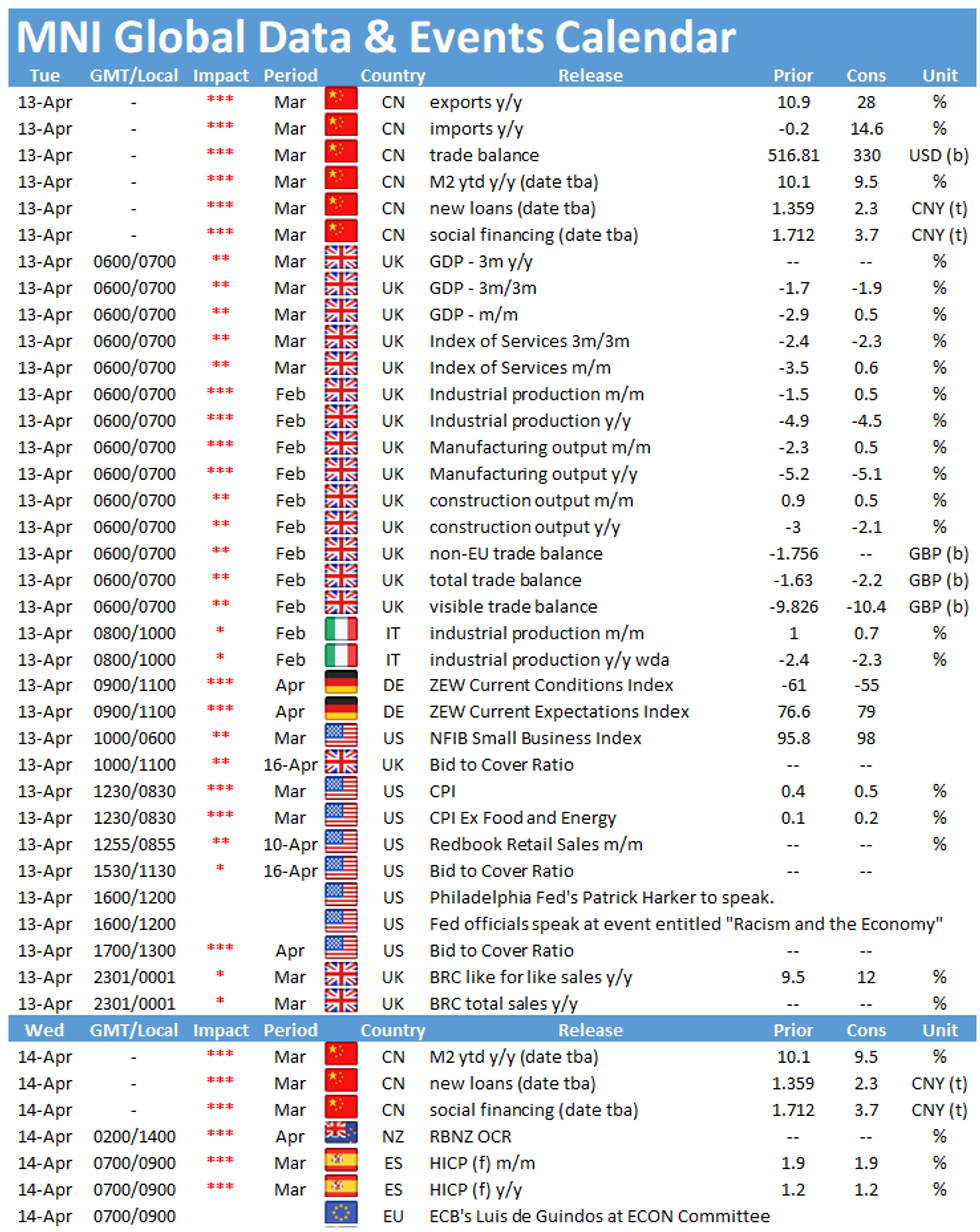

Tuesday starts with the publication of the UK's short-term monthly indicators at 0700BST, followed by Germany's ZEW survey at 1000BST. In the US, the release of inflation figures will be closely watched at 1330BST.

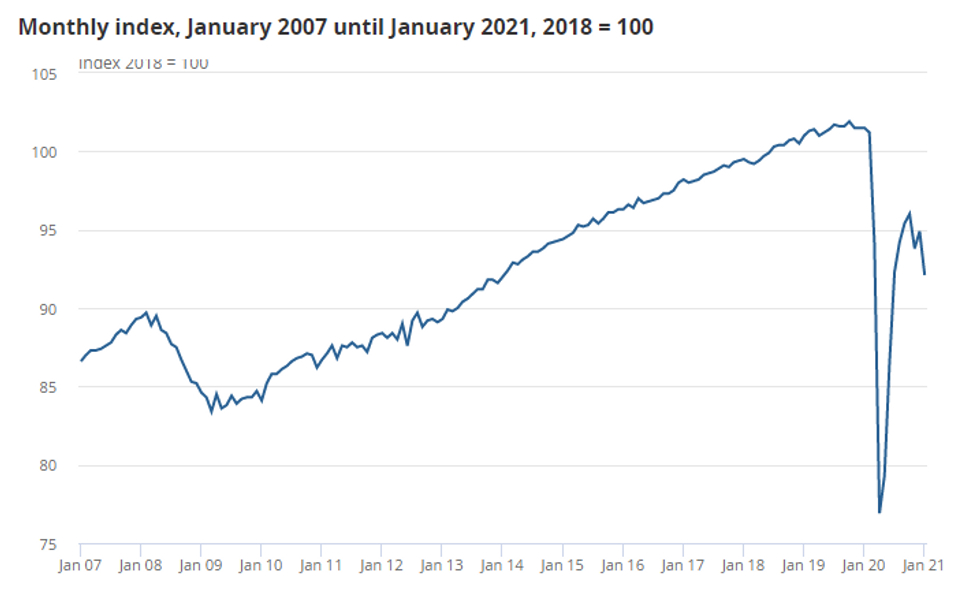

UK monthly GDP expected to tick up

After dropping by 2.9% in January, monthly UK GDP is expected to tick up by 0.5% in February. The recovery is anticipated to be broad-based with both industry and services expected to edge slightly higher in February, despite the national lockdown still being in place. Monthly industrial output is forecast to rise by 0.5% after dropping by 1.5% in January, however this will still leave output below its pre-pandemic level. The index of services was more than 10% below its pre-crisis level in January and markets look for a 0.5% increase in February. Overall, GDP was 9% lower in January than in February 2020 before the start of the crisis.

With non-essential shops and hospitality reopening and vaccinations on track, GDP is set to post substantial increases over the coming months as consumer-facing industries start to recover as well. Consequently, the service sector should see significant gains.

Source: Office for National Statistics

ZEW expectations forecast to rise further

Both the ZEW expectations and current conditions are expected to improve further in April. The expectations index is projected to rise to 79, which would be the fifth consecutive increase after November's dip and the highest level since May 2000. Respondents are more optimistic about the next six months ahead as hopes for a faster progress of the vaccination program keeps expectations elevated. March's survey saw fewer financial experts anticipate a decline of economic growth in Q2, than in February.

Despite being still in deep negative territory, current conditions are expected to improve as well. Markets forecast an increase by 6pt to -55. Nevertheless, infection rates are still high in Germany and the vaccination program is slower than desired, which weighs on the current situation and is likely to prevent a substantial rebound until the situation improves. Similar survey evidence is in line with market forecast. The Sentix index rose to the highest level since 2018 with both expectations and current conditions improving further.

US inflation seen higher

U.S. CPI is set to rise in March, with markets looking for a gain of 0.5% from 0.4% in February. That'll mostly be driven by surging energy prices. Meanwhile, base effects from the start of the pandemic will amplify core inflation, analysts say. Core CPI should rise 0.2% in March following a 0.1% gain in February and will likely be boosted by increases in travel-related prices like airfares, hotels, and cars.

The events calendar throws up a quiet schedule with the only speeches scheduled being by Philadelphia Fed's Patrick Harker and Richmond Fed's Tom Barkin.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.