Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

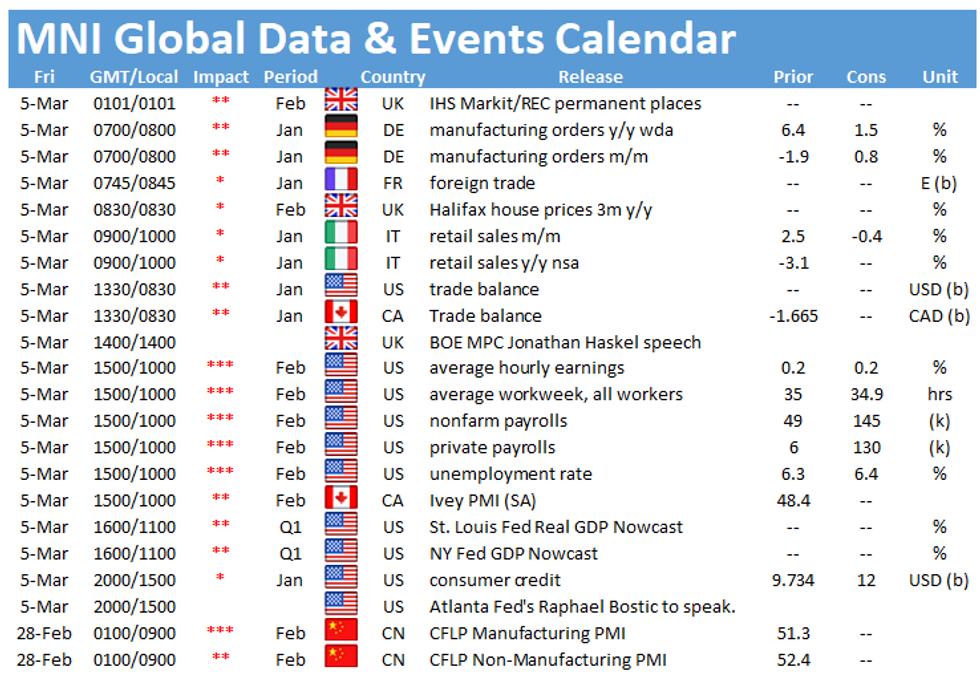

Friday morning kicks off with the publication of German factory orders at 0700GMT, followed by Italian retail sales at 0900GMT. The highlight in the US is the release of nonfarm payroll data at 1330GMT.

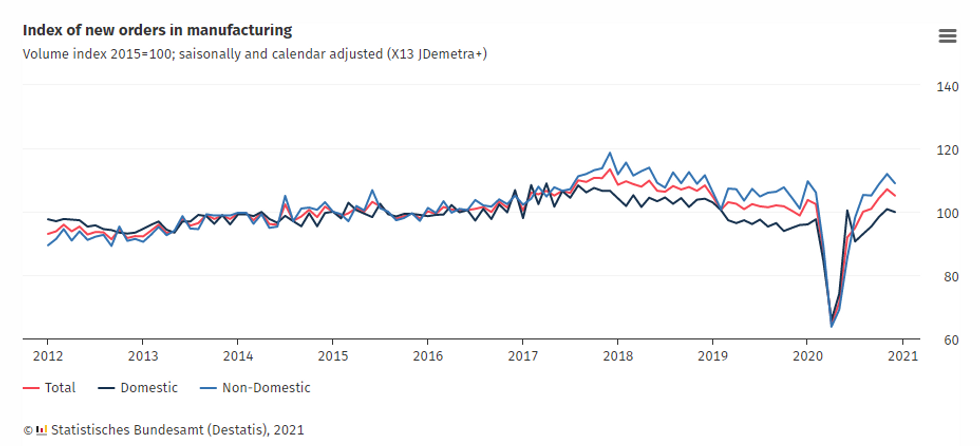

German industrial orders seen higher

Monthly factory orders declined by 1.9% in December following seven consecutive months of gains. Nevertheless, December orders were 2.6% higher than in February 2020. In January, markets are looking for a small rebound to 0.8%, while the annual rate is seen at 1.5%. Forward looking survey evidence is in line with market forecasts. Germany's manufacturing PMI continues to signal strong growth in the manufacturing sector with higher demand from Asia, the US and across Europe and new orders hitting the highest level since October. Moreover, the Ifo business climate indicator for the manufacturing sector jumped to highest level since November 2018 in February.

Source: Destatis

Italian retail sales to fall

December retail sales increased by 2.5% on a monthly basis, while annual sales declined by 3.1% with non-food sales dropping by 9.4%, while food sales were up 6.6%. In January markets expect retail sales to fall by 0.4%. Restrictions got tightened in several parts of the country as infection rates rose significantly, which weighs on sales in January. February saw further tightening of covid rules; hence retail sales are likely to remain subdued going forward.

Bounce for US nonfarm payrolls

U.S. payrolls growth likely surged in February, with Bloomberg forecasting a monthly gain of 145,000 jobs, nearly tripling January's disappointing 49,000 gain. High frequency data and regional Fed surveys point to some improvement in both goods producing and services payrolls through February. The unemployment rate should tick up slightly to 6.4% from 6.3%, according to Bloomberg.

The main events to look out for on Friday include speeches by BOE's Jonathan Haskel and Atlanta Fed's Raphael Bostic.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.