Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

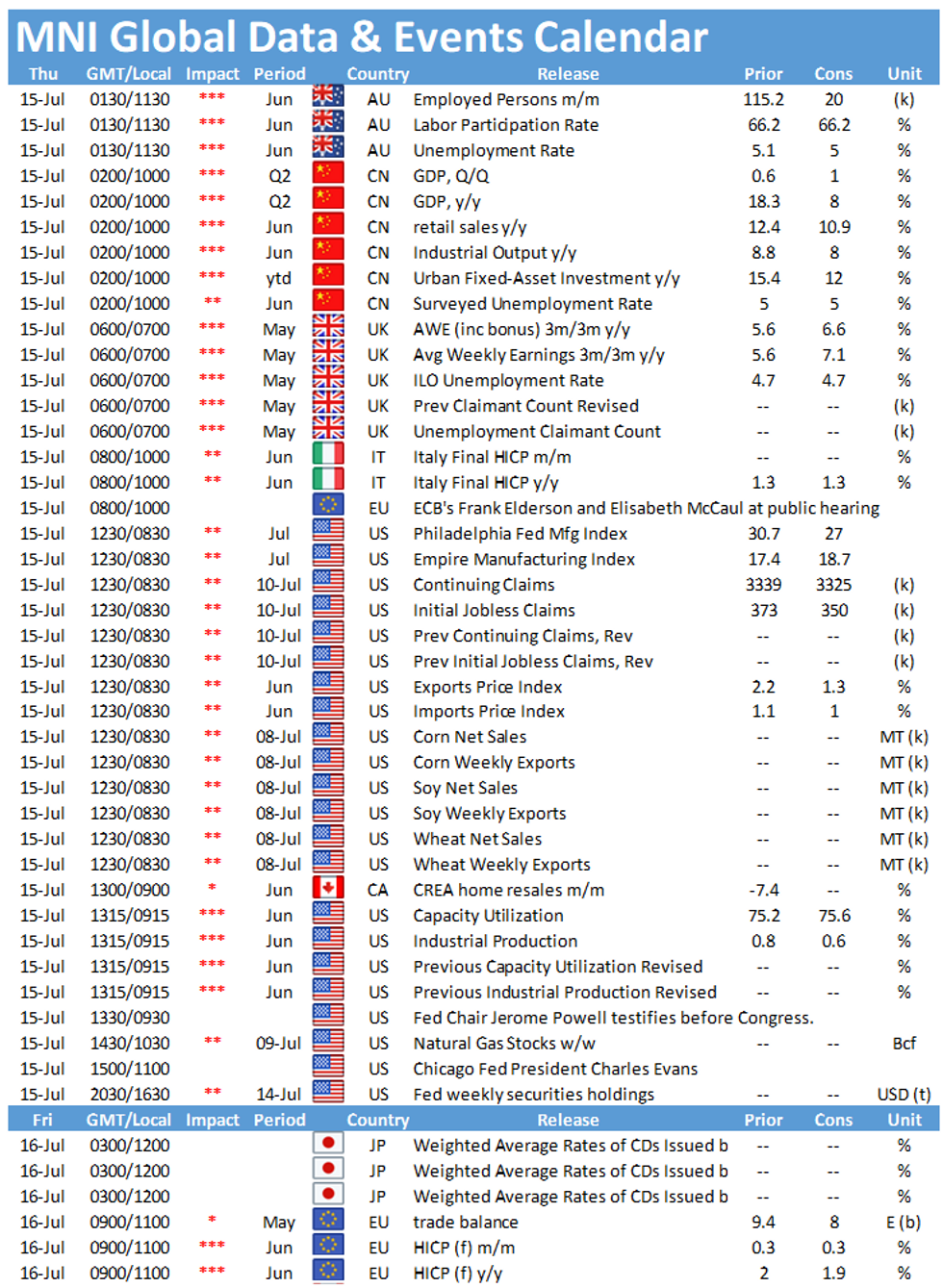

The main data event in Europe Thursday is the publication of the UK's labour report at 0700BST. In the US, the release of the Empire State Manufacturing index at 1330BST and US industrial production at 1415BST will be closely watched.

UK's jobless rate seen unchanged

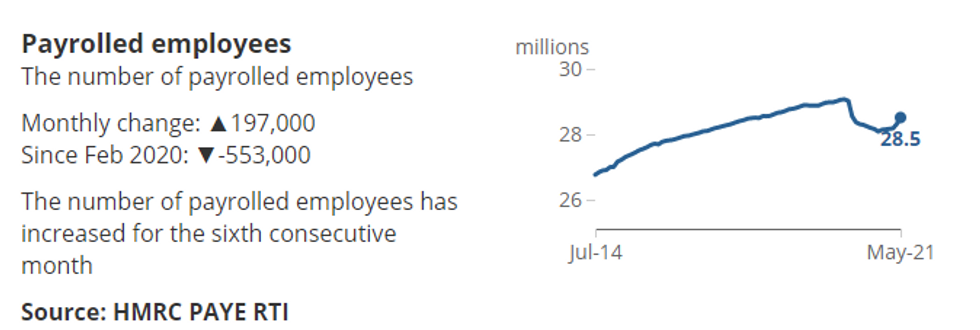

The UK's jobless rate is forecast to remain at 4.7% in May according to market analysts. In April, the unemployment rate ticked down slightly, while employment continued to recover and the inactivity rate was broadly unchanged. Employment is forecast to improve further with markets looking for an increase of 90,000 in the three months to May. More up-to-date PAYE data for May showed the sixth consecutive increase of payrolled employees and June is likely to post another uptick as demand picked up, especially in the hospitality sector. Nevertheless, May's data showed that there are still 553,000 fewer people in payrolled employees since the start of the pandemic. Meanwhile, total and regular earnings are both expected to accelerate in May with total wage growth seen at 7.1%.

Survey data suggests that recruitment activity is picking up in June as vacancies jumped to a record high. The KPMG/REC jobs report saw a sharp increase of demand for staff with permanent placements surging to a record high.

Source: Office for National Statistics

Empire State Manufacturing index forecast to edge higher

The general business activity index of the Empire State Manufacturing Survey is expected to tick up to up to 18.7 in July, up from 17.4 recorded in the previous month. June's report noted that business activity continued to expand, although at a slower pace with the headline index falling 7 points. While, new orders, shipments and unfilled orders rose, delivery times lengthened again and inventories declined. However, firms remained optimistic regarding the outlook in the next six months.

US industrial production projected to slow

Monthly industrial output in the US accelerated to 0.8% in May and markets expect the index to slow to 0.6% in June, which would mark the fourth consecutive monthly increase. Manufacturing output rose 0.9% in May and was largely driven by a sharp rise of motor vehicle assemblies. Annual output increased by 16.3% in May, but compared to February 2020, output was still 1.4% lower. Capacity utilization registered at 75.2% in May and markets expect a small uptick to 75.6% in June.

Survey evidence suggests growing business activity in the industrial sector. The ISM manufacturing PMI saw another strong reading in June at 60.6, while the June IHS manufacturing PMI saw the strongest improvement in operating conditions since May 2007.

The events calendar holds several interesting speakers in the cards, including ECB's Frank Elderson, Fed's Jerome Powell and Chicago Fed's Charles Evans.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.