Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

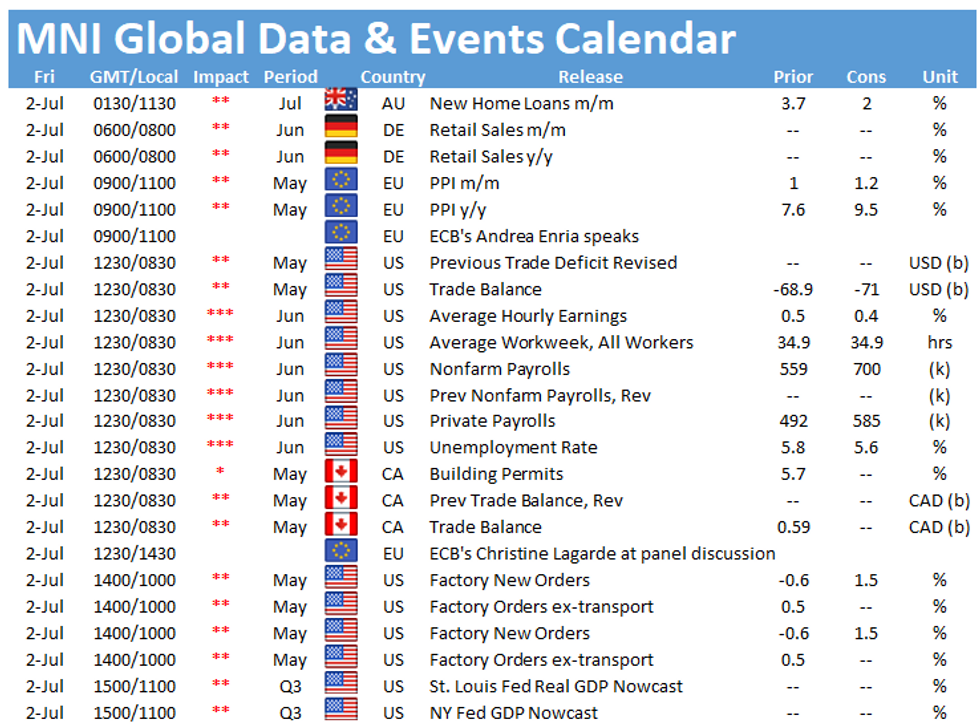

The only data release scheduled in Europe Friday is the EZ producer price inflation at 1000BST. The main event in the US is the release of nonfarm payrolls at 1330BST, followed by US factory orders at 1500BST.

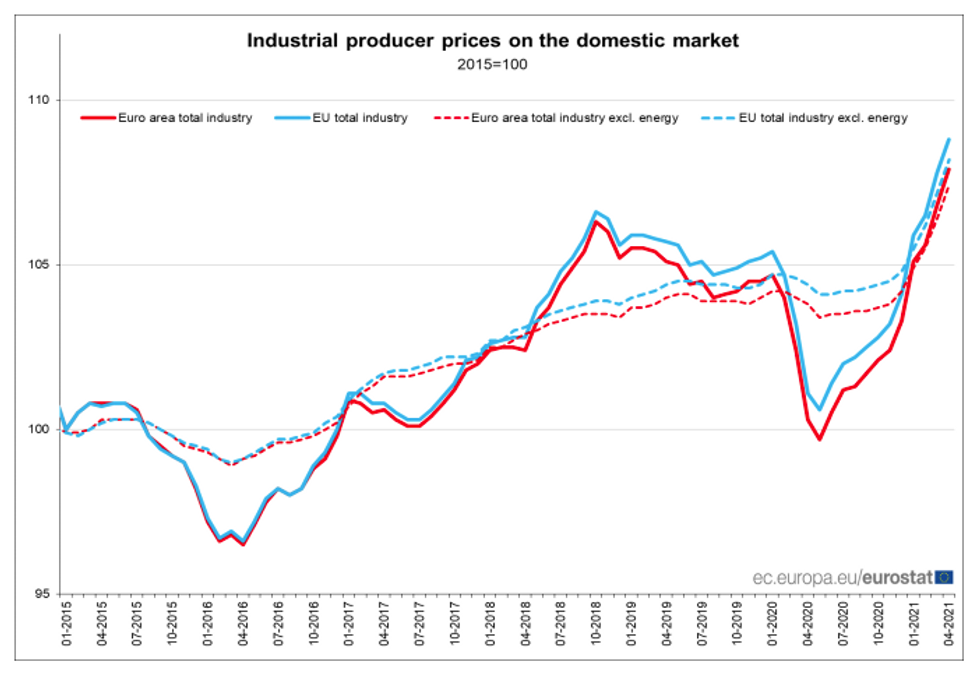

EZ PPI forecast to rise further

Annual producer price inflation rose markedly in recent months and jumped to an almost 13-year high of 7.6% in April. In May, markets are looking for the index to rise further to 9.5%, which would mark the highest level on record. April's uptick was driven by a sharp increase of energy prices, up 20.4%, followed by intermediate goods, rising by 6.9%. Survey evidence continue to report rising input price inflation due to strong demand and limited supply. The EZ manufacturing PMI saw input prices rise at a record pace, which led to an increase of output price inflation as well.

Source: Eurostat

US nonfarm payrolls seen increasing

Hiring likely accelerated in June, with employers adding up to 700,000 jobs through the month, according to Bloomberg. New graduates and students off for the summer expanded the labour pool, but the supply of available workers last month remained muted, putting more upward pressure on wages. Strong job growth should push the unemployment rate down to 5.6% from 5.8%, according to Bloomberg.

US factory orders expected to rebound

Factory orders in the US declined by 0.6% in April, after rising by 1.4% in the previous month and marking the first drop in 12 months. Transportation equipment saw the largest decrease, down 6.6%. Excluding transportation factory orders rose by 0.5%. In May, markets expect factory orders to rebound to 1.5%, which would mark the highest level since January. The IHS manufacturing PMI also noted a significant increase in new business in June and May.

The main events to follow on Friday include speeches by ECB's Andrea Enria and Christine Lagarde.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.