Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

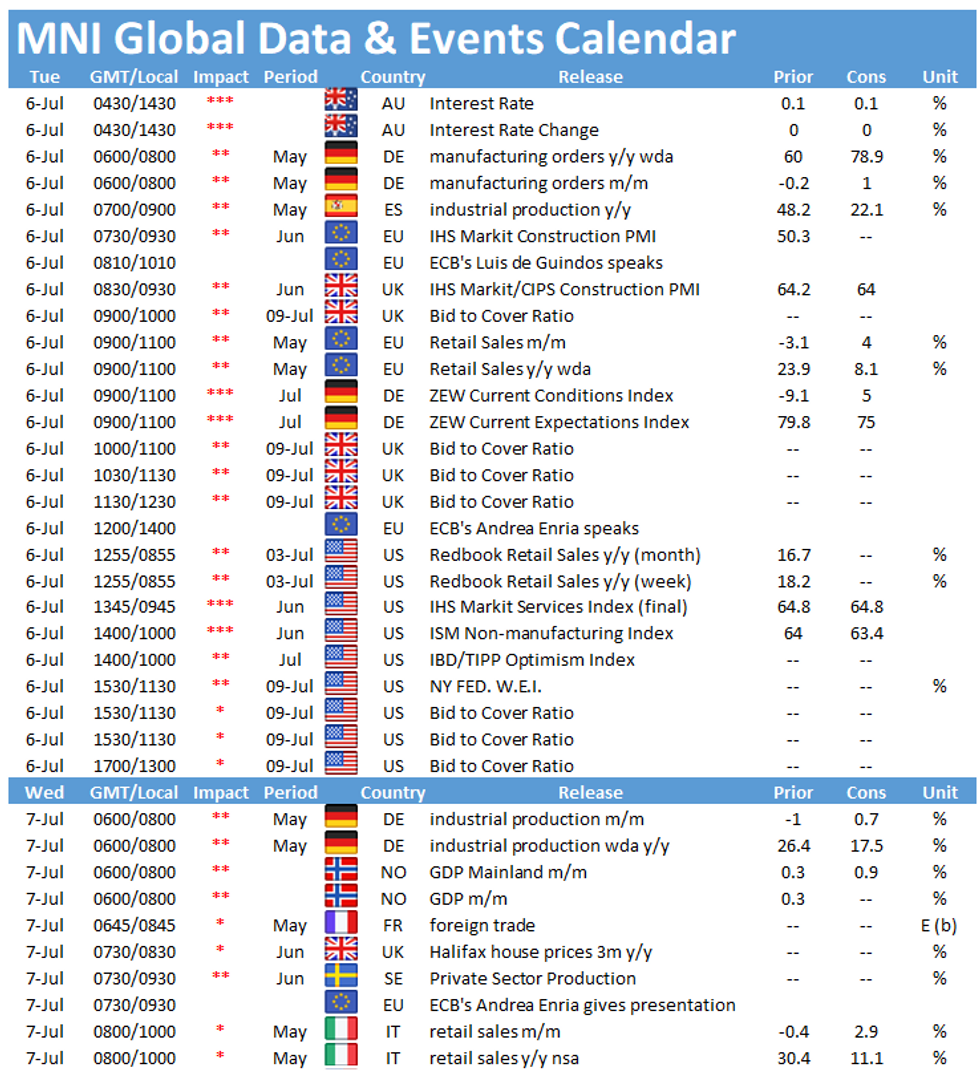

The main data Tuesday include the ZEW survey and EZ retail sales, both released at 1000BST. In the US, the publication of the ISM services PMI at 1500BST is the highlight of the day.

ZEW Expectations seen slightly lower

The ZEW Expectations index eased marginally to 79.8 in June, although from a very high level. In July, markets are looking for another drop to 75.0, which is still a historically high level. The current conditions index on the other hand, rose sharply in June, up 31 points to -9, its highest level since August 2019. The index is forecast to rise further this month, to +5, which will be the first positive reading since 2019.

Last month's report noted that especially the loosening of restrictions in the service, retail and hospitality sector provided a boost to economic activity. The current situations index should see another gain in July, as the easing of restrictions continued across Europe. Market forecasts are in line with similar survey evidence. The Sentix index rose to the highest level since Feb 2018 with current conditions rising markedly, while expectations ticked down in July.

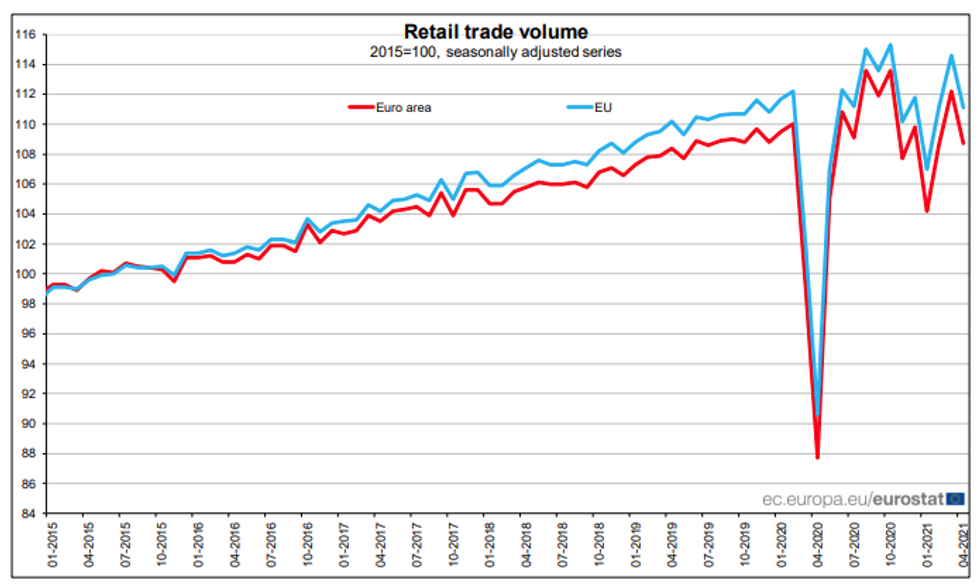

EZ retail trade expected to rebound in May

Retail sales in the Eurozone dropped by 3.1% in April as coronavirus restrictions were widely in place. In May, markets are projecting an uptick by 4.0%, which would mark the highest level since February where sales grew 4.2%. Restrictions got loosened from May onwards and vaccinations gained momentum across Europe which bodes well with consumer confidence and household spending.

The further easing of coronavirus rules in June and July together with warmer weather and tourism picking up slightly, should result in sold gains for retail sales in the coming months.

Source: Eurostat

ISM services PMI projected to edge lower

U.S. service sector activity likely held steady through June, with the ISM Services Index forecast to dip just slightly to 63.5 from a record-high 64 in May, according to Bloomberg. Analysts say the index is likely to fall further in coming months as the effects of fiscal stimulus and reopenings fade but should still remain well above the 50 benchmark that signals expansion.

The only events scheduled on Tuesday include speeches by ECB's Luis de Guindos and Andrea Enria.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.