Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

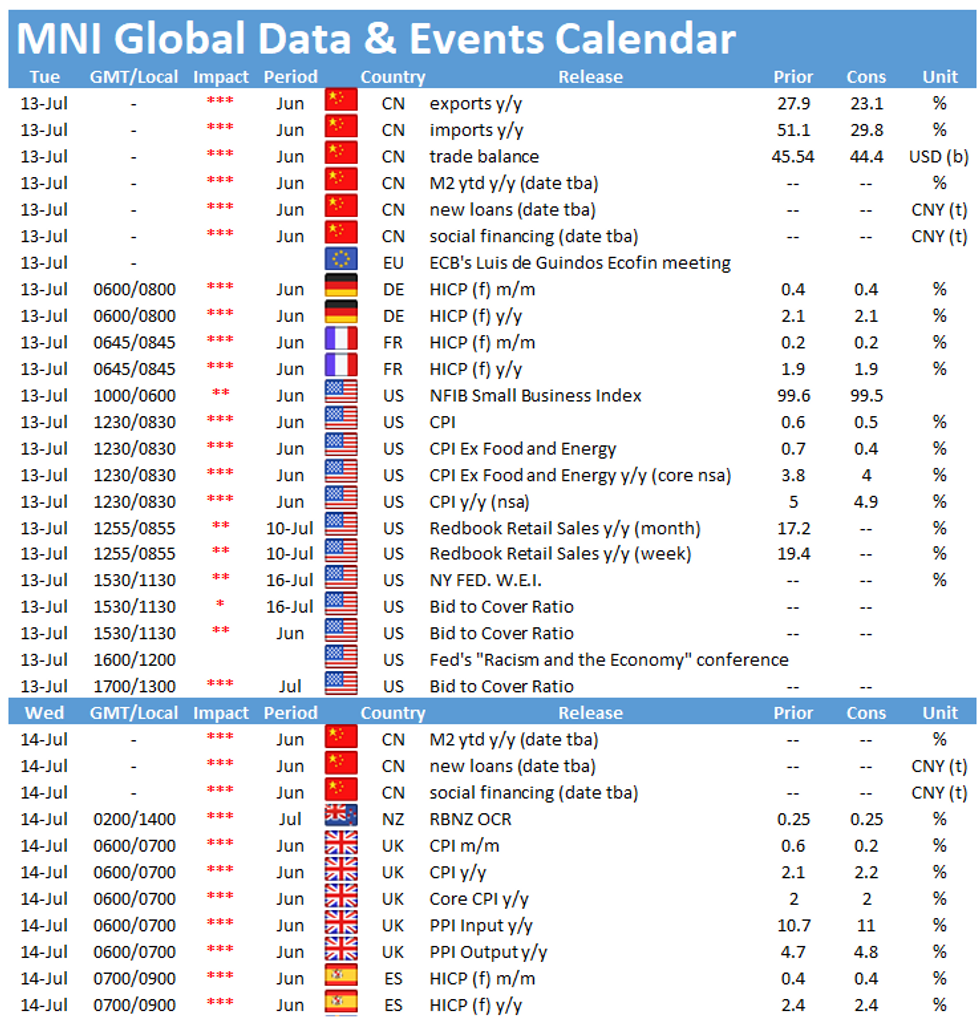

Inflation is the theme of the day in terms of data releases. Tuesday morning kicks off with the publication of final German inflation at 0700BST, followed by final French inflation figures at 0745BST, while the US consumer price index is released at 1330BST.

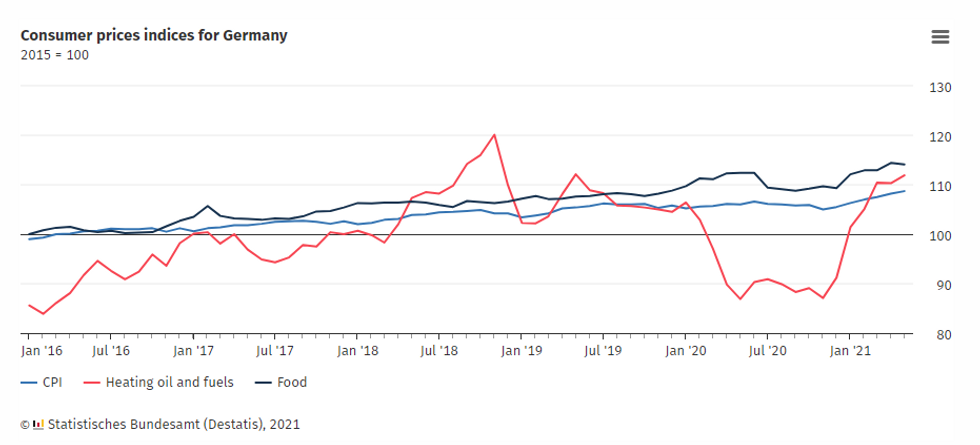

June German inflation forecast to ease

According to the flash estimate, German inflation eased to 2.1%, down from 2.4% recorded in May, and markets expect an unchanged reading for the final print. The flash report showed that prices for energy, food and services decelerated in June. The impact of energy price base effects eased in June reflecting a loosening of restrictions in June 2020 compared to the previous months.

However, base effects stemming from the German VAT will push up headline inflation from July onwards, as consumer prices declined markedly from July 2020 until December 2020 when the VAT cut was in place. Moreover, the continued reopening is likely to put pressure on service inflation and survey evidence suggests that higher input costs are passed on to consumers.

Source: Destatis

French consumer prices accelerated

French flash inflation ticked up slightly in June to 1.9%, up from 1.8% recorded in May. The increase was driven by a rebound in prices for manufactured goods in link with clothing and footwear prices, while energy and services prices slowed in June according to the flash estimate. Markets expect the final print to register in line with the flash results.

Survey evidence suggests that price pressures are intensifying. The services PMI saw output price inflation rise at the steepest rate in almost a decade in June. Additionally, Insee's consumer confidence survey shows that the number of households expecting inflation to rise in the next year remains above the long-term average.

US monthly consumer price index projected to decelerate

Price pressures continued through June as labour shortages and ongoing supply chain disruptions hampered goods production and demand rose solidly. U.S. CPI in June should increase 0.4% in June following a stronger 0.7% increase in May, according to Bloomberg. From a year earlier, CPI should grow 4.9%, little changed from the May's 5% y/y gain.

Excluding food and energy prices, CPI should increase 0.5% m/m and 3.8% y/y, according to Bloomberg.

Analysts say high inflation readings are being amplified by base effects and more transitory factors should begin to fade soon, but things like higher will likely keep inflation running above 2.5% through 2022.

The only event scheduled on Tuesday is the Ecofin meeting where ECB's Luis de Guindos is participating.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.