Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

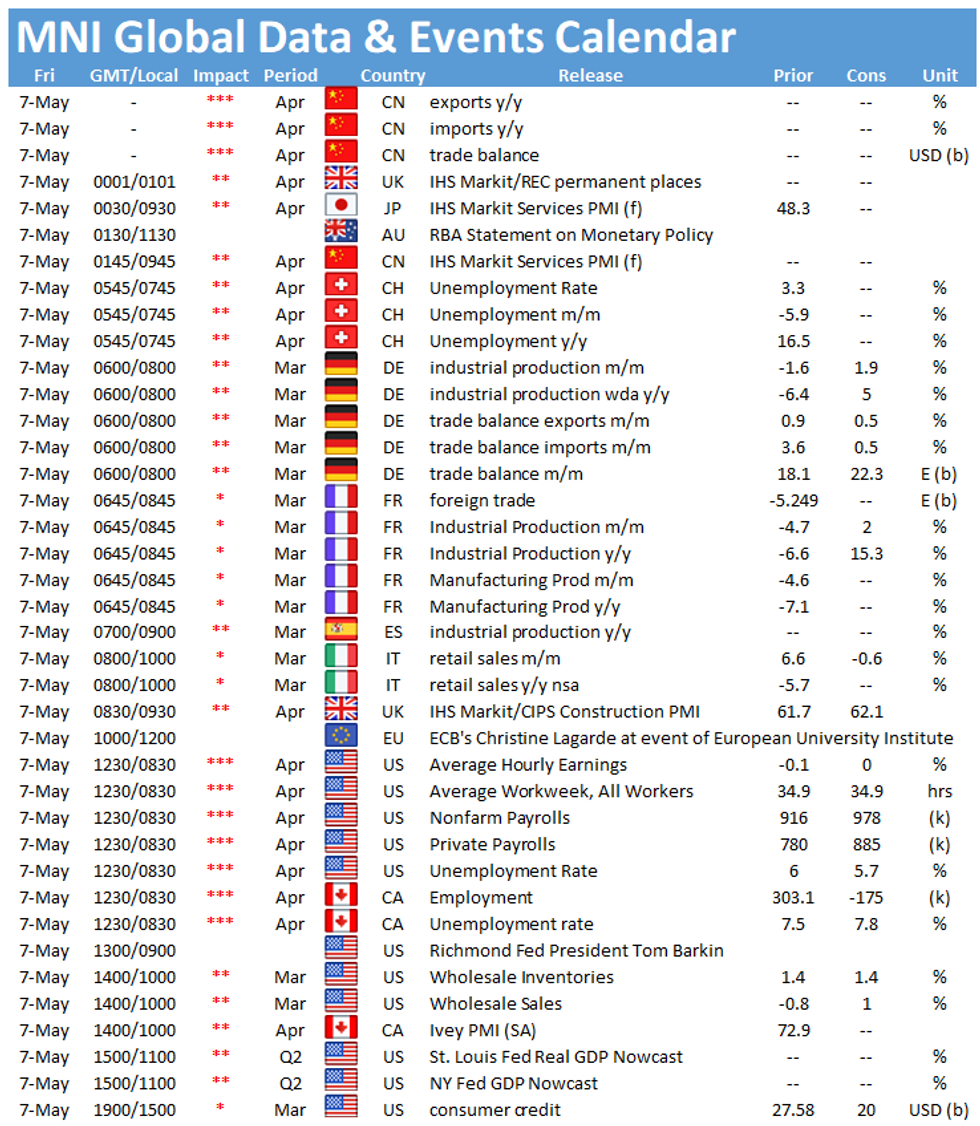

Friday kicks off with the publication of German industrial production at 0700BST, followed by French industrial output at 0745BST. The highlight in the US is the release of nonfarm payrolls at 1330BST.

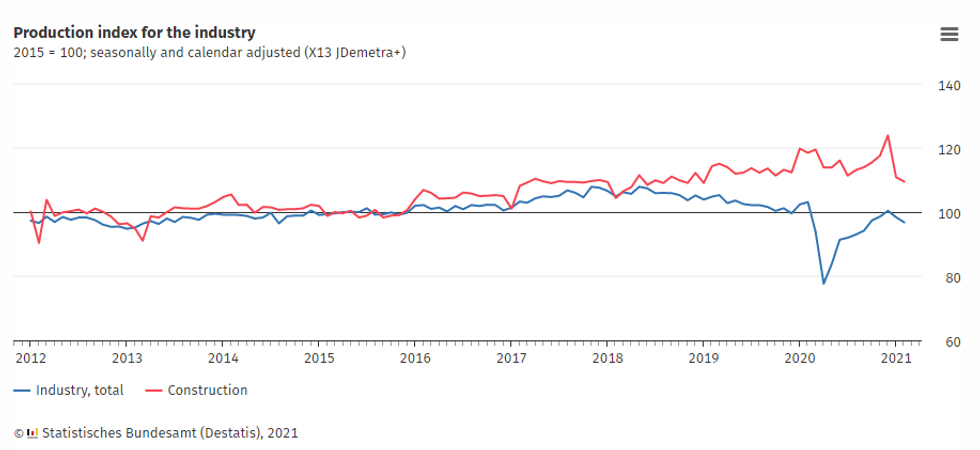

German industrial production forecast to rebound

German industrial production is forecast to rebound to 2.1% on the month, after output dropped by 1.6% in February and by 2.0% in January. The industrial sector showed a disappointing start to the year, despite surveys indicating strong business activity. In February 2021 production was still 6.4% lower than in February 2020 before the start of the pandemic.

Surveys continue to show strong readings but also emphasize the current supply chain issues, which weigh on industrial output. Nevertheless, the truck toll mileage index, which is closely connected with industrial output, rebounded in March after February's decline. Moreover, factory orders surprised in March and rose by double the extent expected.

Source: Destatis

French industrial output seen rising

French industrial output is also forecast to rebound to 2.0% in March after declining by 4.7% in February, which was the largest drop since April 2020. Compared to February 2020, output was still 6.6% lower. February's decline was broad-based with almost every major category posting a monthly decrease.

Survey evidence signals strong business activity in the manufacturing sector. The manufacturing PMI eased slightly in April but continued to show improvement in business conditions with output and new orders rising sharply. Insee's business climate indicator for the manufacturing sector rose markedly in March but ticked down marginally in April.

US nonfarm payrolls seen higher

Employers are expected to have added 950,000 jobs in April, according to the Bloomberg consensus, higher than March's 916,000 gain. Business restrictions were eased through April as more of the public became vaccinated, and weekly jobless claims dipped to pandemic lows through the Bureau of Labor Statistics' reference period.

Job growth in leisure and hospitality, manufacturing, and construction was particularly strong, according to anecdotal evidence from the Fed's Beige Book. But many employers struggled to hire workers hesitant to return to the workplace, which could put some downward pressure on overall job gains.

The main events to look out for include speeches by ECB's Christine Lagarde and Richmond Fed's Tom Barkin.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.