Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

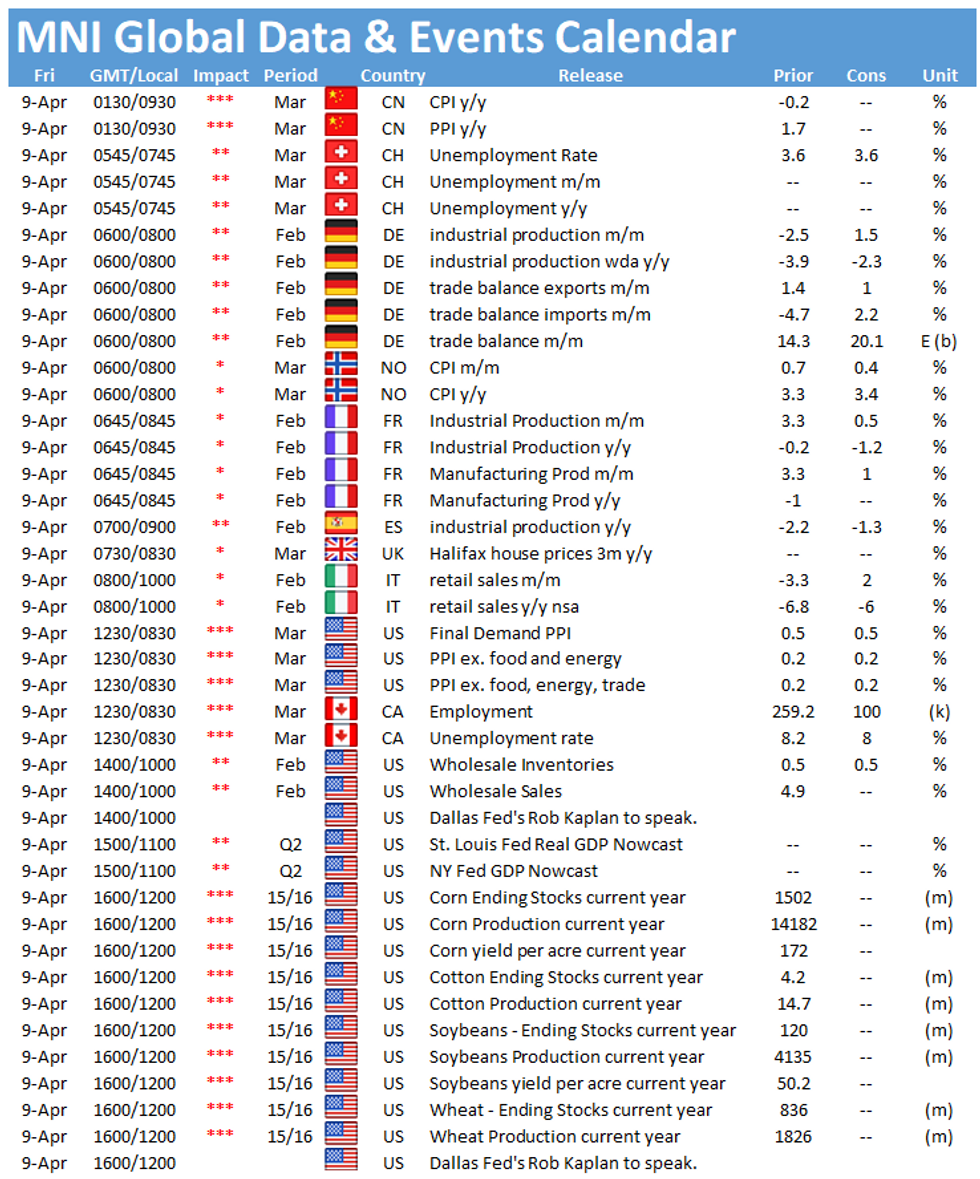

The main data points in Europe Friday are releases of industrial production figures, starting with Germany at 0700BST and followed by France at 0745BST. In the North Americas, the Canadian labour force survey at 1330BST will be closely watched.

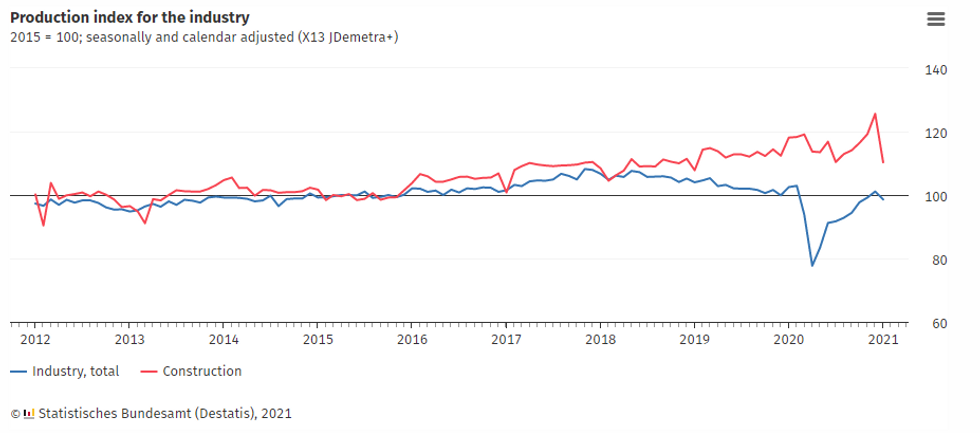

German industrial output seen rising

Industrial production is forecast to rise by 1.5% in February after declining by 2.5% in January. January's decline was the first drop since April 2020 and was driven by a significant decrease of consumer goods production. Annual sales dropped by 3.9% in January and markets expect the indicator to fall by 2.3% in February. Output in January was still 4.2% lower than before the pandemic.

Survey evidence indicates strong business activity in the manufacturing sector. While the manufacturing PMI posted a record high in March, the Ifo business climate indicator rose to the highest level since June 2019. On the other hand, the truck toll mileage index, which is closely connected to industrial production, fell further in February.

Source: Destatis

French industrial output expected to decelerate

Monthly industrial output growth is projected to slow to 0.5% in February after rising by 3.3% in the previous month. January saw a rebound in manufacturing output, up 3.3% and especially in construction output which surged by 16.3% after falling by 9.2% in December.

Survey evidence suggests solid business activity expansion in the French manufacturing sector. March's manufacturing PMI rose to the highest level since 2000 with both output and new orders expanding markedly. However, the report also noted severe supply chain disruptions which led to higher prices. Insee's business climate indicator for the manufacturing industry ticked up in February and remained stable in March. Despite recent increases, the index remains below the pre-crisis level.

Canadian labour market forecast to improve further

Restrictions were eased in many Canadian provinces in early February, which led to the reopening of many non-essential businesses. As a result, employment increased by 259,000 or 1.4% in February, after falling in the previous two months. In March, markets look for an uptick by 100,000 for employment, while the unemployment rate is forecast to ease to 8.0%, down from 8.2% seen in February. The jobless rate already fell significantly in February to the lowest rate since March 2020.

The events calendar remains quiet on Friday and the main speakers to look out for include ECB's Luis de Guindos and Dallas Fed's Rob Kaplan.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.