Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

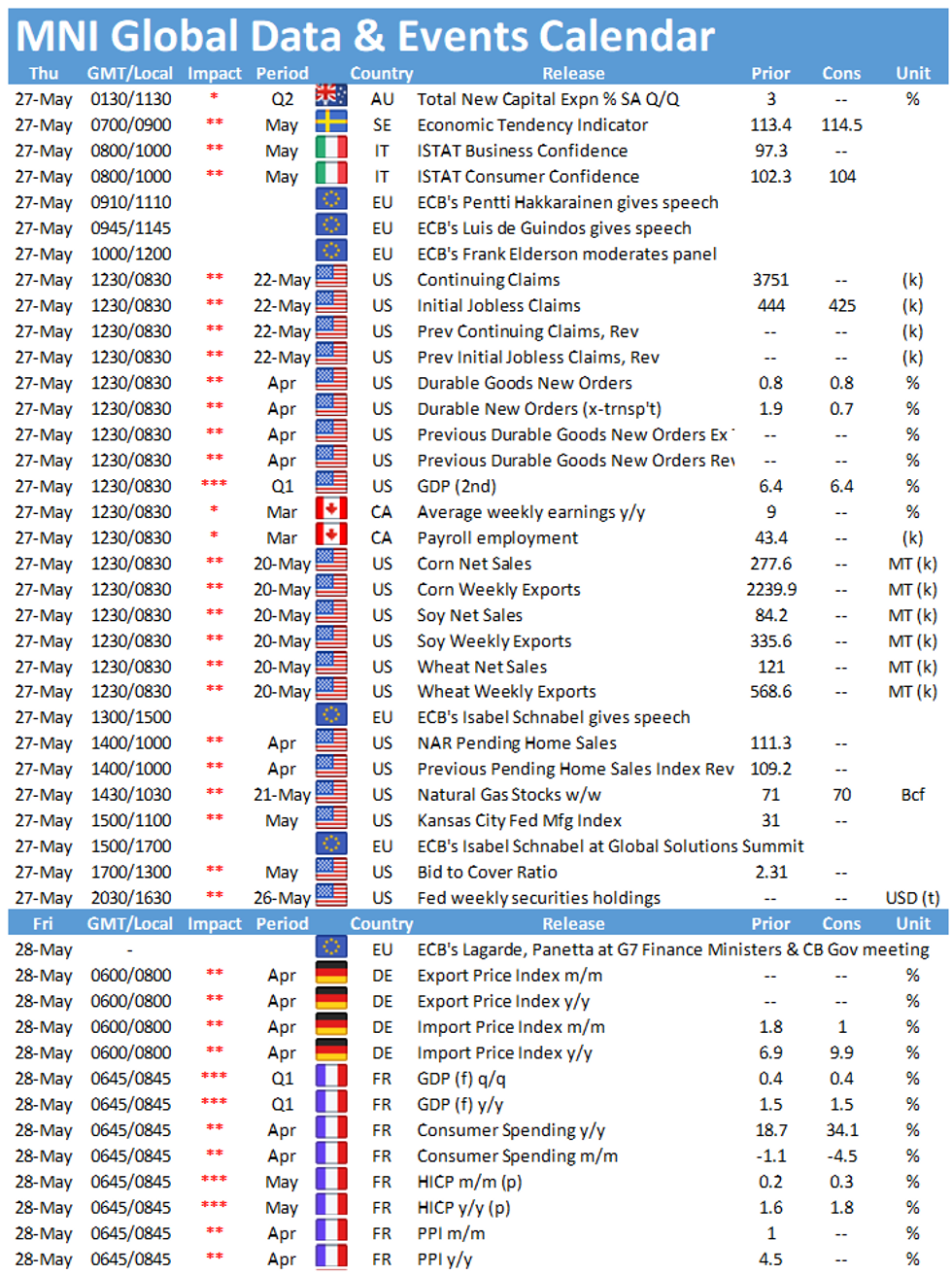

The main data events in Europe Thursday include Italian consumer and business confidence indicators at 0900BST. In the US, the release of Initial jobless claims at 1330BST will again be closely watched.

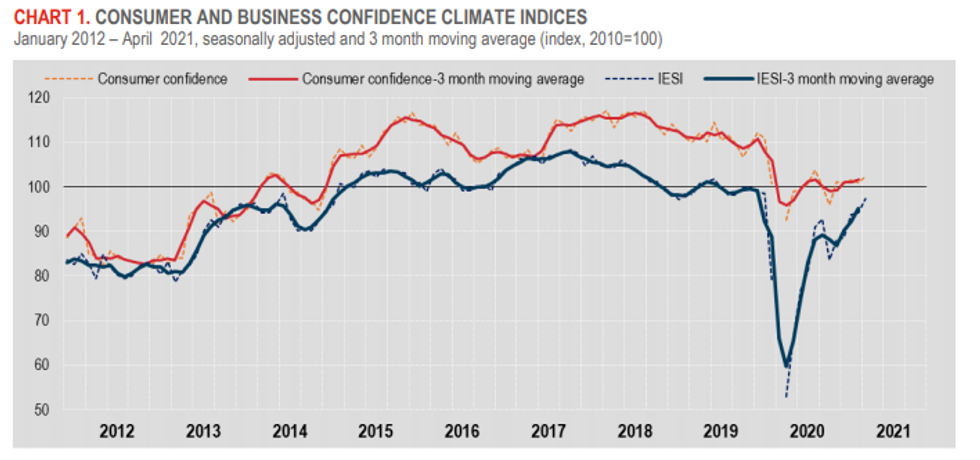

Italian consumers and business more optimistic

Italian consumer sentiment is expected to tick up to 104.0 in May, which would mark the highest reading since the start of the pandemic. The index rose to 102.3 in April with consumer's assessment of the economic situation and their financial one both improving. Meanwhile, business sentiment edged higher as well in April to 97.3 as did the manufacturing confidence index. April's report showed that firm's opinion on both current and expected new orders improved. Manufacturing sentiment is forecast to post another gain in May with markets looking for an uptick to 106, up from 105.4.

Restrictions have been loosened in Italy in mid-May with rules on international travel being eased as well, which bodes well for both consumer and business confidence. Other survey evidence is in line with market forecasts. The flash EZ consumer sentiment also gained 3 points in May, pushing the indicator slightly above the pre-crisis level. Moreover, the flash EZ composite PMI noted that business activity rose markedly in the euro area overall.

Source: Istat

U.S. Jobless Claims forecast to slow

U.S. jobless claims filed through May 22 are set to dip to 425,000 from 444,000 through May 15, a new pandemic low, according to the Bloomberg consensus. Initial claims should continue to trend downward as the economy opens through the summer and hiring improves.

Analysts say both initial and continuing claims could see a sharp decline in mid-June, when many states plan to opt out of enhanced federal UI benefits.

The main speakers to follow on Thursday include ECB's Pentti Hakkarainen, Luis de Guindos, Frank Elderson and Isabel Schnabel.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.