Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

The week ends with a few data events of note, including Italian business and consumer confidence indicators at 0900BST, followed by the CBI distributive trades survey at 1100BST. The highlight in terms of data releases in the US is the publication of personal income and consumption figures at 1330BST.

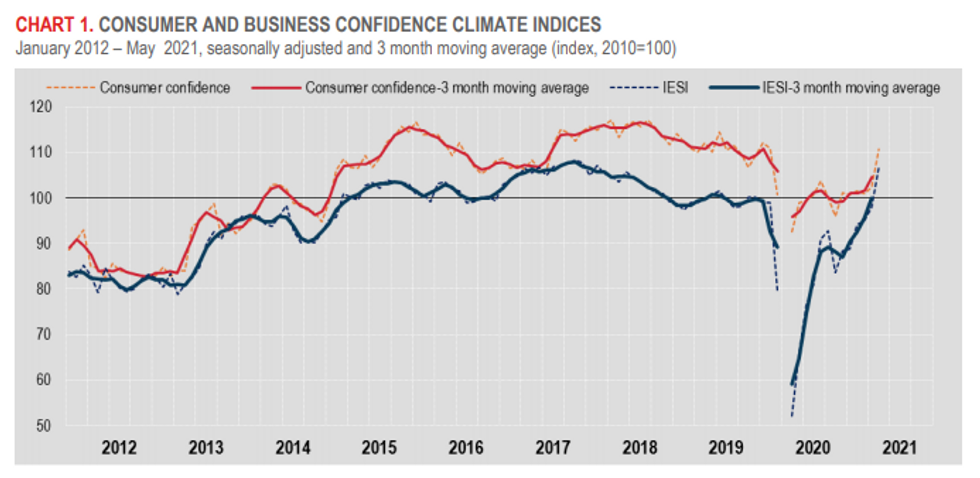

Italian consumer sentiment seen higher

Italian consumer confidence is forecast to improve further in June to 112, up from 110.6 recorded in May where the index jumped to the highest level since the start of the crisis. May's uptick was mainly led by a solid increase of the future climate as well as economic confidence. Italy's vaccination rate is improving with more than 50% having received the first dose and a quarter of the population being fully vaccinated, which bodes well with consumer's mood. Meanwhile, manufacturing confidence is also expected to edge higher in June to 112, up from 110.2.

Other survey evidence is in line with market forecasts. The EZ flash consumer confidence saw another sharp increase in June, while the EZ flash composite PMI, which also includes Italian data, rose to a 180-month high.

Source: Istat

CBI retail sales to fall

CBI retail sales are expected to tick down to 10 in June, down from 18 reported in May. Nevertheless, the indicator is projected to remain in positive territory following several months of decline. Last month's survey noted that sales for grocers, non-store retailers, DIY and furniture shops were still above seasonal patterns, while clothing and department store sales remained below. May's report noted that firms expect their business situation to remain stable in the next three months.

US personal income seen lower

U.S. personal income likely fell 2.8% in May according to Bloomberg, following April's 13.1% decline and reflecting waning government aid. Spending is set to have slowed further in May, mostly driven by a drop in goods spending that could partially offset gains in services. Spending in May likely increased 0.3% following a 0.5% gain in April. The PCE price index should increase 0.5% after rising 0.6% in April, while the core PCE price index should increase 0.6% following April's 0.7% gain.

The main events to look out for include speeches by Christine Lagarde, Minneapolis Fed's Neel Kashkari, Cleveland Fed's Loretta Mester, Boston Fed's Eric Rosengren and New York Fed's John Williams.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.