Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

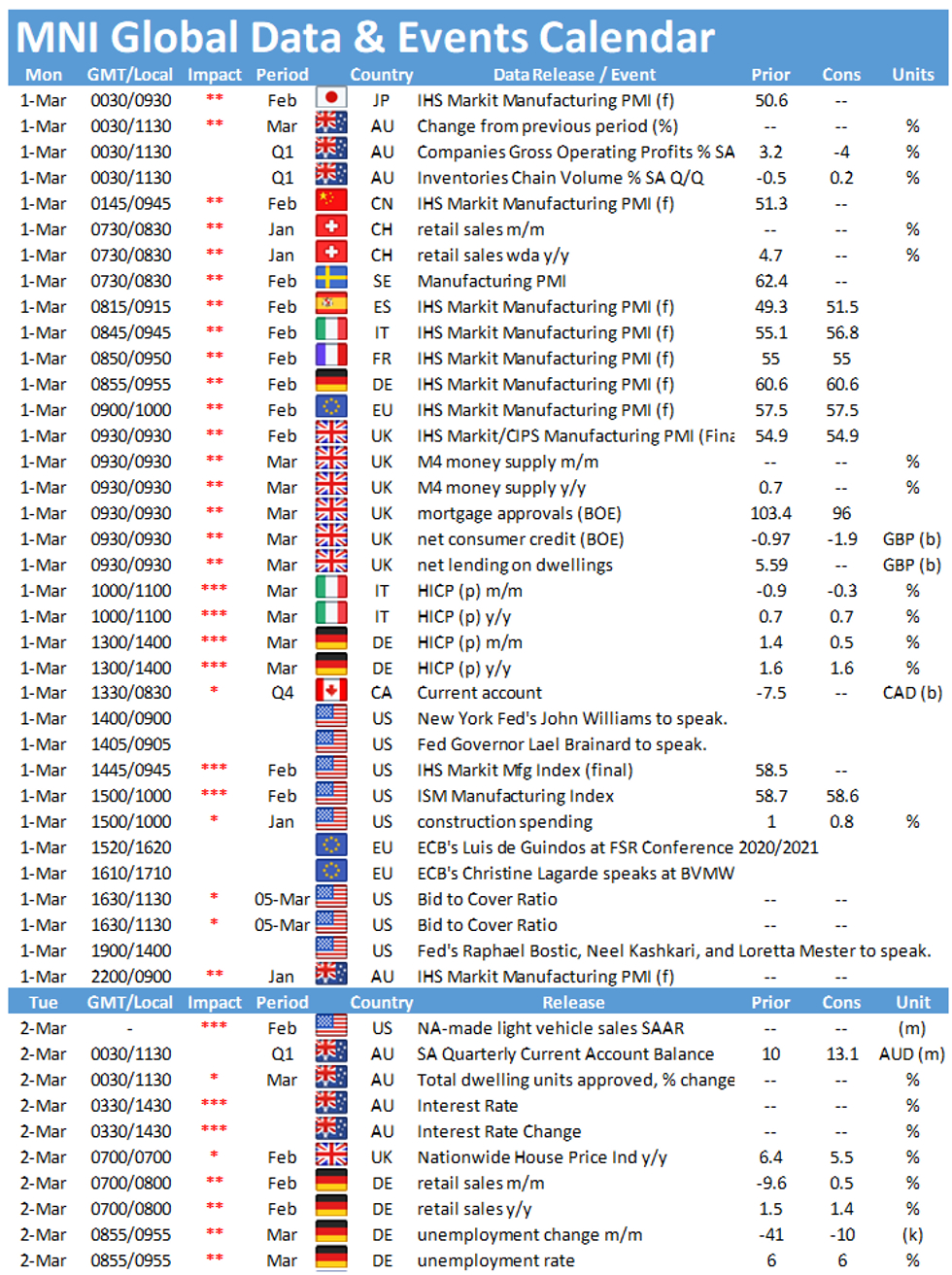

Monday kicks off with the release of the final manufacturing PMIs for Spain (0815GMT), Italy (0845GMT), France (0850GMT), Germany (0855GMT), the EZ (0900GMT) and the UK (0930GMT). Additionally, the release of flash German flash inflation will be watched closely at 1300GMT. In the US, the highlight of the day is the publication of the ISM manufacturing PMI at 1500GMT.

Manufacturing PMIs hold up well

Spain's and Italy's manufacturing PMIs, for which no flash estimates are available, are forecast to rise in February to 51.5 and 56.8, respectively. Spain's manufacturing fell below the 50-mark in January, dropping to 49.3 due to several factors such as covid-restrictions, the Storm Filomena and supply chain issues. Italy's index surged to a 34-month high in January, rising to 55.1 and signalling expansion.

France's, Germany's, the EZ's and the UK's manufacturing PMIs are expected to register in line with the flash estimates showing monthly gains in February. All four indicators remain comfortably above the 50-mark, signalling expansion of business activity in the manufacturing sector. While France's index ticked up to a three-year high of 55.0, Germany's manufacturing PMI rose to 60.6. The EZ's index increased to a 36-month high of 57.5, while the UK's indicator ticked up to 54.9. All flash reports noted severe supply chain disruptions which also led to an increase in prices. While export orders surged in Germany and expanded in France, export sales remained weak in the UK with anecdotal evidence suggesting that fulfilling orders to the EU meant higher costs and transportation delays.

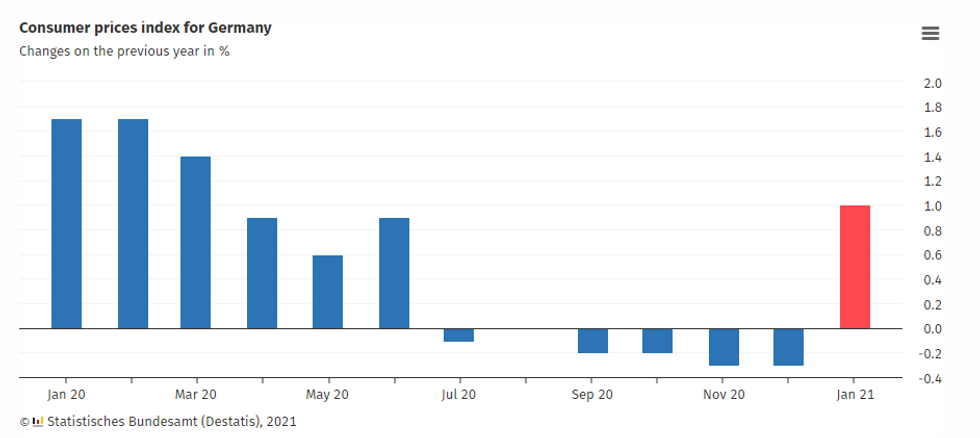

German flash inflation seen unchanged

Markets are looking for German annual inflation to print at 1.6% in February, unchanged from January. The monthly rate is forecast to slow to 0.5%, down from 1.4% seen in the previous month. Inflation rose sharply in January to a 11-month high of 1.6%, up from -0.7% recorded in December. January's increase was driven by the end of the German VAT cut which led to a decline in prices since the start in July 2020. Looking ahead, energy price base effects are likely to boost inflation in the coming months.

Source: Destatis

ISM manufacturing PMI expected to tick up

The ISM manufacturing PMI eased to 58.7 in January, down from 60.5 seen in December. January's downtick was led by sharp drops of New Orders and Production. On the other hand, Employment and Supplier Deliveries increased in January. Last month's report noted that firms still reported absenteeism, short-term shutdowns to sanitize facilities and difficulties in finding new staff which all weigh on activity growth in the sector. In February, markets expect the ISM manufacturing PMI to edged slightly lower to 58.6. Similar survey evidence is in line with market forecasts. The Chicago Business Barometer ticked down in February on the back of falling orders and production, while the flash IHS manufacturing PMI eased to a two-month low.

The main events to look out for on Monday include speeches by New York Fed's John Williams, Fed's Lael Brainard an Raphael Bostic as well as the ECB's Luis de Guindos and Christine Lagarde.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.