Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

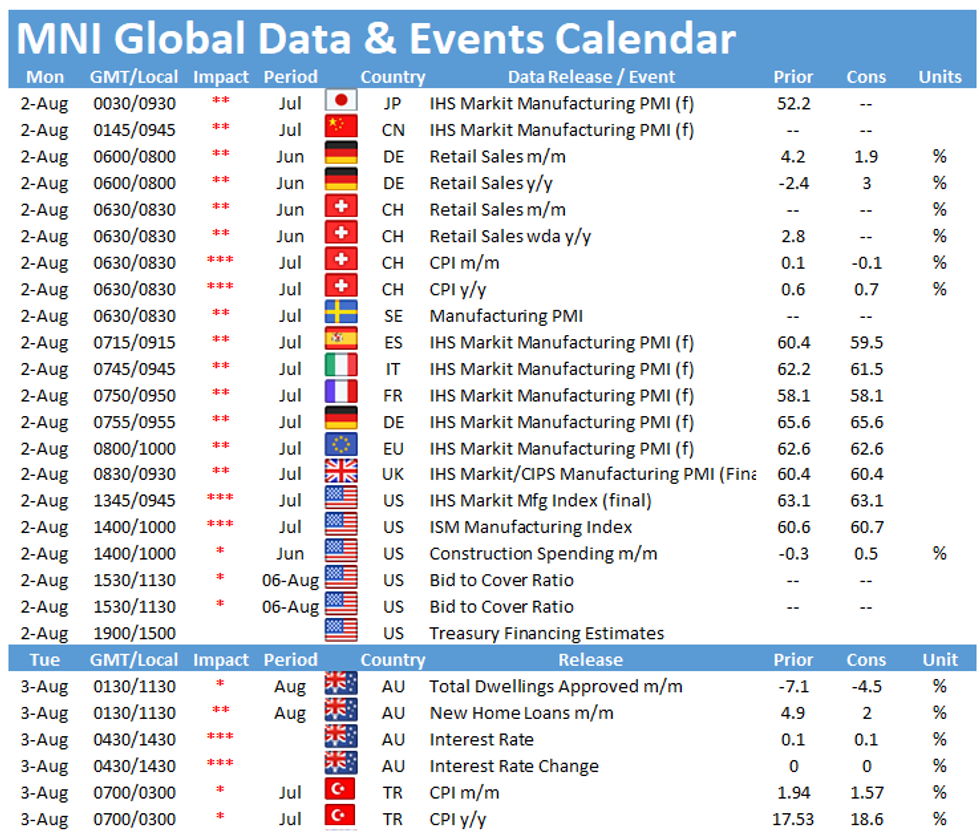

Monday kicks off with the release of German retail sales at 0700BST, followed by the publications of the final manufacturing PMIs for Spain (0815BST), Italy (0845BST), France ( 0850BST), Germany (0855BST), the EZ (0900BST) and the UK (0930BST). In the US, the publication of the ISM manufacturing PMI will be closely watched at 1500BST.

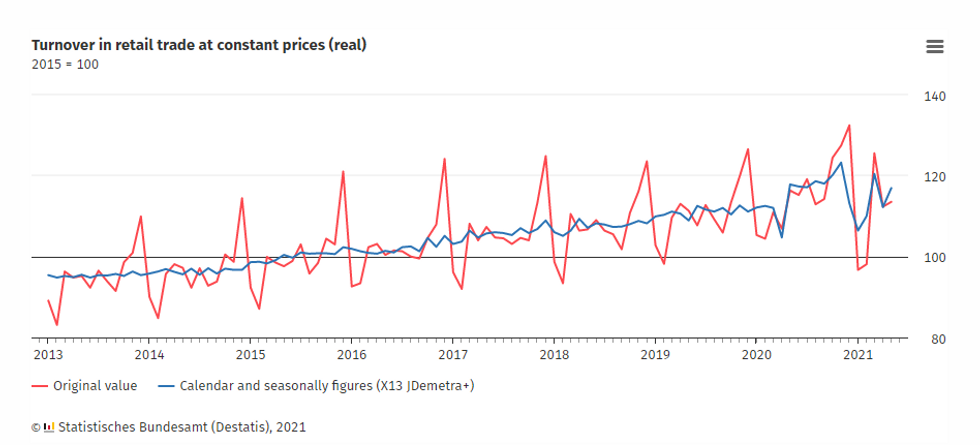

German retail sales seen slowing

Monthly German retail sales are expected to decelerate in June to 1.9%, while annual sales are seen at 3.0%. In May, the monthly index rose by 4.2%, after a sharp decline of 6.8% in April. Destatis noted that falling infection rates and an easing of restrictions pushed up May's sales figures. Compared to February 2020, retail sales were 3.9% higher in May 2021. Germany's consumer confidence stagnated in August, as economic and income expectations declined. However, the propensity to buy saw a monthly gain, which bodes well with future consumer spending.

Source: Destatis

Final manufacturing PMIs seen at flash estimate

While the French and EZ flash manufacturing PMIs dropped in July to 58.1 and 62.6, respectively, the German index rose to a 3-month high of 65.6. Markets expect all three indicators to register in line with the flash results. The EZ flash report noted that business activity in the manufacturing sector was slowing due to the worsening of supply lines in July. Moreover, prices and order backlogs rose at the fastest pace since records began. Business confidence deteriorated in July as firms were concerned about the spread of the delta variant.

The Spanish and Italian manufacturing PMIs are forecast to ease slightly in July to 59.5 and 61.5, respectively. However, both indicators remain in expansion territory, signalling business activity growth in the sector.

The UK's manufacturing PMI eased to a four-month low in July, falling to 60.4. Nevertheless, the index remains comfortably above the 50-mark. Production was hampered by a shortage of materials and critical components. Nevertheless, firms reported strong domestic and export demand in July.

ISM manufacturing PMI seen marginally higher

The ISM manufacturing PMI is forecast to tick up slightly to 60.7 in July, after dropping to 60.6 in the previous month. June's decline was led by a 3.7-point decrease of Supplier Deliveries, followed by New Orders and Employment, both down 1pt. On the other hand, an uptick of Production and Inventories offset some of the declines.

Similar survey evidence provides a mixed picture. The Chicago Business Barometer rose markedly in July, while the Dallas Fed manufacturing index posted a monthly decline.

The events calendar remains quiet on Monday with no speeches scheduled for the day.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.