Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

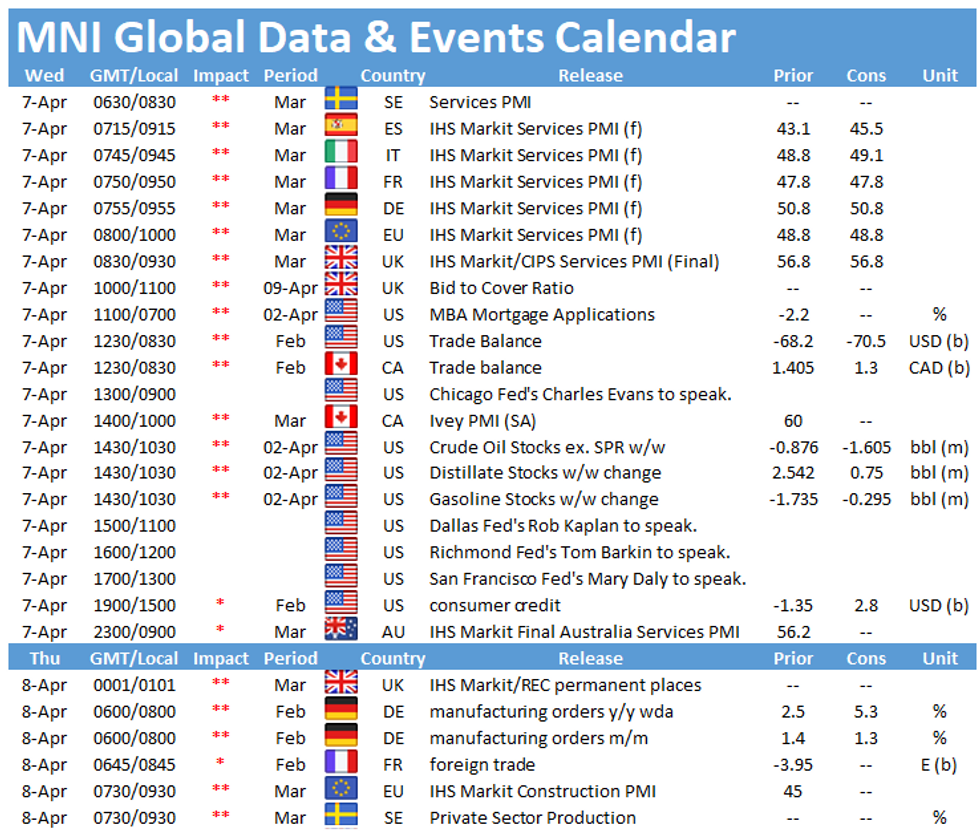

The main data events Wednesday include the publication of the final services PMIs for Spain (0815BST), Italy (0845BST), France (0850BST), Germany (0855BST), the EZ (0900BST) and the UK (0930BST). In the US, the release of the trade balance at 1330BST will be closely watched.

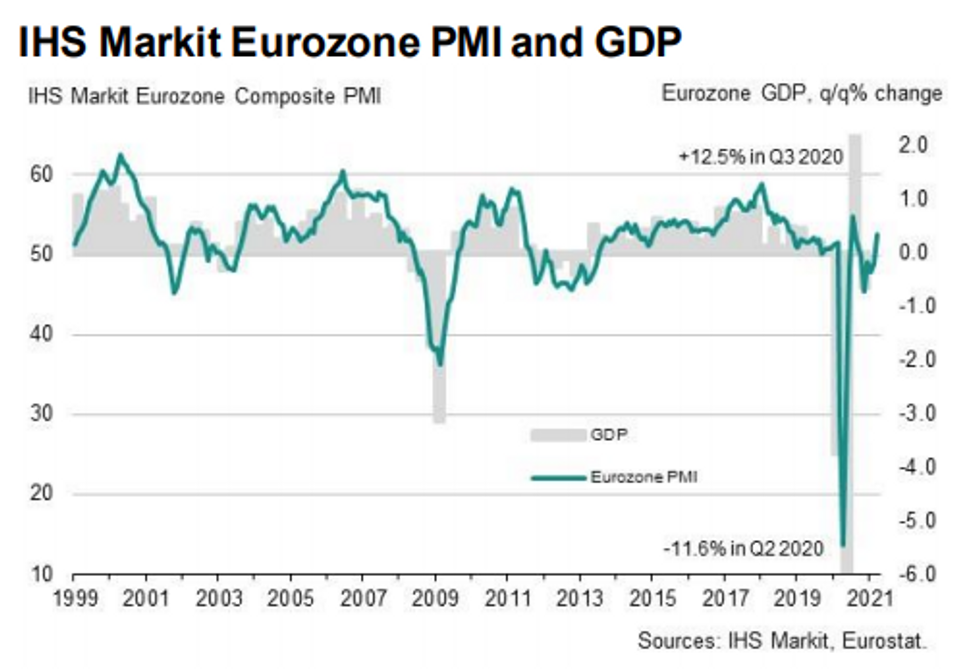

Germany's services PMI outperforms its EZ peers

French, German and EZ services PMIs are seen in line with the flash estimate showing monthly gains in March, although the French and EZ indices remain in contraction territory. France's flash services PMI rose to a three-month high of 47.8 in March, while the EZ index hit a seven-month high at 48.8. Among the euro area countries, Germany recorded the best flash results as the services PMI was the only one to rise above the 50-mark to 50.8 in March, signalling expansion. Nevertheless, the other euro area economies also saw improvements and showed slower rates of contraction. Generally, business activity is still directed by the development of the pandemic and subsequent restrictions.

Spain's and Italy's services PMIs, for which no flash estimate is available, are forecast to improve slightly as well in March to 45.5 and 49.1, respectively. Both indicators are still seen below the 50-mark as restrictions remain tight in both countries and business activity in the service sector is therefore still restricted.

UK services PMI back in expansion

According to the flash estimate, the UK's services PMI rose to a 7-month high in March and shifted back to expansion territory at 56.8. March's uptick was driven by a rebound of new orders which rose for the first time since September 2020 mainly due to increased sales ahead of the easing of lockdown measures and improving consumer confidence. The services PMI is likely to see further increases in the coming months when the economy is reopening gradually, and restrictions get eased.

US trade deficit seen widening

The US trade deficit expanded in January to USD 68.2bn following December's reading of USD 67bn. While exports rose by 1.0% in January, imports ticked up by 1.2%. In February, markets expect the trade deficit to widen further to USD 70.5bn. Survey evidence indicates subdued exports in the coming month. The ISM services and manufacturing PMI recorded a decline in new export orders, while the IHS manufacturing noted saw export orders increase, although at a slower pace. Both the ISM services and manufacturing PMI saw imports increase marginally.

The main events to look out for on Wednesday include speeches by Chicago Fed's Charles Evans, Dallas Fed's Rob Kaplan, Richmond Fed's Tom Barkin and San Francisco Fed's Mary Daly.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.